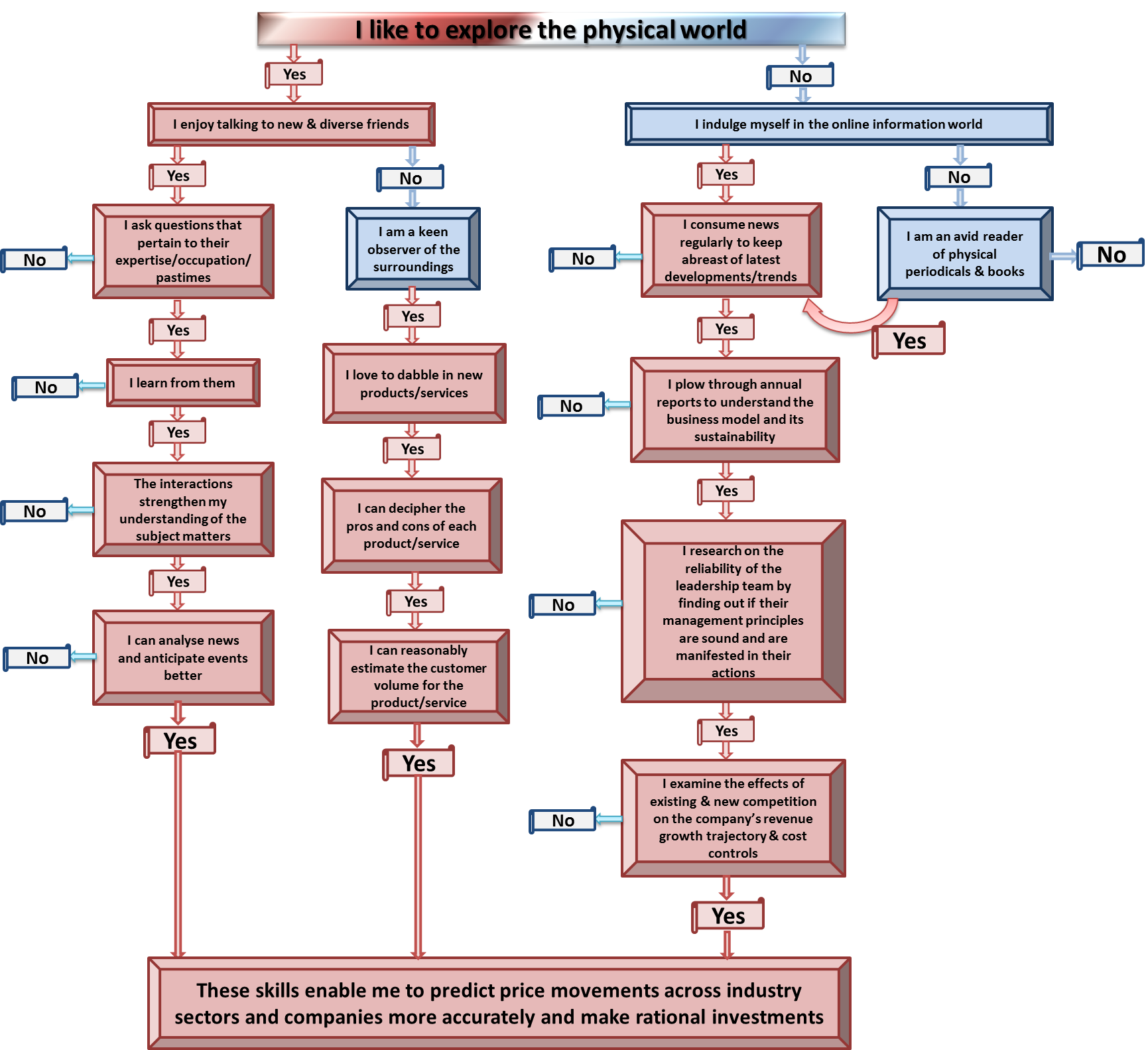

Investment books often urge readers to do extensive research to identify megatrends such associal and cultural shifts that could make a potentially big difference in investing decisions. However, the real answer is never simple. The ideal way to value anything, including company shares, would be to plug yourself entirely into the real world, which means shaping your daily behaviours such that it enables you to maximise your exposure and learning about almost everything.

Given the increasing connectedness of the world and the rapid explosion of information, learning is no longer confined to any one medium or source. Therefore, keeping an open heart and mind is in reality the best bet to a lucid understanding of the dynamic and complex interactions across companies, industries and countries.

The flowchart below illustrates the types of personal behaviours that may help individuals to hone their stock investment skills.

I’m going to share some of the ways that you can allocate your portfolio according to the different amounts of money that you are able to invest (those above your emergency fund and not needed for any big-ticket purchases).

Straits Times has done a similar article on this topic, How to invest if you have $20k or more (19 Jul), but I disagree with some of their recommendations (especially since I don’t really like the idea of unit trusts and prefer index funds)

If you have around:

$10,000 (or less) to invest….

100% Index funds or ETFs

You can place your money in index funds or an exchange-traded funds (ETFs), the latter can be bought and sold on the SGX like shares, but some of the funds are specified Special Investing Products (SIPs) and would require you to meet some criteria. This would give you diversification as investing in the fund will give you exposure to the different shares in the fund.

For example, investing in an index fund that tracks the Straits Times Index (STI) will spread your capital across the 30 shares that make up the STI, according to the size of the market cap of each company as the STI is a capitalization-weighted index.

$50,000 to invest….

60% Index funds or ETFs 40% Stocks or REITs

Instead of investing in index funds or ETFs, if you are more adventurous, you can try investing in individual companies or REITs (but I think it’s still good to keep a good part of your portfolio in index funds or ETFs). Picking out individual companies will require a bit more time to research the companies on your own to pick out the good from the rest. The ability to pick out good companies will require some experience to master, but the potential returns will be much better than investing in index funds or ETFs if done well, but don’t try to do so if you’re not willing to put in time to learn and research as you may end up only paying “tuition fees”.

$100,000 (or more) to invest….

70% Stocks or REITs 20% Bonds 10% Cash

With this amount, you may be able to purchase all of the 30 shares in the STI on your own to avoid the expense ratios of index funds and ETFs and another advantage would be getting dividends as the companies pay them instead of waiting for the funds to pay them out. You may still incur some minimum brokerage charges if you try this, but if held over a long enough period, this would be cheaper than using index funds or ETFs.

Another advantage of not using index funds and ETFs at this point is the ability to buy shares that you think may outperform the market. Let’s say you think that the finance sector may not do so well in Singapore, you can cut out the finance stocks, such as DBS, UOB and OCBC, and go for the companies that you think will outperform the market.

You may also want to keep some of your portfolio in bonds and cash as well to better protect your portfolio should the market enter a downturn, you still have an income and cash to take advantage of the drop in share prices to buy into the market at the cheaper prices.

I think that this is a good way to invest if you have above $100,000, unless you have amounts in the millions in which case I have not much idea of how to invest in that region.

Summary

Overall I support index funds and ETFs as a good way for people with smaller portfolios to be able to access a wide diversification across different shares in the index that the fund covers. (You can see my post on indexing at: Thoughts on Indexing) As your portfolio grows, you may want to move into individual shares as they offer the potential for better returns and with your larger investment, it would make more sense to spend more time researching the companies (amount earned over time is higher).

When investing in the market, you may also want to practice dollar-cost averaging to ensure that you do not enter the market at too high a price and get your fingers burnt when the market drops, but don’t invest too small amounts such that you spend a large amount of your money on minimum brokerage fees. While it’s good to diversify to reduce your exposure to any one company, investing in too many companies dilutes the returns of the “winners” that you have chosen.

A place where you can securely reside with your loving family – that is what you call a home.

Since land is scarce in Singapore, properties had always been a go-to investment tool for many. The majority of these investors have strategies limited to purchasing, reselling, and renting flats or condominiums. But, in order for higher returns to generate, one must consider investing to a range of other properties such as using the Real Estate Investment Trust (REIT).

And for a beginner with merely S$10,000 on hand, is property a viable and smart investment tool?

PROS

1. GETTING MORE LEVERAGE

With the banks help, you can have the ability to leverage your capital, make a down payment, and increase your overall return. Simply, more leverage enables you to pay less money upfront (e.g., 30% down payment and 70% from the bank) while making more money in the process.

2. CAN BE A SHIELD AGAINST INFLATION

Inflation occurs when there is a spike in prices and fall in the purchasing value of the dollar. As the miscellaneous for the property increases, the rent, and its value also increases. This is why property investing can be a good shield against inflation.

Image Credits: .Martin. via Flickr

CONS

1. CAN BE TIME CONSUMING

Finding a property in a decent location, building a good relationship with the tenants, and maintaining the condition of the property can be time consuming. Time that may not be in the good side of most.

2. THE RISKS ARE HIGH

A two-bedroom HDB flat can cost about S$250,000. That is a huge sum of money you may be willing to risk if you are serious in property investing. The risks only increase when the investor does not understand how the property market works or when and where to invest. Hurrying up without analyzing the situation thoroughly can only bring about more damage (e.g., bankruptcy) than good.

ULTIMATELY

You can lower the risk of property investing by diligently researching and analyzing reports, tests, and the current situation. Furthermore, investing in below market value properties backed up with insurance can help manage the risk. You would not know all these things unless you are well informed!

A buyer with an in-depth financial knowledge is important to the success of a property investment. So, if you lack sufficient knowledge, seek advice from a financial consultant or other professional advisers. And, when you find the “right property”, ensure that you keep your expectations realistic and keep your finances in tact.

DISCLAIMER: THIS ARTICLE DOES NOT FORM PART OF ANY OFFER OR RECOMMENDATION, OR HAVE ANY REGARD TO THE INVESTMENT OBJECTIVES, FINANCIAL SITUATION, OR NEEDS OF ANY SPECIFIC PERSON. BEFORE COMMITTING TO AN INVESTMENT, PLEASE SEEK ADVICE FROM A FINANCIAL CONSULTANT OR OTHER PROFESSIONAL ADVISER.

Singapore may be the world’s most expensive city, but to lead a reasonably comfortable life may not be impossible. It takes significant forward planning and a strict adherence to one’s investment principles to achieve a desirable outcome. This article – the third in a five-part series that continues from “How to maximize your life with a $3,000 paycheck”- will thus explore the different ways to diversify and maximize your returns on a $1,500 monthly “investment budget”.

Image credit: blog.propertyguru.com.sg

Property

A home not only provides a physical shelter, but also instills a sense of belonging and emotional attachment in the members of a family. Therefore, this prized asset is arguably the main driving force that motivates people to work hard and tirelessly, which forms the bedrock of our prosperous society. At the same time, it makes sense to allocate a lion’s share of the investment budget equivalent to 40% or $600 to property. Given that 23% of the wages that are allocated to the Ordinary Account can be used for housing, which thankfully exceeds the regular 20% employee’s CPF contribution, no further action needs to be done to set aside any disposable income for the property budget. Since the CPF savings in the Ordinary Account yield a guaranteed annual interest rate of 2.5%, this should form the benchmark on which the returns of the alternative investment vehicles shown below are based.

Image credit: gelvininfotech.com

Stocks

Evaluating a stock is akin to evaluating your potential life partner. You need to understand it well before you are able to pass a well-informed judgment – to buy, sell or keep in view. And for most working adults, time constraint is a persistent bugbear. But keep your heads up. You just need to stay focused on certain options (both in the arenas of investment and love). Choose the industry that you are familiar and confident with – especially if you are working in that sector or make friends in the sectors that you are interested in – and share the exclusive knowledge and expertise with your selected group of friends to leverage on the pooled insights. Besides that, running checks on the consistencies of the historical dividend yields and the shareholding information of the top management executives of the publicly listed company is pivotal. These track records offer an ultimate backstop when things go awry by providing “consolatory recurring dividends” and a “management confidence boost” (assuming that these companies are content with the status quo). Allocate 35% or $525 monthly to your share investment budget. Engage in the due diligence process while gradually building your ammunition to purchase stocks that offer at least 2.5% dividend yield.

Image credit: pondicherryurbanbank.in

Fixed deposits

While most fixed deposit interest rates are considerably lower than 2.5% and grimly sufficient to beat inflation, it is nevertheless a secure source of income, especially during a recession where stock prices and incomes are falling. Moreover, it offers flexibility as you can decide on the tenure of your fixed deposits that ranges from 30 days to 10 years. Therefore, cap your downside risks by designating 15% or $225 to fixed deposits and be assured of the steady returns to this investment.

Image credit: forbes.com

Savings account

Saving up for a big ticket item like the upcoming iPhone? The remaining 10% or $150 should not be tied up in any illiquid investment vehicles. It is a good financial management practice to reserve a small portion of the investment budget every month for the pursuit of the latest trends or luxury indulgences instead of bursting your credit card limits on such occasional treats.

While these measures may not propel you to the top 10% of the Singapore’s population, they serve as a general guide to better manage your finances. As always, sheer hard work and discipline rule the day.

While i love the amazing skyline from Victoria Peak, what got me excited were not the insta-worthy photos i took or the dim sum i gobbled down at Lung King Heen.

It was the fact that i actually travel for free.

Free? Does it means that i won a free trip to Hong Kong or had my travel sponsored by a company?

Good guess, but nope!

Well, the trick here is about planning my own finances. I couldn’t have included Hong Kong into the list of places to visit without exceeding the budget i set aside for this year.

A few years ago when i was still a student, i didn’t care too much about my own finances since i was spending within my means. Like many others, I had my money stashed away in a POSB’s saving account. Who care about interest rates when we hardly have five figures in our possession? The returns were pittance that it hardly warrant any extra attention.

My attitude changed when i had friends who were boasting about how much money they were making. I told myself i wanted to be like them — to be rich, in the shortest amount of time.

It seems then that the only way is to investventure gamble into the stocks market. I had no idea where to start until one day i was approached by a financial adviser when i was exiting the MRT station. And being a ambitious and impulsive young adult, i was persuaded into buying a saving plan that invests into the market with some kind of insurance cover that comes with it.

It felt good even though i had no idea what i was buying into – the feel good factor that i am now investing like an adult.

I call in to check on the policy every month, but apparently i was told that it is still in the early stage and had little or no cash value.

After a few months i gave up because it hardly grows and sadly i was told that if i were to terminate the plan, i would end up with almost nothing.

The change

From then on, I told myself that no one else can manage my own finances except myself. I need to take the responsibility or i will be the one suffering down the road.

I spend months reading up on books, forums, MoneySense and any resources that i could laid hands on. I begin to understand the importance of budgeting, investing and how to manage my own finances.

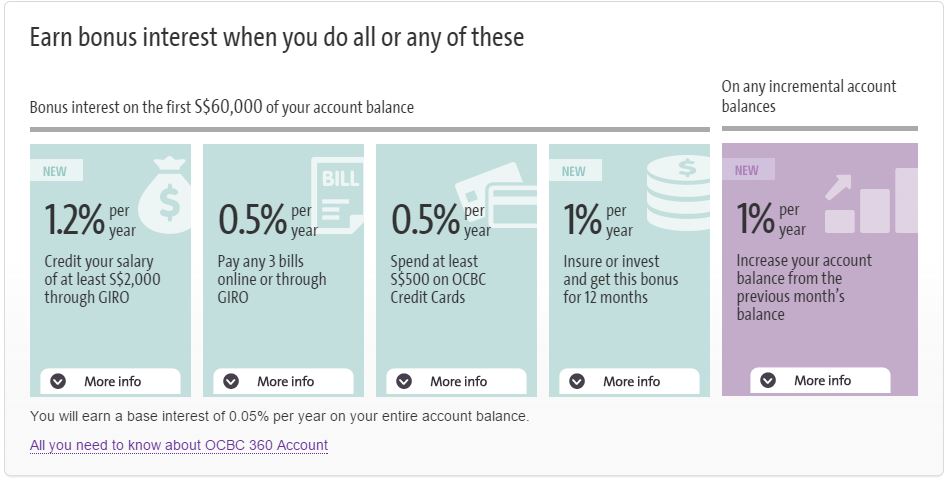

I started by switching my funds to a higher interest-bearing account such as the OCBC 360 where customers could potentially earn up to 3.25% as at 1 May 2015.

It was also then that i realized that previously i was holding on to an investment-linked plan which comes with high fee and charges. It is not cost-effective to achieve my goals and i had to take the hard decision to surrender and make a loss.

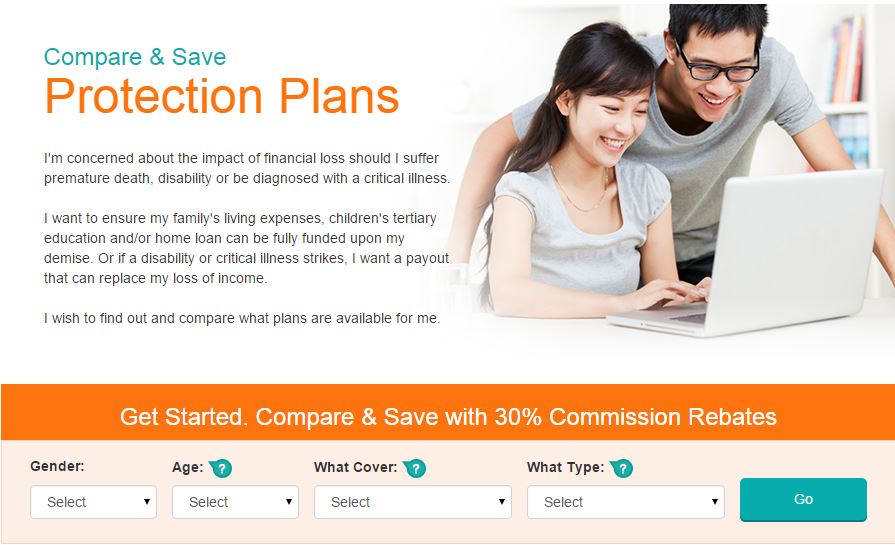

A better way that i learnt is to buy term insurance and invest the difference. Term insurance is cheap and affordable although it does not have cash value. But the difference i could potentially save could be put into better investment vehicle such as the low cost fund that tracks the Straits Time Index (STI) which has a historical return of around 8 per cent in the long run.

I was introduced to the online platform DIYInsurance — a portal which allows me to compare the different term insurance plans out there. What appeals to me is that they rebate 30% of the commission back to the customer and at the same time still make an effort to go through the planning process, making sure that the person is on the right track.

They have a live chat system where i can ask any questions on how to use the online platform, as well as clarifying with the client services manager on the semantics of insurance definition. It was fuss free and it beats the inconvenience of holding on to the line when you call in to financial institutions for enquiries.

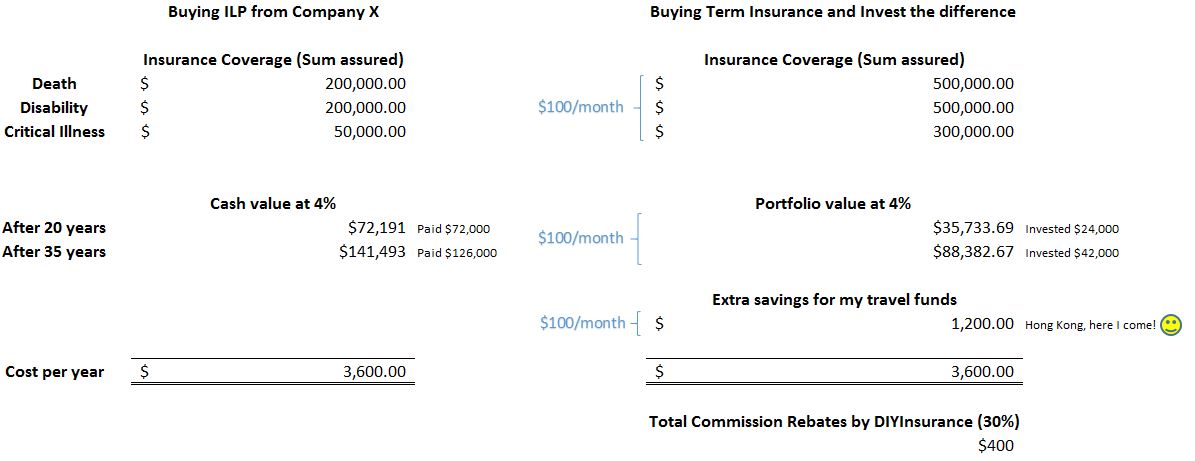

If you are wondering how much money i save using the DIY method, i have done up some numbers for comparison.

(Click to enlarge)

As you can see, i was previously paying $300 a month for a $200K cover on death and disability and a $50K rider on critical illnesses. If the funds grow at 4%, it will take me 20 years to break even and 35 years to make a small profit of $15K. (calculate the ROI)

If i were to employ the alternative strategy of buying term and investing the difference, i’d be merely paying $100 a month for a $500K cover on death, disability and $300K on critical illnesses. The other $100 will be channeled to a low cost fund, and assuming it grows at the same rate, my portfolio would be sitting at a value of $35K after 20 years or $88K after 35 years. (note that i’m contributing 2/3 of what i’d have otherwise contributed to the ILP and i have pegged its growth at 4% for comparison purposes)

As a result, i managed to put away $100 a month into my travel funds and this adds up to a significant amount of $1,200 a year. A sum that is sufficient for me to pay for the return air ticket to Hong Kong which including hotel and shopping expenses incurred during the trip. I am also getting $400 worth of commission rebates from DIYInsurance which i can either re-invest or spend it on my next trip. (I have re-invested it)

In conclusion

By taking charge of my own finances, i am now enjoying a higher returns of 2.25% (excluding the 1% bonus to insure or invest) from the money sitting in the bank as well as future incoming funds. I have also manage to cut down on unnecessary fee and charges slapped on expensive insurance products by switching to a more affordable term cover and investing in a low cost funds.

I have lost some money in the investment linked product but at the same time i have took home valuable knowledge and wisdom of managing my own finances, and as a result, created more wealth from it.

Well, perhaps a road trip to Australia next?

(Article contributed by Cheryl, a Marketing Executive working in Singapore.)