Describe your job to your children. You may even bring them along one in your workplace and give them a tour. Then, introduce this video of a farmer that gets paid for supplying milk. This short video explains the concept of money to children in a simple and animated manner.

2. MONEY IS NEEDED TO PURCHASE THINGS

Like the farmer in the video, he needed money to buy what he wanted. Help your child understand the concept of being able to buy things by identifying items that cost money (e.g., house, car, table, or iPhone) and those that are free (e.g., hugs and kisses from Daddy).

3. THERE IS A DIFFERENCE BETWEEN NEEDS AND WANTS.

When you are shopping with your kid, highlight what are the essentials such as vegetables and fruits. Then, let your him pick the items that are considered as wants.

Tell your child that an individual must wait before buying something he/she wants. Make him realize this by putting money into two jars: 1 for savings, 1 for spending. Ask him to save a dollar of his allowance for savings and a dollar for spending every week.

Aged 6-10

4. IT IS GOOD TO COMPARE PRICES.

Teach your child how to look around the shops first before buying anything in order to get the best deal. In spending money, choices must be made. So, include your child in small decisions to increase their awareness.

5. THERE ARE DANGERS IN SHARING PERSONAL INFORMATION ONLINE.

Discuss to your child how dangerous and costly it is to enter personal information (e.g., address or bank account details) online because someone may steal it. Encourage purchasing online only when you are beside them.

6. INTRODUCE BANKING AND INTEREST.

Describe how the banking and interest works. Savings account will protect your child’s savings and it will also generate more money due to interest. You may open a junior bank account that you supervise. Let your child watch this video to understand the concept better:

There are two types of people in the world: those who spend and those who save.

SPENDERS

Compulsive spenders do not want to delay gratification. If they want something, they will purchase it right away…as long as they are happy. It worked so well in the past, so they stick to the same habit. But, when expenses and debts extremely increase then, it is the time they realize that they need to kick that habit away.

Here are 3 ways to prevent your impulses and to help you save:

1. IDENTIFY YOUR FINANCIAL GOALS

How much do you need when you retire or how much do you need to pay for your child’s education? Ask yourself these questions to identify your financial goals. Then, be vocal about it to your friends and family.

2. NEED VS WANT

Before purchasing anything, evaluate and know whether you need or want the item. Then, purchase according to your budget.

3. STAY AWAY FROM THE PLASTIC CARDS

By using mainly cash and withdrawing it from your bank account, then you became more aware of your spending and your account balance.

SAVERS

For financially aware individuals, the act of spending can activate neural activity in the anterior insula and amygdala. These two parts are responsible for the mood and unpleasantness felt. This is why the more these two are activated; the less likely a financially aware individual will spend. On the other hand, the act of saving will bring immense pleasure to them.

While many people take pleasure in purchasing things, some savvy savers do not feel the same. Instead some of these people are uncomfortable when shopping, they constantly look for the price tag and calculate the total, and they feel emotionally painful when they are paying. If you are not experiencing enough pleasure in life, you deserve to loosen up and enjoy spending every once in a while.

So, what brings the pleasure back as a savvy saver that is spending?

1. STAY AWAY FROM THE PLASTIC CARDS

Give yourself the vacation or rest day you deserve by budgeting a portion of your money to a category called “personal incentives”. With that money, you would not need to use your credit or debit card since you have already set aside the cash to cover it. Now all you can do is relax and take your mind off the expenses.

2. PURCHASES=REWARDS

At the end of the month and once you meet your savings goal, reward yourself with the pampering you deserve for working hard and doing so well. To prevent frugal fatigue, reward yourself by using a responsible amount of 4% – 8% of your savings.

3. THINK OF THE FUTURE

Study has shown that people are happier when they spend their money on experiences (e.g., sky diving) than in goods (e.g., Gucci bag). So, do the same with your personal incentives. Do you really want to regret experiences you did not take because you don’t want to spend money on enjoyment?

Image Credits: Tax Credits via Flickr

Even though you belong in one category now…you can still change! Whether you are a saver or spender, you hold your financial present and future.

It is amazing to start the Lunar New Year with a clean financial slate and increased savings. So, begin the year with a 2015 spending cleanse: short yet impactful exercise to help you clear your mind, focus on your goals, and improve your buying habits. There are no excuses because a short-term intervention (7 days) is a good place to start.

In just a week, your financial awareness can help you stop spending on unnecessary items and eventually help you break the bad habits. Try these 3 Spending Cleanse Ideas and come out more motivated, focused, and richer.

You must first figure out a budget plan that helps reach your financial goals before starting the cleanse. Seek guidance from family, friends, or YouNeedABudget.com.

1. ELIMINATE THE UNNECESSARY

Plan: Identify a category where you are overspending then, slash that problem area.

Purpose: To allocate more money for shopping, emergency fund, and savings.

If you a person who does not pack for lunch and only go for local restaurants, gourmet counters, and coffee shops everyday then your expenses can take about S$450 of your income. With this cleanse, you will have to go on cold turkey and avoid buying for outside food for 7 days. You will find yourself save more afterwards.

Just by reducing expenses in one category such as switching back to basic cell phone plan; you can save up for your dreams in just a few years. It is so simple! There is no sense if you go back to your unpleasant ways.

2. HAVE AN “AUTO-SAVE” SYSTEM

Plan: Program regular account transfers to help you reach your goals while having a busy schedule.

Purpose: To save money for retirement, emergency fund, and vacations before you spend it all.

Contemplate upon your budget and begin writing a list of the things you want to save for from your needs (e.g., emergency fund) to your wants (e.g., Christmas vacation in Paris). Divide your income to the needs first then, divide what is left to your wants. You need at least two bank accounts: one for your needs and one for your wants. The next step is to set up automatic transfers or direct deposits that will move your money into each account on payday.

3. NO MORE PLASTIC CARDS

Plan: Withdraw the week’s spending from the bank in cash. When it is gone…it is gone.

Purpose: Saying no to credit cards will cut down the impulse purchases.

Most people talk about how important their long-term financial goals are but their regular buying decisions do not support their goals. This cleanse will have you keep your credit and debit cards at home so you can easily notice when you are losing money for every purchase. Before the week begins you must spare 25% of your income and divide it to your spending categories and put all in different envelopes.

Image Credits: wikihow.com/Do-Envelope-Budgeting

This will be your only allowance for the whole 7 days and all for purchases shall only come from it. Research showed that the act of relying to cash for spending makes you savor the paying process, think more, and spend less. Trust me, it works.

After days of Chinese New Year, many of us feel “richer” after collecting red packets from your parents and relatives. (For those that gave out red packets, i hope your rubbed shoulder with God of Fortune and got your windfall) Now as you hold and sniff your stacks of new notes, you may be thinking of the best place to put away this sum of money other than your tin can or under your pillow. Should you just deposit these money to your standard POSB/DBS account?

We take a look at the banks you should be putting away your money with, which includes fixed deposits and your daily saving accounts.

1. POSB

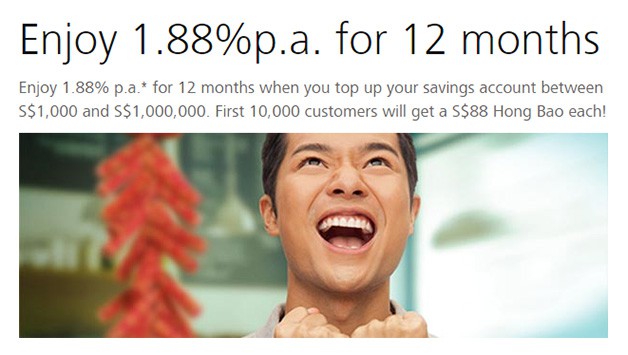

If you are not aware, POSB launched a cash gift promotion of 1.88% for 12 months on 23 January 2015. What this means is that any single sum deposit between SGD 1,000 to SGD 1,000,000 to your saving account will earn you an interest of 1.88% for 12 months. The catch is you cannot withdraw these top-up amount during this 12-month period.

Note: You must sign up before 28 February 2015 to be eligible for the promotion.

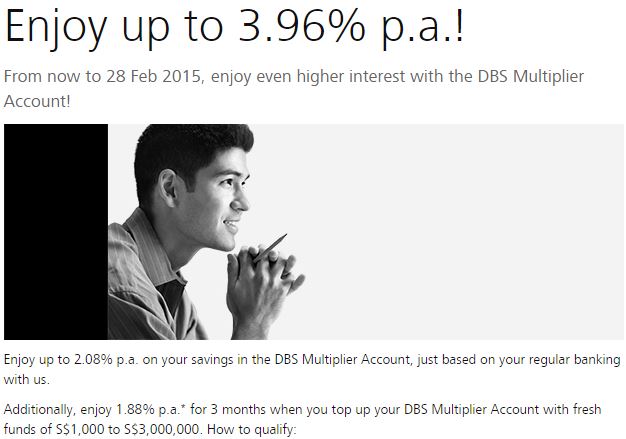

DBS launched the same promotion earlier this month for customers who deposit SGD 1,000 to SGD 3,000,000 can earn an additional 1.88% p.a for 3 months on top of the 2.08% of their DBS Multiplier Account. Likewise, you need to register with them by 28 February 2015 and make a one-time top-up to be eligible for the promotion. You will need to hold on to the fund for 3 months.

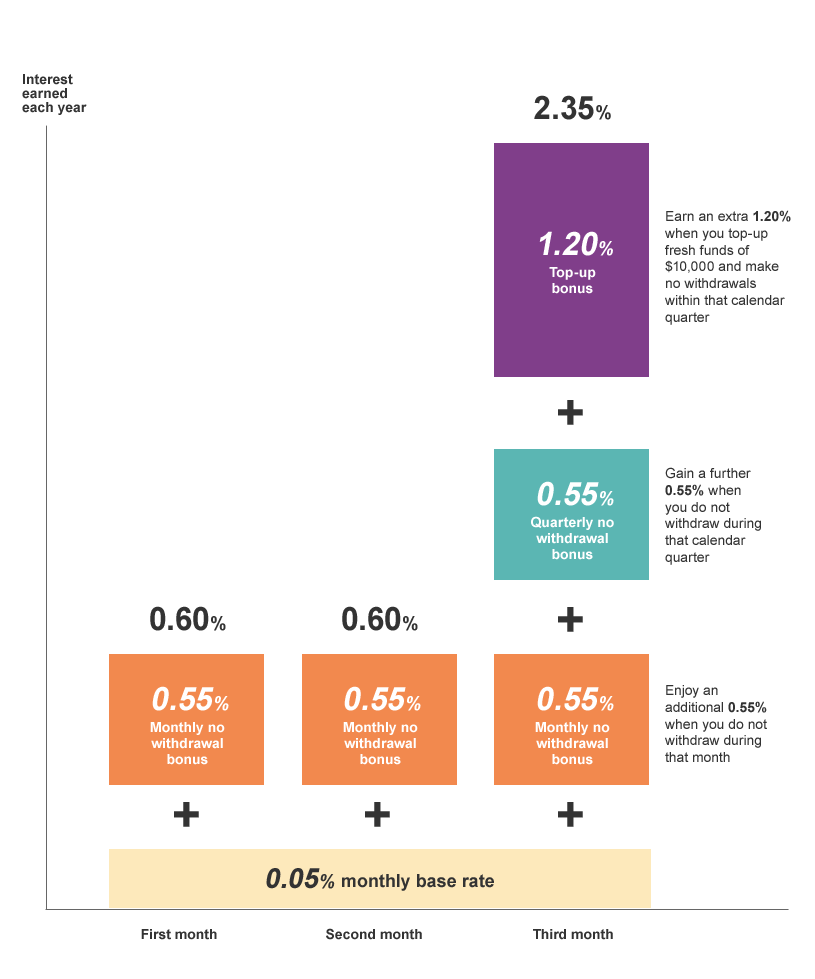

For those who makes a larger deposit of fresh funds of SGD 10,000 and more can consider OCBC Bonus+ Savings Account with up to 2.35% p.a. All funds will earn a base interest rate of 0.05% p.a if no withdrawals are made. If no withdrawals are made in a month, you get an additional 0.55% p.a. Get an additional 0.55% p.a if you do not withdraw in that calendar quarter and a whopping 1.20% p.a top-up bonus if you deposit $10,000 of fresh funds. (0.05% + 0.55% + 0.55% + 1.20% = 2.35%)

For Premier customers, you get an additional 0.05% p.a on each tiers which means you could earn up to 2.50% p.a.

For a 12 month Time Deposit, earn up to 1.40% when you deposit a minimum of $20,000 in fresh funds.

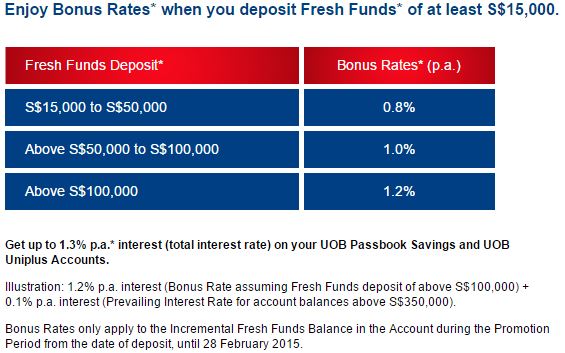

Enjoy bonus rates of 0.8% p.a when you deposit fresh funds of at least $15,000. If you deposit fresh funds of $50,000, you will get 1.0% p.a bonus rates and 1.2% p.a if you deposit $100,000 and more. Get an additional 0.1% if your account balance is above S$350,000.

Receive a limited edition 24K Gold-Plated RISIS Magnificent Goat Figurine (valued at S$238) with S$108,000 fresh funds deposit*.

This UOB Lunar New Year Savings Promotion ends on 28 February 2015.

* For those who want a higher rate can opt for their SGD Fixed Deposit, where you can get up to 1.30% p.a with a 13 month tenor and a minimum of SGD 20,000. Promotion ends 28 Feb 2015.

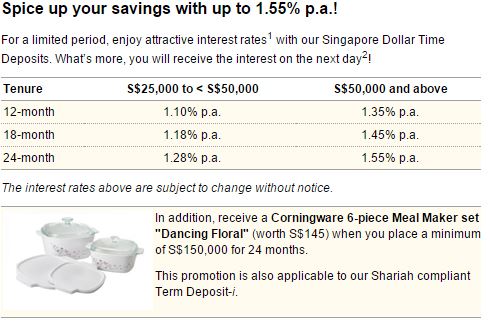

Maybank offers more choices for their Time Deposit plans and the interest rate varies depending on the amount and tenure of your deposit. From S$25,000, you can get 1.10% p.a if you can lock away for 12 months and can go up to 1.28% p.a if you can stretch longer to 24 months. If you have double the amount (S$50,000 and above), you fall into the higher tier and can receive up to 1.55% p.a for a 24-month Time Deposit.

If you deposit S$150,000 for 24 months, you stand to receive a Corningware 6-piece Meal Maker Set “Dancing Floral” worth S$145.

Deposit a minimum of $25,000 to get an interest rate of 1.25% p.a for their 12-Month SGD Fixed Deposit Account. For larger amount deposit of $250,000 and more, you will receive 1.30% p.a. That’s not all, depending on the amount of fresh funds you deposit, you stand to receive a New Moon Abalone Set.

Register no later than 5 March 2015 to be eligible for the promotion.

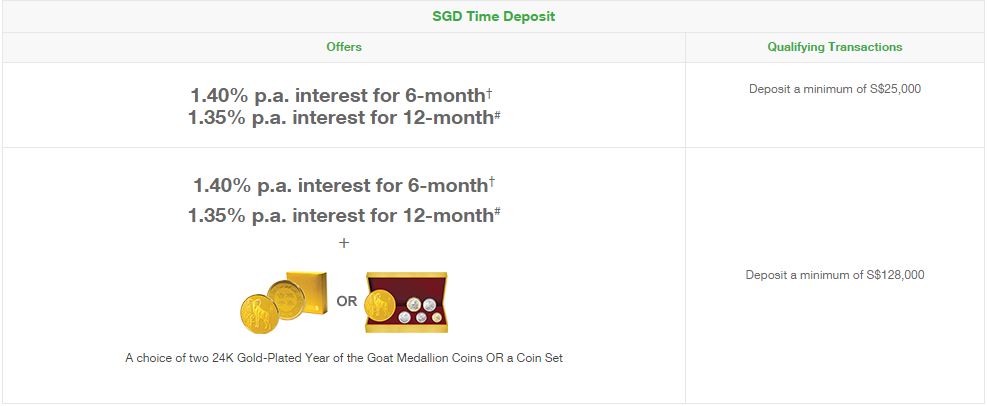

Deposit a minimum of S$25,000 and get up to 1.40% p.a for 6-months and 1.35% p.a for 12 months. For larger amount of S$128,000 and more, you stand to receive a choice of two 24K Gold-Plated Goat Medallion coins OR a Coin Set. Promotion ends 28 February 2015.

* For those who want to deposit a smaller amount (with no min deposit) and no tenure can opt for their e$aver Account where you stand to earn an interest rate of 1.35% p.a until 31 March 2015. More info: http://goo.gl/18oKdx

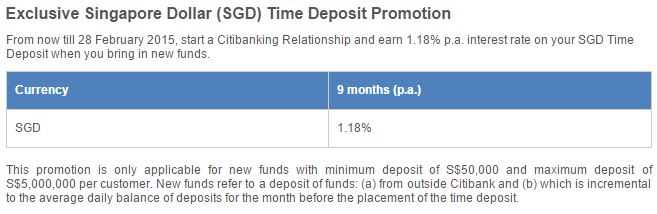

8. Citibank

Want time deposit with a shorter tenor? Then go for Citibank’s 9-month Time Deposit and receive an interest rate of 1.18% p.a. You will need to deposit a minimum of S$50,000 and up to a maximum of S$5,000,000 of fresh funds. Promotion ends on 28 February 2015.

Read and understand materials about self-empowerment, investment, and money management. Here are four books to get you started with:

“The War of Art” by Steven Pressfield

“Why Stocks Go Up and Down” by William Pike

“The Intelligent Investor” by Benjamin Graham

“Turning Pro” by Steven Pressfield

2. CONNECT AND DISCONNECT MORE.

Networking is very important especially if you will be dabbling in the field of business. Meeting people with shared interests will not only bring a life of fun but also a life of opportunities. Your network may refer you to your first job or even challenge you to be a business partner. On the other hand, you must disconnect with the distractions such as excessive amounts of alcohol or other vices that are harmful to your body.

IN YOUR 30s

3. BEGIN NOW.

The sooner you start, the more money you part with. In order to retire on 80% of an income, a 30-year-old must save 10% of his or her salary.

4. INVEST IN STOCKS.

Even if the economy suffers badly, your account will have time to recover. For instance, The Fidelity Select Software and Computer fund has yielded more than 11% a year since 1996. Keep it basic with a low-cost index fund.

IN YOUR 40s

5. PUT VALUE TO YOURSELF.

You may want to put your retirement savings into hold because of your child’s college fund. But, keep in mind that you cannot load for retirement yet you can loan for college fees or even get a scholarship.

6. SEEK THE EXPERT’S ADVICE.

To reach the maximum level of your retirement savings, sit down with a financial planner. Create a financial goal together and learn how to save more, spend wisely, and invest to reach it.

IN YOUR 50s

7. STAY WITH STOCKS.

You may increase your percentage of savings by investing in bonds but do not totally quit on stocks. To battle inflation, you must lean on the stocks’ higher growth potential.