Bali is known as the Island of The Gods. It exudes a unique cultural appeal, excites holiday-goers with its natural beaches and tantalizes foodies with its wide-range of culinary cuisines. It is little wonder that Bali is an extremely popular beach destination in South-East Asia. It would not be surprising if some of you have already booked a trip there for the upcoming summer holidays. Before departing for your holidays, don’t forget to purchase your travel insurance policy. Do ensure that your travel insurance policy contains “must-have” features such as medical expenses, emergency repatriation, trip cancellation/curtailment, baggage cover etc.

Travel insurance is important because it offers financial compensation during events such as travel disruptions. For instance, Moung Agung’s eruption in 2017 led to the closure of the airport for several days. As a result, additional hotel accommodation needs to be booked, flights rescheduled and some tourists even sought alternative modes of transportation. All these would add additional costs to your holiday budget. While travel inconveniences are entirely unpredictable, a travel insurance policy purchased in advance could partially offset some of these unforeseen expenses.

Many adventurous tourists visit Bali to try activities such as hand-gliding, para-gliding, diving etc. With its picturesque scenery, Bali boasts many adrenaline-filled activities for the sports junkies. You might want to consider getting travel insurance coverage before attempting these leisure activities. For instance, AXA’s SmartTraveller provides coverage for leisure activities such as parachuting, sky diving, bungee jumping etc. Having a travel insurance policy before attempting these leisure activities could provide an additional level of assurance.

Before embarking on your long-awaited getaway to Bali, it is therefore critical to be well-informed of the best travel insurance policies available in the market. You can compare travel insurance policies on SingSaver and directly purchase one that best suits your holiday needs. Comparing on SingSaver is not only convenient; it also helps you save money on your travel insurance policies!

Update: SingSaver is having a flash sale on 19 – 20 May 2018 on selected insurance products, including AXA, where the first 10 successful applicants in each hour (10am, 4pm, 10pm) get their travel insurance for free! For more details, click here.

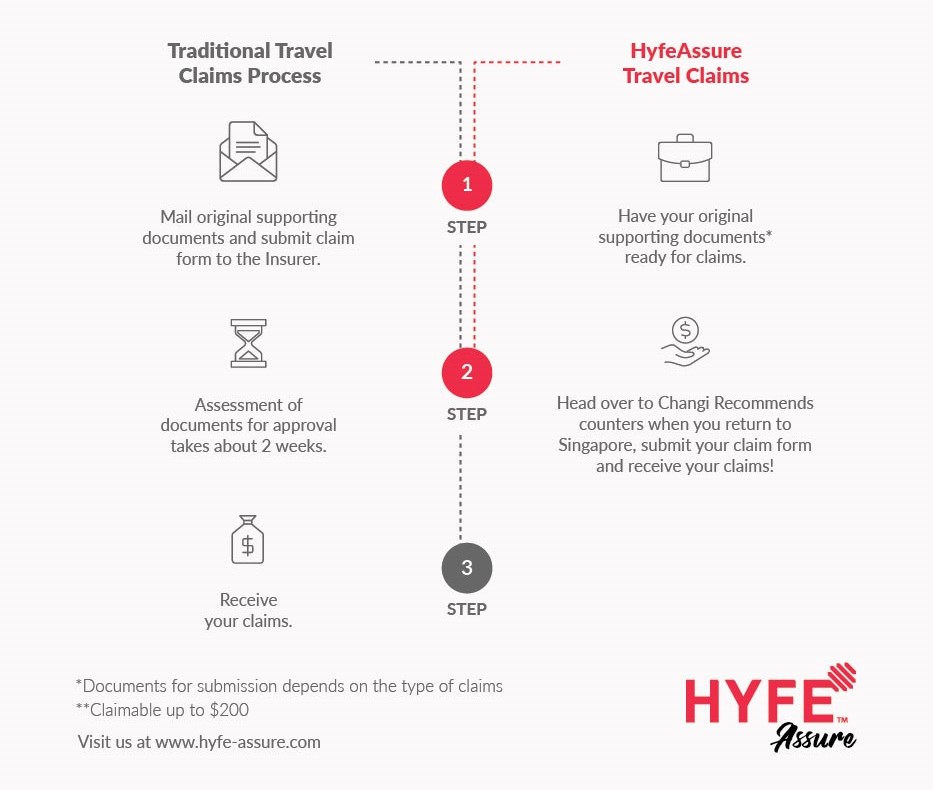

Consumers typically grapple with various issues when trying to file travel claims with travel insurance providers. For instance, consumers might lack the knowledge with regards to the administrative process of filing claims. This could be due to a lack of provision of clear instructions from the travel insurance provider. It is just as likely that the consumer is not bothered to find out more about the claim process until the actual need arises. Even if the consumer successfully files a claim, the process can potentially be cumbersome due to the multiple verifications required and the lengthy time involved before a claim is successfully processed. As a result, the traveller might remember less about his or her wonderful holiday, but more about the unpleasant experience with the travel insurance provider. The good news is that travellers in Singapore can now cast such worries aside as instant travel insurance claims can now be made at Changi Airport with HyfeAssure.

For the first time in Singapore, HyfeAssure allows travellers instantly process their travel claims at the Changi Recommends counters located across all 4 terminals in Changi Airport. HyfeAssure is an innovative travel insurance product underwritten by HL Assurance for Changi Travel Services. With HyfeAssure, customers can now furnish the necessary supporting documents and submit travel claims for medical expenses, travel delays or misconnections, baggage delays and baggage damages and receive immediate payouts up to $200.

This is how HyfeAssure works:

Upon returning and touching down at Singapore Changi Airport, a HyfeAssure customer can proceed to any of the Changi Recommends counter located at any of the 4 terminals.

Travel claims for cases such as medical expenses, travel delays, baggage delays, baggage damage and travel misconnections can be processed immediately at the Changi Recommends counter.

Customer must furnish the relevant supporting documents such as original medical reports, invoices from medical clinics and baggage loss and travel delay reports from airlines.

Customer service officer at the Changi Recommends counter will make an immediate assessment of these claims. Once approved, the customer can get up to $200 in cash on the spot!

As the process has shown, HyfeAssure instantly brings travel convenience up another notch since its customers can now file and receive travel claims once they touch down.

Besides the convenience factor, HyfeAssure is also competitively priced. Travellers can enjoy 50% off travel insurance when they use the promotional code 50OFF. The low and competitive premium represents excellent value for holiday-goers who would like to have a greater peace of mind when travelling. Therefore, with HyfeAssure, travellers can now kiss goodbyes to bad travel claim experiences ruining their holidays ever again!

In its fundamental form, insurance is a contract that enables individuals or entities to receive financial protection against losses. It ensures the stability of families and businesses after a crisis or other unfortunate events. Simply put, insurance grants policyholders a peace of mind. Isn’t that what everybody wants – to be able to sleep at night without having to worry about what the future holds?

These are the reasons why I am drawn to getting insurance policies. I have to be completely honest. One of the major drawbacks that I dislike about insurance is its complexity. I am apprehensive about the piles of questions and bulky documents. Do not get me started about the confusing technical terms!

To my delight, I was introduced to a revolutionary insurance company that dances gracefully with the modern tides. This was none other than FWD Insurance. FWD Insurance aims to transform the way that Singaporeans experience insurance by simplifying the purchase and claims process. It helps you to skip the agent by directly working with them online.

Say goodbye to nerve-wracking call backs and time-consuming interrogations by embracing their user-friendly website!

FWD Insurance understands how valuable a working Singaporean’s time and money is. This is why the company maximizes these two commodities through providing insurance quotations under 60 seconds for car insurance and 10 seconds for travel insurance. These impressive figures are due to the fact that FWD only asks questions that are absolutely necessary.

For instance, it took me 25 seconds to be quoted with the premium of about S$174 for a DIRECT-Term Life insurance that seeks to cover 5 years of my life. I used the rest of my day to focus on other productive matters. You can do the same thing too!

The people behind FWD best explained the company’s concept: “We believe that insurance doesn’t need to be complex, sold through middlemen, or take up vast amounts of your time.” It offers competitive prices and easy-to-understand insurance.

Attractive Insurance Products

It is usual for people to feel skeptical when they encounter an insurance company for the first time. Wash away this feeling by knowing that you are supported by a company with a strong financial record. FWD is the insurance business arm of the established investment group, Pacific Century Group (PCG).

Choose from the four secure insurance products such as DIRECT-Term Life Insurance. Car, Travel and Personal Accident.

A. DIRECT-TERM LIFE INSURANCE

The DIRECT-Term Life insurance ensures that your family’s financial future is secured despite unfortunate events such as becoming diagnosed with a critical illness, becoming permanently disabled, or passing away.

These are the primary reasons why I am drawn to this policy:

I can choose the period that works for my budget and lifestyle (e.g., 5 or 20 years).

I can purchase coverage through my smartphone – without going through a middleman.

Because FWD does not pay commission to agents, my coverage of up to S$400,000 may cost less than S$1/day.

B. CAR INSURANCE

Three comprehensive plans cover vehicle repairs, third-party damages, medical expenses, and roadside assistance. These plans were crafted to suit your personal needs and budgets.

No matter what plan you avail, your repairs will be completed by the FWD workshops. You can cruise along blissfully until your car turns ten. Furthermore, your 50% NCD is guaranteed for lifetime. NCD stands for no-claim discount. Drivers who have earned their 50% NCD get to keep it for life because they believe that one accident doesn’t make you a bad driver.

On top of that, you can add amazing features which gives you coverage when you are driving in West Malaysia and certain parts of Thailand.

C. TRAVEL INSURANCE

Take for instance; to reap the rewards of her hard work, Jena scheduled a weeklong vacation to Thailand. The beautiful country has so much to offer from pristine beaches to established sports clubs. She did not forget to pack her favorite S$200 golf putter. To enjoy a fuss-free tropical getaway, she purchased FWD’s travel insurance. It was one of the best decisions she ever made as the putter got lost in the airport and fortunately, sports equipment is covered by the policy.

Aside from sports equipment, the travel insurance also includes unlimited medical evacuation. You read that right! The last thing on your mind is how much your emergency evacuation will cost. This is why FWD has thought of this for you.

You can expect the claiming process to be a breeze too. Claim with a few clicks with the “Click to Claim” feature. This means, all you have to do is snap your boarding pass and claim for flight delays via WhatsApp. This feature is available for baggage delays too. Simply take a photo of your baggage slip and send it to FWD via WhatsApp. That is convenience at its finest!

D. PERSONAL ACCIDENT INSURANCE

Personal Accident (PA) insurance provides compensation in the event of disability, injuries or death. In fact, one feature unique to FWD is that the policy also covers the most number of infectious diseases including Zika and dengue fever. Under this policy is the Guardian Angel Benefit. If both parents pass away or become permanently disabled due to an accident, FWD will provide up to S$500,000 for the surviving children.

Lastly, natural circumstances now cannot stop you from having fun as ticketed event cancellations due to haze are covered. Apparently, they are the only insurer in Singapore to offer this.

Irresistible Features and Highlights

Before you make a commitment, it is important to know what this new insurer can do. Let me start by stating the fact that there are no middlemen or agents. Since you do not have to pay for commissions, you can save more money.

FWD allows you to complete your purchases online. It is so quick and easy to complete the online quotation that even your 9-year old niece can do it for you! As soon as you make your purchase, you will get an email with the policy. You will also receive an SMS that notifies you to check your email.

Lastly, the policies are delivered with no technical terms. You will know exactly what you will get explained in plain English.

From now till 31 January 2017, you can now enjoy a 10% discount on all FWD insurance products with this promo code – FWDHi10.

For the people behind FWD, customers are at the heart of the entire process. They let you experience exceptional insurance by minimizing your effort and making products readily accessible. May they change the way you feel about insurance!

Some Singaporeans have gone off the idea of travel insurance. While it used to be considered an absolute necessity, more travellers now think of it as an unnecessary waste of S$50 to S$100.

This is particularly true of those who go on short trips, to whom travel insurance becomes a significant expense. But are they doing the right thing?

Why No Travel Insurance?

The most common reasons are:

They have personal accident insurance

They feel the claims process is unrealistic and restrictive

The seek cost-efficiency

They are already covered by credit card

They are covered under their employer’s insurance

They Have Personal Accident Insurance

For some travellers, their main concern is their healthcare related. They do not want to face medical expenses if they suffer from a fall, get hit by a car, etc.

They are less concerned about the other things that travel insurance covers. These are things like lost jewellery (they may not be carrying anything valuable), flight delays (not an issue if they have airline memberships that already compensate them), or tour agency issues (they may not be on a package tour).

For those travelling to countries where they have friends or family, some of the emergency assistance from travel insurance may be irrelevant. For example, if you are travelling to stay with your uncle in Canada for a few days, it may not be a big deal if your luggage is diverted for a day or two. The inconvenience may not be worth a S$100 insurance policy.

(It might be a different story if you are travelling alone, and know nobody where you’re going).

These travellers typically add personal accident coverage to their existing insurance policies, in the form of a rider. This can give them comprehensive protection wherever they are, for a fairly low cost (e.g. under S$30 a month).

If they are going skiing, for example, they may be happy to rely on their personal accident coverage, without adding travel insurance.

They Don’t Want to Go Through the Claims Process

Some seasoned travellers are intimately aware of travel insurance terms, and are dissatisfied with them.

For example, many policies do not allow you to make claims for lost jewellery. For lost cash, the maximum claimable amount might be too small to be relevant (e.g. The maximum claimable amount is S$250 regardless of how much you lose, and then insurance policy alone is already over S$100).

There are often tight limits on maximum claim amounts, on a per item basis. Even if the policy insures you for you to S$1 million, for example, the maximum claimable amount on your broken iPad may only be S$500.

Some travellers also feel the claims process is unrealistic, or too convoluted. For example, you may be required to present original receipts if you want to make a claim for your broken laptop.

With regard to trip cancellations, some policies only pay out only under specific conditions. For example, a policy may not pay out if the cause of the cancelled trip is the Singapore haze or a strike (the trip may only be insured against poor weather).

As such, a subset of travellers believe travel insurance has too many restrictions to be useful. If you want to join their ranks though, you will have to be sure that you make up for lack of travel insurance with the right safety precautions, and the right personal insurance policies.

They Seek Cost-Efficiency

As a rule of thumb, it is not cost-effective to insure expenses you can pay out of pocket.

For example, it would not make sense to pay premiums to insure your socks, or to insure cheap canned food in your kitchen pantry – the odds of losing them are so low, and the cost of replacement so cheap, that the premiums would just be a waste of money.

The same theory can be expanded to things like second-hand laptops, cheap watches, old clothes in your bag, etc. Some travellers would feel no significant pain from losing these items, and prefer to have more cash on hand for shopping or better accommodations. Should they lose the items, they have more than sufficient money to replace them immediately.

(Note: if your worry is losing your luggage and having no clothes, toiletries, etc., you should note that most airlines provide supplies or funds for passengers whose luggage they lose).

Their Credit Card Offers Free Travel Insurance

Many air miles credit cards, such as the Citi PremierMiles Visa Card, come with complimentary travel insurance if you charge your travel tickets to it. The Citi PremierMiles Visa Card covers up to S$1,000,000 in case of death or permanent disablement from accident in a common carrier, up to S$40,000 for medical expenses during a trip, and travel inconvenience.

If you are satisfied with these, there’s no need to buy more travel insurance.

They are Covered by Their Employer’s Insurance

Many people overlook this, so make sure you don’t.

If you are flying abroad for business, check with Human Resources on whether you are covered under your employer’s insurance. If there already is one, you do not need to buy your own.

Some companies have generous corporate insurance plans, that will cover you even if you are not on official business. If so, all you need to do is familiarise yourself with the terms (and get private only if you are unsatisfied).

“Do you want travel insurance?”, a sentence has become so common that it is now included in the menu of tour packages and online travel booking. While some of us may be guilty of travelling without getting covered, travel insurance has now evolved into a need rather than a want.

Ask yourself these questions:

Who will evacuate you when you are injured on top of Mount Fuji?

Who will bear the cost of cancelled air tickets or tour package during the protests in Hong Kong? A flood in Australia? Or if you and your travel companion is hospitalized days before your travel?

Who will be the one you call when you are terribly ill in Europe? Or when your rented car has crashed into a monumental sculpture?

Who will cover the cost of your essentials when you lost your baggage or your travel documents?

The list can go on but instead of trying to spoil your holiday planning, we have come up with a guide for you to compare travel insurance plans in Singapore.

We had compiled the data across different insurance companies so that you can have an idea of which offer the best cover for each risks you identified as well as getting the cheapest travel insurance in Singapore.

Let us first examine a few common benefits that you should be looking at when purchasing a travel insurance.

Medical treatment and emergency evacuation

(Image credit: Phalinn Ooi, via Flickr)

Sure, you can be as healthy as a horse but you can’t avoid getting hit by someone skiing down the mountain or prevent a dengue mosquito that wants to sting you. Shit happens, and that could cost you ten or thousands of dollars when you are overseas. It is not too bad if there is a hospital nearby but what if you are trekking on the remotest part of the island? Emergency medical evacuation could easily set you back between $75,000 – $300,000.

You don’t want me to add the medical expenses, do you?

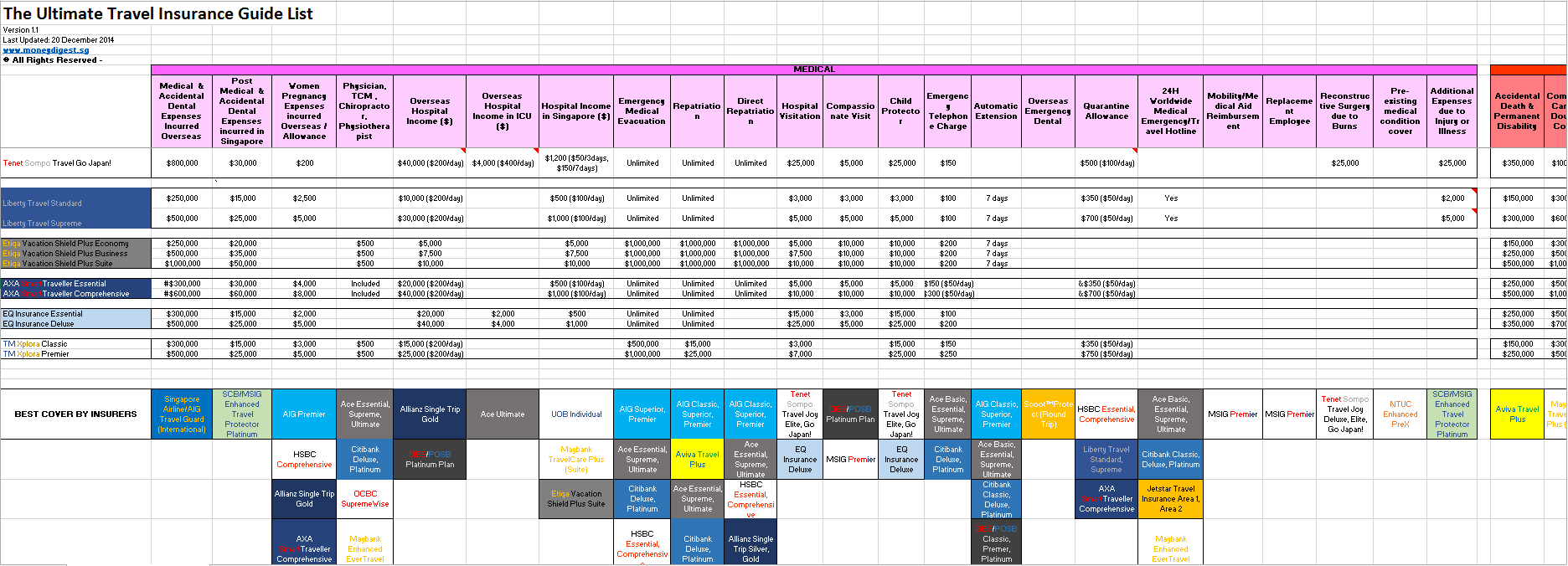

From our list, Singapore Airline Travel Guard offers the best cover for medical and accidental dental expenses when you are overseas. You can claim unlimited benefits from their International plan underwritten by AIG. For emergency evacuation and repatriation, there are many companies that offer unlimited cover, including AIG’s own flagship Travel Guard plans. The word ‘unlimited’ is equivalent to a peace of mind that is important to all travelers, including myself.

Accidental death and permanent disability

(Image credit: Dominik Golenia, via Flickr)

Should the most unfortunate event that results in death and permanent disability, there is an additional payout to you and your family members. Aviva offers the highest coverage of up to $2million to protect you and you family from the liability of you suffering from permanently incapacitatation or premature death.

Hospital income

(Image credit: aenri05, via Flickr)

Whether you are hospitalized overseas or in Singapore, it may take weeks or months for you to recuperate. If you are still employed, you may end up having to take no-pay leaves and this could come in handy when you receive a daily income for your stay in hospital. It makes sense when you still have you bills and mortgage to pay and a parents to support. DBS TravellerShield and Allianz Gold plan has the best overseas hospital income benefits with the highest limit of $50,000, with the latter paying you $250 a day. (vs $200 a day from DBS)

However, if you are hospitalized in Singapore, a plan from UOB, Maybank’s TravelCare (Suite) and Etiqa’s Vacation Shield Plus (Suite) make more sense as they have the highest limit of $10,000.

So which should you choose?

Besides comparing the premium amounts, take the destination you will be travelling to into consideration and if it is located far away from Singapore. That is to say if you are travelling to Europe or the US where it may be difficult to transport you back to Singapore for local treatment, then overseas hospital income should be your priority. Whereas if you are travelling to a country in South East Asia, you should be looking at a higher hospital income limit in Singapore.

Travel cancellation, curtailment and disruption

(Image credit: Ross G. Strachan, via Flickr)

When you have spend thousands of dollars booking your tour package or air tickets months in advance, you may well want to get this covered. Some airlines offer a non-refundable air tickets and should you have a last minute cancellation due to serious illness, riots or flash flood, your month-worth of paycheck would be down in the drain.

Allianz Gold plan beat all other plans hands down as it tops the list of benefits with a $25,000 limit for travel cancellation, postponement, curtailment and interruption.

Delay or loss of personal baggage

(Image credit: donuzz, via Flickr)

Most people buy travel insurance to protect their baggage and belongings as it seems to be the most common mishap that could happen on a trip. Again, Allianz has outshone the rest with a $15,000 cover on personal baggage and a $10,000 cover on travel documents. However for baggage and travel delays, Etiqa Vacation Shield Plus Suite is a better option with a $5,000 limit.

Other benefits such as golf benefits, home cover, car rental excess and more

If you are planning to go on a green trip, golf benefits may be more attractive as you are covered from things such as loss or damage to your golf equipment to getting an incentive for getting a hole-in-one. With up to $3,000 cover limit for your golf equipments, golf junkies look no further to HSBC Comprehensive and AXA SmartTraveller plans. If you on your way to become Tiger Woods, Ace Ultimate plan will offer the highest bounty for a hole-in-one, currently at $750.

Insurance companies has gotten more creative over the years. From offering you cash incentive such as a hole-in-one, you can get covered at almost anything you can think of such as reimbursement for pet medical care to protecting your home from any damages. Besides taking into account of the benefits offered by insurers, you should also compare the premiums to make sure you get the most value for the cover.

Read the fine prints of the policy as some insurers define each benefits differently. For example, some insurer requires you to seek medical advice or treatment when you are overseas to be eligible to claim for your medical expenses incurred in Singapore, while some allow you to claim if you seek medical advice within 48 hours of returning to Singapore.

In short, some of the most common benefits are highlighted below:

Benefits

Recommended plans

Overseas Medical Expenses

Singapore Airline Travel Guard (International)

Medical Expenses in Singapore

SCB Enhanced Travel Protector Platinum

Overseas Hospital Income

Allianz Single Trip Gold, DBS Platinum Plan

Hospital Income in Singapore

UOB Individual, Maybank TravelCare Plus (Suite), Etiqa Vacation Shield Plus Suite

Emergency Medical Evacuation/Repatriation

AIG Travel Guard Superior/Premier, Ace Essential/Supreme/Ultimate, HSBC Essential/Comprehensive, Allianz Single Trip Silver/Gold, Tenet Sompo Travel Joy Deluxe, AXA SmartTraveller Essential/Comprehensive

Pre-existing medical conditions

NTUC Enhanced PreX

Child education grant, family assistance

MSIG Premier

Accidental Death & Permanent Disability

Aviva Travel Plus

Travel cancellation, postponement, etc

Allianz Single Trip Gold

Travel baggage delay, overbooking and misconnection

Etiqa Vacation Shield Plus Suite

Golf benefits

HSBC Comprehensive, AXA SmartTraveller Comprehensive

Visit our Travel Insurance Guide for a full list of benefits and the respective premiums of each insurers.