* Update 22/7: Abana Singapore announced in a Facebook post that they have restocked the drinks at 7-Eleven stores progressively today, while stocks last.

Yes, you heard it right.

One of Taiwan’s most popular bottled beverages 『純萃。喝』 will be launched in Singapore from 13 July. “純萃。喝” means pure and simple, just drink it.

The much anticipated drink in assorted flavours was launched in Hong Kong amid great fanfare, and was reported selling out at island-wide last year.

If you have been to Taiwan before, you might have spot this unique cylindrical bottle that looks like a shampoo or a comestic bottle — what is stored inside it, however, is something you must really try. There are 10 assorted flavours of milk tea and coffee that were launched and it includes varieties such as Mandheling, Sumiyaki (Roasted Coffee), Cafe Au Lait, Matcha Latte and more.

Abana Singapore Pte Ltd has been appointed to distribute『純萃。喝』in Singapore and will be launching two all-time-favourite flavours: Milk Tea and Latte.

It will be available at over 400 7-Eleven stores from 13 July, but we believed it won’t be on the shelves for long judging by its popularity and how it amassed a huge followings on their Facebook before launch.

It’s on a while stocks last basis and we don’t know how fast they’d be restocked, but that being said — don’t be too eager to raid their fridge as each bottle hasa shelf life of about 15 days.

『純萃。喝』 (Milk Tea/Latte) GIVEAWAY

Can’t wait to get your hands on these exclusive drinks? Good news. we will be giving away 2 bottles of『純萃。喝』 (1 x Milk Tea + 1 x Latte) to 30 readers.

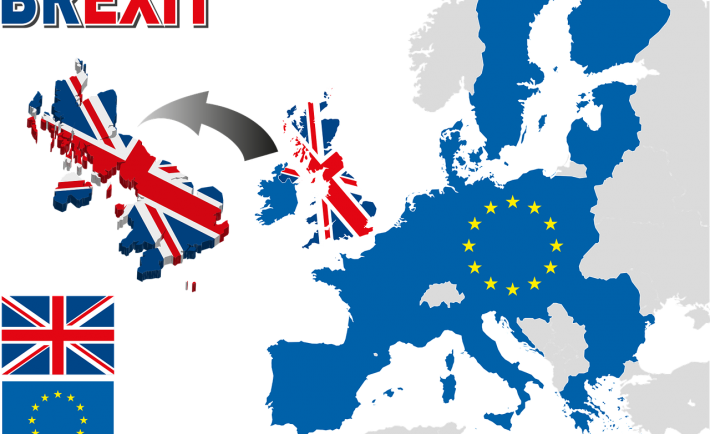

One of the most talked about issues surrounding the world today is the Brexit. Brexit is shorter term that refers to “British Exit”. It is the strong vote of British people to detach themselves from the European Union (EU). This referendum impacted the global markets including that of Singapore’s.

For starters, Brexit contributed to the changes in exchange rates as the value of Pounds drop in its lowest level in decades. Aside from this shift in currency, the Brexit has implications in Singapore’s trade, properties, and investments.

CURRENCY

The British Pound is in its weaker state – as of the moment.

To illustrate, imagine Sally is a Singaporean expat who moved to United Kingdom 6 years ago. Being financially savvy, she made a plan to save some of her money for retirement back home. Since Sally kept a relatively huge sum of money in Pounds, she was surprised to find out that her funds are worth less than they were a week ago.

Aside from the individuals like Sally, British companies are affected by the weaker British currency. It will cost them more money to grow and expand their businesses here.

TRADE

Unlike other ASEAN countries, the Singapore government has concluded their negotiations for “Free Trade” with the European Union. Within the Free Trade agreement, any imports and exports between EU and Singapore are more affordable and are subjected to lesser restrictions. This greatly helped our transactions as we imported over S$44.46 Billion worth of goods and products from the EU last year.

An issue floats as majority of our EU trade was with the Brits. There seems to be an uncertainty whether Britain will have more or less bargaining power over Singapore after the Brexit.

PROPERTY

According to Knight Frank, Singaporeans lead the list of Asian buyers who patronized United Kingdom commercial properties in 2015. With the prevalent clamor of Singaporean buyers and the ambiguity of the British market, banks such as UOB and DBS had to act quickly.

In a statement, UOB says that they “will temporarily stop receiving foreign property loan applications for London properties.” While, DBS is advising its lenders to be more cautious.

INVESTMENT

Behind Japan and Hong Kong, Singapore ranks third as the largest investors in EU. This is why the population of the Singaporean investors will be surely affected. In particular, a stock called GL Ltd (SGX: B16) encompasses more than 5,000 hotel rooms in London. If the British currency will decrease further, it can pressure GL Ltd’s profit in Singapore dollars.

Image Credits: pixabay.com

As a solution, experts suggest to diversify your investments in terms of currency exposure.

Let me close with the post that PM Lee Hsien Loong published in his Facebook page:

https://www.facebook.com/leehsienloong/posts/1142353405827364 “Singapore will continue to cultivate our ties with Britain, which is a long standing friend and partner. We hope in time the uncertainty will diminish, and we will make the best of the new reality.”

As a kid, I remember asking my father to get me a new toy even though I had plenty of it back home. He looked at me and told me that he cannot purchase it at the moment because “money does not grow on trees.” This old Proverb implies that it is not easy to earn money. However, the modern times enlightened me to a revolutionary realization.

I realized that there are simple, unique, and effective ways to earn money without having to commit loads of your time and exhaust your physical or mental abilities. Hence, I give you the 6 “Effortless” Ways To Earn Money…

1. SHOP FOR FREE

Ever dream of getting paid to shop? I know I had at it was amazing!

The people that shop for a living are called Mystery Shoppers. Mystery Shoppers are paid by the company’s marketing department to report about their experiences as they try the said company’s products, eat at their restaurants, or buy their goods. If you accepted a “mystery shopping” job, you will be paid for your time as well as be reimbursed for anything you bought.

Eager to be one? Check out the current job openings at Gumtree and Jobstreet.

2. ENJOY A GOOD NIGHT’S SLEEP

Sleep has been proven to improve concentration, increase cognitive function, reduce stress levels, and increase one’s Emotional Quotient (EQ). But aside from these, it can also increase your salary! An additional hour of sleep per week has shown an increase in salary by 1.5% over the length of a season. This increase is due to the positive effect of sleep on productivity.

3. DISTRIBUTE FLYERS AND LEAFLETS

You do not have to exhaust your physical and mental skills in order to distribute flyers and leaflets to others. A go-to side job by many students, distributing paper advertisements might sound like a boring task but you can earn decent cash (about S$7/hour) in a span of a few hours. Simply search at Gumtree to apply for this “promotional gig” near you.

4. COMPLETE SMALL TASKS ONLINE

If you have an hour to spare, consider joining websites that pay you for completing small and easy tasks such as signing up for websites, searching articles, making a background image, or linking URL to websites. Creating an account at Fiverr will only take you 5 minutes. With Fiverr.com, you will be paid a minimum of US$5 (S$6.70) for every project you accomplish. Alternatively, you can create an account at Microworkers.com to join more than 600,000 workers worldwide.

5. SELL YOUR PHOTOS

If you love capturing moments and have a collection of creative images that are worthy to be featured on websites then, you can try selling your photos online. Companies are in constant need for images for their websites, brochures, cards, blogs, and other projects. Start by selling your stock photography on Shutterstock or Fotolia. Each website works differently so read through the guidelines first before you commit.

6. GET PAID TO TWEET

If your overactive Twitter page boasts with a relatively large following, you can get paid for posting sponsored tweets to your followers. The rate, which typically ranges from S$0.67 to S$26, depends on the number of your followers as well as other factors such as the creation “age” of your account. An example of this service is manifested by paidpertweet.com.

When you hear the term “Critical Illness Insurance”, what comes to your mind?

If you are envisioning a coverage which offers a payout when the policyholder is diagnosed with a critical illness (e.g., stroke or cancer) then, you are correct!

Critical Illness Insurance or Dread Disease Policy is a lump sum payout given in the event that the policyholder is diagnosed with one of the specific illnesses covered by the policy. It can either be sold as a stand-alone policy or a part of a main policy in life insurance or investment insurance. The guidelines and definitions of the 37 critical illnesses are predetermined by the Life Insurance Association of Singapore. This definitions are fixed across the board.

Unlike other forms of health insurance, the benefits of Critical Illness Insurance is paid out in lump sum so that the person can use it not only for medical expenses but also for other living expenses that can result from the ongoing treatment.

COMMON FEATURES

Here are some of the usual features of the Critical Illness Insurance:

1. Its premium is adjusted based on the policyholder’s age-band.

2. The policyholder is allowed to claim no more than one of the critical illnesses listed.

3. There are no restrictions on the utilization of the benefit payment.

4. The critical illness rider will be terminated once you give up the basic policy.

5. A type of health insurance (with a critical illness rider) has an expiration once the policyholder reaches a maximum age.

6. To reduce the risk of moral hazard, there is a limit on the total amount that you can purchase.

7. Upon purchasing the Critical Illness Insurance, there is a waiting period before you can make a claim.

POSSIBLE ISSUES

Given the fixed definitions of the critical illnesses as well as the common features of the Critical Illness Insurance, there are several issues that can possibly happen in different situations. For starters, the benefits can only be paid if the disease EXACTLY meets the standard definition stated by the policy.

For example: Coma is defined as…

“A coma that persists for at least 96 hours. This diagnosis must be supported by evidence of all of the following:

• No response to external stimuli for at least 96 hours; • Life support measures are necessary to sustain life; and • Brain damage resulting in permanent neurological deficit which must be assessed at least 30 days after the onset of the coma.

Coma resulting directly from alcohol or drug abuse is excluded.”

In reference to the definition above, say your beloved spouse had been in a state of coma for the past 48 hours due to substance abuse and you cannot do anything about it because he is not qualified to claim the insurance payout. It will be difficult for you to fork some money at a relatively short notice.

Another issue that can happen is when two or more diseases transpire (co-morbid diseases) and you can only claim for one of it.

Image Credits: pixabay.com

Furthermore, claiming of the benefits usually has a waiting period. If a critical illness is carried out during the waiting period then, you cannot be paid for its benefits.

Is it possible to live in a world where you can carpool with a stranger during an emergency? How about dining at someone’s home or hiring an experienced chef with a swipe of a finger?

With a “sharing economy”, all these are possible!

According to Investopedia, a sharing economy is…“an economic model in which individuals are able to borrow or rent assets owned by someone else. The sharing economy model is most likely to be used when the price of a particular asset is high and the asset is not fully utilized all the time.”

United States, Europe, Seoul, Australia, and other parts of the globe have shifted from a consumer market to a sharing one. In these places, people use technology to rent, lend, and exchange goods and services rather than purchasing them from shops or companies. Considering the scarcity of some resources in the country as well as its technological advancements, experts suggest that a sharing economy is an untapped realm with great potential for Singaporeans.

April Rinne, a consultant and World Economic Forum Young Global Leader, expressed that a sharing economy can help a society to become more sustainable. And is it not what Singapore aims to accomplish?

In fact, in the Sustainable Singapore Blueprint 2015, the state set up a collective vision that includes being a zero waste nation by 2030. A sharing economy fosters activities that enable people to share and earn income from underused assets such as apartments, cars, clothing, and tools.

There are several benefits that a sharing economy can bring to a nation such as reducing environmental waste impact, redefining the materialistic ideal, increasing efficiency in transport, as well as cutting energy and water consumption.

Sharing economy helps to reduce the environmental waste impact and extend the longevity of items. For example, The Freecycle Network™ allows people to give and receive re-usable items to divert them from the landfills. 9,104,727 users post ads of pre-loved items and give them freely to people that would want to take it. Interestingly, I saw one post from Singapore that offered “lofted twin beds with desks underneath”.

A sharing economy also helps to redefine our materialistic ideal as it encourages to sell or share our possessions. You see, we grew accustomed of having material goods as a measure of success. We believe that the more we have, the more society will perceive us as wealthy and happy. But the truth is, having all these designer goods or lavish cars will never satisfy us. It will only make us craving for more. In a sharing economy, you can easily buy and rent clothes online.

Aside from sharing our possessions, a sharing economy supports the idea of community transportation. By community transportation I mean that people can rent cars from companies, carpool with strangers, and pay for a ride from the people in their neighborhood. A good model for this is Uber. Uber allows you to get a taxi or share a ride with other people through a mobile service.

Lastly, a sharing economy allows you to cut on the accommodation costs as well as energy and water consumption thru services like Airbnb and Couchsurfing. In 2014, a study found that sharing homes had considerably lesser energy and water consumption, greenhouse gases, and accumulated waster compared to hotels. The current situation of home sharing in Singapore depends on the Urban Redevelopment Authority (URA). The URA is re-assessing the law which considers that it is illegal for an individual to rent out their home for stays shorter than 6 months.

Image Credits: pixabay.com

For individuals, companies, and the society at large, a sharing economy presents a myriad of opportunities to invent new streams of revenue, solve social issues, and to create community resilience. If this idea is successfully achieved, Singapore can just boost its productivity levels significantly.