Turn your spending into miles, cash backs and other exclusive perks.

Whether you want to enjoy cash back or accumulate miles, credit cards when used responsibly can be a way to stretch your dollar further. Wouldn’t it be great to save a little on things you usually spend on? Besides perks and convenience, you can also build a positive credit history when you make your repayment on time! The key is to use them wisely.

SingSaver.com.sg, one of Singapore’s one-stop comparison portal, has turned 3 this year. To celebrate this milestone, users who use their portal and sign up for any of the credit cards will get extra sign-up bonus in addition to the bank’s welcome gift when you apply for these cards. Forget roadshows. This is the real deal. Did we say more than $500 cash and shopping vouchers or more? (Yes, the cash will be deposited into your designated bank account.)

Sign up for more than one and receive multiple welcome gifts:

1 Credit Card = Up to $150 Cash

2 Credit Cards = Up to $300 Cash ($150 + $150)

3 Credit Cards = Up to $300 Cash ($150 + $150) + Samsonite Luggage etc

.. and so on

Start applying here now or by clicking on the cards below.

With a minimum income requirement of S$30,000, this is probably one of the easiest to qualify for those who want to turn their spending into free flights. It is also one of the most convenient way to earn KrisFlyer miles since all miles earned are automatically credited to your KrisFlyer account with no conversion fee!

Earn 1.1 KrisFlyer mile for every S$1 spent on all your eligible purchases with your Card

Earn 2 KrisFlyer miles for every S$1 equivalent in foreign currency spent overseas on eligible purchases during June and December.

Earn 3.1 KrisFlyer miles for every S$1 spent on Grab and Uber rides, up to S$200 each calendar month.

More miles and more rewarding privileges. The American Express® Singapore Airlines KrisFlyer Ascend Credit Card earn more miles on every S$1 spent. It also gives you complimentary airport lounge access 4 times in a year and a complimentary night with Millennium Hotels and Resorts.

Earn 1.2 KrisFlyer miles for every S$1 spent on all your eligible purchases with your Card

Earn 2 KrisFlyer miles for every S$1 equivalent in foreign currency spent overseas on eligible purchases during June and December

Earn 3.2 KrisFlyer miles for every S$1 spent on Grab and Uber rides, up to S$200 each calendar month

Earn your miles faster with one of the best cards for your travel needs. The Citi PremierMiles Card lets you redeem from the widest range of airlines, where 1 Citi Mile = 1 Mile, with KrisFlyer, Asia Miles, Qantas, Qatar, Flying Blue, and more. With no caps on miles earned, redeem your miles for flights, hotels and merchandises. You can also receive up to 42,000 bonus miles as welcome gift.

Earn 1.2 miles for every S$1 spent on all your eligible purchases with your Card

Earn 2 miles for every S$1 equivalent in foreign currency spent overseas on eligible purchases

The card that offers you the highest local and overseas earn rate all year round. The UOB PRVI Miles Card lets you earn 1.4 for every S$1 spent locally and 2.4 miles on every S$1 spent overseas. Earn 6 miles for spends on major airlines and hotels booked through Expedia, UOB Travel, and Agoda.

With no minimum spend and cap on miles earned, every spend adds up to free flights. Redeem miles from over 40 partner airlines and complimentary personal accident and travel inconvenience insurance coverage of up to S$1,000,000.

The new OCBC Titanium Rewards Card now gives you more rewards points in more places. Whether you shop online or in stores, locally or overseas, or pay using mobile payments – you now earn 10x OCBC$ for every S$1 spent on selected categories – equivalent to 4 miles for every S$1 spent!

The Titanium Rewards Card should be in miles collector’s portfolio because of its high miles per dollar rate, and also because mobile payments also qualify for 10X OCBC$ (4mpd), you don’t have to worry whether your spend belongs to any qualifying categories. As long as Android/Samsung/Apple Pay is accepted, you can be sure you will get your 10X bonus!

Live large with the new Standard Chartered Rewards+ Credit Card. Earn up to 10X rewards points with every S$1 spent on foreign currency and more. No minimum spend required.

Get up to 10X rewards points for every S$1 spent in foreign currency on overseas retail, dining and travel transactions. No minimum spend required. (Rewards+ Card Promotion T&Cs apply)

Get up to 5X rewards points for every S$1 spent on dining transactions. No minimum spend required. (Rewards+ Card Promotion T&Cs apply)

Get 1 rewards point for every S$1 spent, on all eligible spend. No minimum spend required. (Rewards+ Card Promotion T&Cs apply)

Enjoy 1-for-1 Platinum Movie Suites Tickets with Cathay Cineplexes².

Apply now and make 5 qualifying transactions on your mobile wallet to receive up to $120 cashback.

Get 5x Rewards on dining, entertainment and online purchases (equivalent to 2 miles for every dollar spent) with HSBC’s Revolution credit card. What’s more, there’s no minimum spend and 2 years’s annual fee waiver. 5x Rewards include:

Dining: restaurants, cafes and fast food outlets on your local dining transactions.

If you’re only going to live once, you might as well live large. The UOB YOLO Card has a bundle of exciting offers, but its entertainment deals are truly remarkable.

You get 8% rebate on weekend entertainment, 3% rebate on weekday entertainment, 1-for-1 movie tickets at Cathay Cineplexes, and exclusive access to the Priority Queue at Switch, Barber Shop, Timbre @ The Substation, and Timbre @ The Arts House. You and a friend also get free entry at Zouk and one free house pour on Wednesdays and Fridays!

No cashback cap and no minimum spend, the Standard Chartered Unlimited Cashback Card lets you enjoy 1.5% cashback on all spend – from beach holidays to buffet feasts, or even your new wardrobe. How much better can it gets? Think of it as the card to use after maxing out the benefits on other cards. This card gives you 1.5% cash back with no cap and no minimum spend requirement to make all your spend even more worthwhile.

You can earn absolute 1.5% cashback on any spend, without caps. This means that you can earn cashback on every dollar you spend on your American Express True Cashback Card, without having to worry if you have maxed out the cashback you would be receiving.

What’s more? You get to earn 3%* cashback on your first S$5,000 spend during the first 6 months of your Card Membership.

When you use your Card for everyday purchases, you won’t believe how quickly your cashback can add up. With no spend caps imposed, earning cashback is simpler.

Keep this card in your wallet. The Citi Cash Back Card is one of the best cash back card in the market, offering a whopping 8% cash back on your Dining, Grab rides, Groceries and Petrol daily, worldwide. Imagine this: every $1,000 spends get you $80 cash back in a month. That works out to be almost a thousand dollar of cash savings in a year!

Get cashback on your daily spend. The OCBC 365 Card lets you enjoy up to 6% cash back on dining, online shopping, petrol, grocery and more. That’s not all. You can even enjoy 3% cash back your telco bills.

Are you the one paying for the recurring mobile, cable TV and Internet bills? Apply for the HSBC Visa Platinum Card and start paying less! The HSBC Platinum Card offers up to 5% cash rebate on your daily expenses such as groceries, fuel and dining and it is also one of the only few cards that includes your recurring telephone bills.

In addition, you also get 1 Reward point for every $1 spent. This is on top of the cash rebates which you would have already enjoyed. With the Reward point, you can redeem a great variety of rewards, from everyday essentials to gourmet delights and a dedicated range of luxury rewards to cater to your fancy side.

The right connections can be rewarding. With no minimum spend required, you will now enjoy up to 3.5% cash back on all your purchases* with the new, well connected HSBC Advance credit card. HSBC Advance banking customers enjoys additional 1% cash back.

Another great reason to go on that shopping spree. With no minimum spend and up to $60 cashback monthly, there’s another great reason to go on that shopping spree with Standard Chartered Singpost Spree Card.

Earn 3% cashback on all online spends in foreign currency and all vPost spends.

Earn 2% cashback1 on all online spends in local currency, all contactless and mobile payments.

Earn 1% cashback1 on all other retail spends.

Online Price Guarantee: Get a refund of 50% of the price difference if you find a lower price for the same item within 30 days of your online purchase

Enjoy 20X Rewards^ when you shop at selected department stores in Singapore with your Citi Rewards Card. Plus, earn 10X Rewards* on your shopping all year long. Shopping is more rewarding with the Citi Rewards Card!

Get 20X Rewards^ (20 points or 8 miles for every S$1 spent) when you shop at Duty Free Singapore (DFS), Takashimaya and TANGS. Valid till 3 May 2018.

Earn 10X Rewards* when you shop for shoes, bags and clothes at online or retail stores, or department stores, locally and overseas.

Redeem your points from an amazing range of merchandise from across the globe or for the perfect holiday through Citi ThankYousm Rewards.

Get rebates for the things you love. Chill out and hang out with OCBC Frank Credit Card – Get 6% rebate on online shopping (including flights and hotels) and 5% on weekend entertainment.(i.e Starbucks, The Coffee Bean & Tea Leaf, Cinemas, Bars and Clubs)

Earn up to $60 rebates per month — that’s $720 worth of savings a year! Express your individuality with 120 unique card designs to choose from.

All is fine and dandy when your life is nicely panned out for you, but as Singaporeans, we can never be too cautious. What if a once-in-a-lifetime opportunity knocks, and you suddenly require a larger-than-expected sum of money to seize this opportunity?

Opportunities can come in different forms in your various stages in life. There may be investment opportunities, a chance to go abroad on an exchange programme, or a chance to further develop your skill sets.

If you find yourself short on cash and need a sum of money to tide you over a short period of time, a personal loan can come in useful.

When we think about loans, most would frown upon it. We would assume that borrowers are incapable of managing their own finances, or that they are financially irresponsible. That is but a misconception, as personal loans are merely tools that can improve our lives if used in a responsible and wise manner.

As compared to home loans, car loans or educational loans which have specific purposes, personal loans are a more flexible type of loan which can be used for almost any purposes you wish. The most straightforward of which are personal instalment loans, where you borrow a lump sum of money from a bank. You can use the borrowed cash for any reason you like. Payment is in fixed monthly payments over a specified time period.

You never know when you might need a loan, but it’s always good to be aware that there is this option out there without breaking the bank. A loan can be useful in the following situations:

A buffer for depleting all your savings – taking a personal loan instead of using up your emergency savings in case of, well, emergencies, and you need the savings

Seizing opportunities with smaller cash outlays – taking a personal loan for immediate cash to enrol in a workshop or class to improve your skill sets and employability, which will result in an eventual higher return

Fulfilling aspirations – perhaps an exchange abroad, a hobby you’ve always wanted to master or even an important bucket list item

Repaying a high-interest loan first – taking a personal loan to pay off higher-interest loans, such as credit card bills

Not all banks and money lenders are created equal. Different financial institutions offer different incentives – some offer lower interest rates while others have lower minimum criteria.

Ultimately, it’s always good to compare loans before applying for one, so you end up with the best bang for your buck for your personal goals and budget – one that has the lowest interest rate, the lowest fees, meets your requirements and has the best welcome offers.

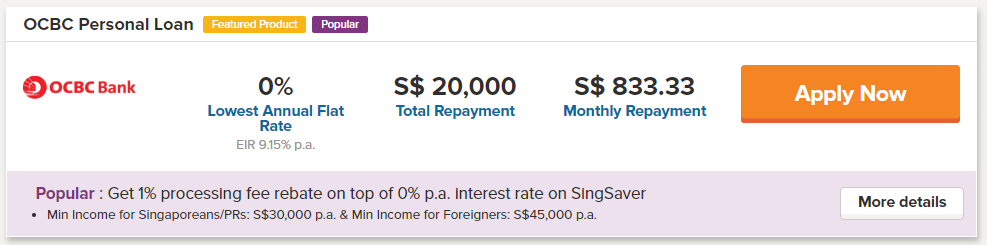

SingSaver offers a convenient platform for comparing between different financial institutions. For a limited time only, get the first 3 months of interest FREE when you apply from SingSaver’s website. That’s not all — SingSaver has also partnered OCBC to offer 0% interest free loan applicable for loan with 2 years tenure.

Not only does choosing the right loan mean meeting your goals earlier, it also means that you can pay off your loans faster.

So while you’re all up for borrowing, be aware of the higher interest rates accounts that you’re liable to paying, so that you clear off those loans first.

Bali is known as the Island of The Gods. It exudes a unique cultural appeal, excites holiday-goers with its natural beaches and tantalizes foodies with its wide-range of culinary cuisines. It is little wonder that Bali is an extremely popular beach destination in South-East Asia. It would not be surprising if some of you have already booked a trip there for the upcoming summer holidays. Before departing for your holidays, don’t forget to purchase your travel insurance policy. Do ensure that your travel insurance policy contains “must-have” features such as medical expenses, emergency repatriation, trip cancellation/curtailment, baggage cover etc.

Travel insurance is important because it offers financial compensation during events such as travel disruptions. For instance, Moung Agung’s eruption in 2017 led to the closure of the airport for several days. As a result, additional hotel accommodation needs to be booked, flights rescheduled and some tourists even sought alternative modes of transportation. All these would add additional costs to your holiday budget. While travel inconveniences are entirely unpredictable, a travel insurance policy purchased in advance could partially offset some of these unforeseen expenses.

Many adventurous tourists visit Bali to try activities such as hand-gliding, para-gliding, diving etc. With its picturesque scenery, Bali boasts many adrenaline-filled activities for the sports junkies. You might want to consider getting travel insurance coverage before attempting these leisure activities. For instance, AXA’s SmartTraveller provides coverage for leisure activities such as parachuting, sky diving, bungee jumping etc. Having a travel insurance policy before attempting these leisure activities could provide an additional level of assurance.

Before embarking on your long-awaited getaway to Bali, it is therefore critical to be well-informed of the best travel insurance policies available in the market. You can compare travel insurance policies on SingSaver and directly purchase one that best suits your holiday needs. Comparing on SingSaver is not only convenient; it also helps you save money on your travel insurance policies!

Update: SingSaver is having a flash sale on 19 – 20 May 2018 on selected insurance products, including AXA, where the first 10 successful applicants in each hour (10am, 4pm, 10pm) get their travel insurance for free! For more details, click here.

Singaporeans looking to support their iPhone habit would do well to heed Apple’s release schedule

SINGAPORE, MONDAY 25 SEPTEMBER 2017 – Now that the iPhone X is straying perilously close to costing an actual kidney, trading in your old iPhone to help defray the cost of a new one is a more popular option than ever. But because the market has a tendency to push prices down when there are more people looking to sell their old iPhones (a well-observed economic principle – price goes down when supply goes up), you wouldn’t know if the trade-in price offered at your telco or handphone shop is a good deal or not.

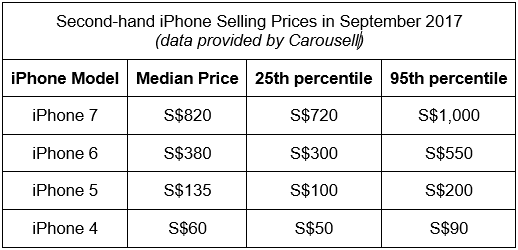

To help you avoid rip-offs, we asked everyone’s favourite online marketplace Carousell what your soon-to-be-replaced iPhone is worth on the second-hand market. Here’s what we found out.

What Do the Numbers Mean?

We apologise for triggering all the traumatic flashbacks of Statistics class you’re probably suffering right now. We wanted to make sure we dealt in scientific data, and not simply hearsay from a lazy walkabout at Tanjong Pagar Plaza. Quick explanation: The median price represents the midway point of each model’s price range. So in the case of the iPhone 7, 50% of all handsets were sold for more than S$820, and 50%, less than that. How much higher or lower? For that, we look at the numbers in the next two columns to the right. These give us a good idea of what low and high prices look like for that particular model. They do not represent the absolute lowest nor highest prices for each model. So, putting it all together: If you get offered S$800 for your iPhone 7, that’s a bit on the low side. S$850 to S$950 would be an ok price, and you shouldn’t hesitate to take any offers coming in at S$1,000 or more.

The Value of Older iPhones Declines Exponentially

Eyeballing the figures from Carousell, you can see that the value of your old iPhone suffers a dramatic decline after one generation. As at September 2017, an iPhone 7 commands a respectable median price. You’ll also notice that the spread between prices is still relatively tight.

But when it comes to an iPhone 6, the median price plunges by more than half. And it gets worse as we go down the ladder to older iPhone models, but you were probably expecting it anyway.

Actual Selling Prices Differ According to Condition

The actual price you will get for selling your old device will depend on a number of factors. Chief of these is the condition your handset is in. “While little scratches and scuffs aren’t deal-breakers – many of our users are upfront about these details and still successful in their sales – people will generally prefer and will pay more for iPhones in the best possible condition,” says Lucas Ngoo, Co-founder and CTO of Carousell. As you’d expect, a perfectly working model with all its original parts intact will fetch a higher price than one that had undergone part replacements. (Think about how damaged the internal circuitry must be after going through at shocks serious enough to shatter the screen.) If you can provide the original box and accessories (such as charging cable and adapter, and never-been-worn headphones) you can probably command top prices. And, because this is Apple we’re talking about, you can expect to charge a little higher for devices with larger storage.

Is it Worth Selling Your Old iPhone?

At this point, you may be wondering if it is even worth selling your old iPhone. The answer is: yes, especially if it’s the latest model. As Carousell’s data show, the iPhone 7 is trading hands at prices near to those of a brand-new set direct from the Apple store. This is probably as good as it gets. But even if all you have is an iPhone 6 or earlier, you can still sell it off and use the money to pay for other things you need or want. For example, while the S$60 you’ll get for selling your iPhone 4 puts nary a dent in what you have to pay for the iPhone X, you could still get a decent pair of shoes for it, or a new computer game.

A Result of Planned Obsolescence?

In case you’re not familiar with the term, planned obsolescence is an actual thing that manufacturers are doing. Basically, the products we buy are designed to last only up to a certain period. Beyond that, they are expected to fail. This practice corrals consumers onto a schedule for replacing the things that we’ve come to rely on. And it’s not just consumer electronics, car or light bulbs either. When it comes to iPhones, the message seems to be: keep up with Apple’s schedule; it’s the most rewarding way to enjoy their products. Especially in light of the record-breaking price of the iPhone X.