To clarify some questions and misconceptions surrounding the collapse of FTX.com, the Monetary Authority of Singapore (MAS) has recently issued a statement. The Bahamas-based crypto exchange company filed for bankruptcy in the US on Nov 11, 2022 and is said to owe about US$3.1 billion (S$4.26 billion) to its top fifty creditors. Its short reign started last 2019.

In the statement released by MAS last Nov 21, MAS highlighted three key points.

#1: IT IS NOT POSSIBLE TO PROTECT LOCAL USERS FROM FTX.COM

Since the company is not licensed under MAS and operates offshore, it is not possible to protect the local users who dealt with the bankruptcy of FTX.com. “MAS has consistently warned about the dangers of dealing with unregulated entities,” the central bank said.

#2: THERE WAS A CLEAR DIFFERENCE BETWEEN BINANCE.COM AND FTX.COM

To the central bank, there was a clear difference between fellow crypto exchange companies Binance.com and FTX.com. While both companies are not licensed in Singapore, Binance.com was actively soliciting users in Singapore while FTX was not.

“Binance.com in fact went to the extent of offering listings in Singapore dollars and accepted Singapore-specific payment modes such as PayNow and PayLah,” according to the statement released by MAS. Thus, it was placed on the Investor Alert List (IAL).

#3: IT IS IMPOSSIBLE TO LIST ALL CRYPTO EXCHANGES ON IAL

Hundreds of such exchanges and thousands of other entities offshore exist so, MAS says that it is not possible to create an exhaustive list of all offshore crypto exchanges in the world on the IAL. The purpose of the IAL is to “warn the public of entities that may be wrongly perceived as being MAS-regulated, especially those which solicit Singapore customers for financial business without the requisite MAS license.”

Image Credits: pixabay.com

Users looking to refer to all the MAS-regulated entities should refer to the Financial Institutions Directory. This directory keeps an exhaustive list of such entities. It is important to remember that crypto exchanges can and do fail.

“Even if a crypto exchange is licensed in Singapore, it would be currently only regulated to address money-laundering risks, not to protect investors,” says MAS.

Bankruptcy is a big word, and some people fear it. But if one were to be familiar with its foundations, maybe it wouldn’t be that terrifying.

According to Investopedia, bankruptcy is a legal proceeding in which a debtor and a creditor resolve debts through the court system. The debtor has its debt resolved while the creditor obtains repayment based on the debtor’s available assets.

For folks considering bankruptcy, here are the basics you should be aware of.

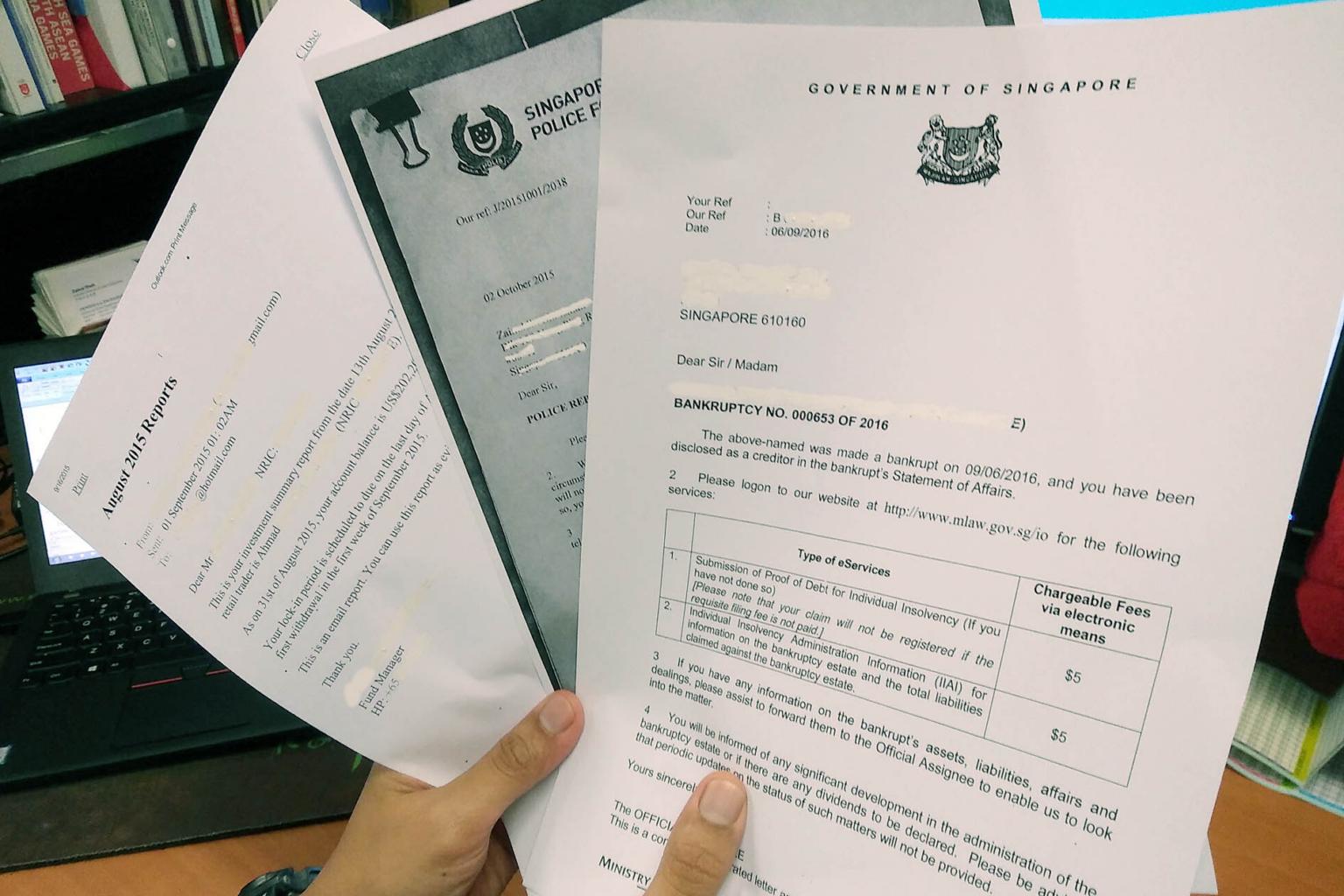

After declaring bankrupt

Once you are declared bankrupt, you gain exemption from your creditors’ legal actions intended to reclaim debt from you. A public servant called an Official Assignee (OA) would examine your financial capabilities and design a suitable repayment plan.

Think of it as your bankruptcy supervisor.

Your OA will ensure that you make monthly contributions on your road to being discharged. They will set up this monthly plan after evaluating your financial resources, income and credentials, household expenses, and the economy’s overall status.

Wave goodbye to your assets

Image Credits: EdgeProp

During the bankruptcy proceedings, your OA will sell any assets you possess to pay off your creditors. This can include items from artworks to furniture and even sentimental gifts.

Life insurance policies if it benefits the bankrupt’s immediate family members

Compensation awarded legally due to personal injuries or wrongful acts against the bankrupt

While it may be tempting to hide or dispose of your possessions quietly, lying to your OA or evading the procedure on purpose can lead to fines of up to S$10,000 and/or up to 3 years in prison.

Not worth it, ladies and gentlemen.

Ready for restrictions on daily activities

Bankrupt persons in Singapore are subject to various duties and responsibilities. Gambling, travelling, seeking credit, or managing businesses while involved in bankruptcy proceedings can lead to monetary fines or jail time.

These restrictions exist to prevent bankrupts from exploiting corporate structures, concealing income, hiding assets, or generally cheating the system. However, the OA can ease or accommodate these restrictions.

Their willingness to do this is based on your level of cooperation. If you are engaged in the bankruptcy process and consistently settling your debts on time, the OA is more likely to view you as reliable and ease those limitations.

Especially so in the business realm, full cooperation, including the provision of requested documents promptly, is the single best strategy for getting those restraints lifted as soon as possible.

If you feel that the OA is not treating you fairly or is imposing ridiculous restrictions, the ideal course of action is to seek the court’s review. Simply ignoring the limits is likely to end with criminal charges against you.

Look forward to the discharge

Image Credits: The Straits Times

Bankruptcy is not forever. Eventually, your debts will be paid, and you will be discharged from them. However, a discharge is dependent on the fulfilment of specific conditions and approval from either the OA or the High Court.

First-time bankrupts with debts of less than S$500,000 may be discharged after 3 to 7 years. For repeat offenders, it will take between five and nine years.

There is a well-known belief that a bankrupt is automatically released after three years, but this is not true. To speed up the process, cooperate fully with the OA and make sure you’re keeping up with your monthly repayment amount.

Bankrupts who have debts exceeding S$500,000 will need to apply to the High Court to seek an Order of Discharge. However, the courts will examine the interests of all involved parties before making a decision.

Noncompliance with the OA or any violation of behavioural restrictions will make the court reluctant to dismiss your bankruptcy.

Resume life after bankruptcy

Being discharged from bankruptcy is not necessarily a return to normal. At least not immediately. Depending on the circumstances of your bankruptcy, the courts may require you to entrust any new properties to the OA if debts remain after discharge.

Should the owed amount be repaid, bankruptcy can only be removed from your records after five years. If not, the bankruptcy status will remain in your public record permanently. Employers and creditors will have access to this information, so this should be a huge red flag for concern.

Final thoughts

Image Credits: AsiaOne

Bankruptcy is not a walk in the park, but it is not the end of the world too. The Bankruptcy Act is designed to be fair to both debtors and creditors and focuses on providing rehabilitative measures to the bankrupt.

For the severely indebted, bankruptcy can provide a mechanism to help recover financial health and gain a second chance at life. Be sure to cooperate fully with the courts, and the OA and the law will likely give you more space to breathe.

When you hear the word “bankruptcy”, you might have found yourself forming a mental image of a destitute and homeless person begging for money on the street while carrying a sign that says, “Will work for food”. While it might sound a bit too extreme for an outcome of bankruptcy, the stigma surrounding the term itself isn’t entirely unfounded as bankruptcy usually serves as a last resort measure that a person considers only when all other options for repaying the money owed from a creditor have already been exhausted. Thus, you would want to avoid heading straight into bankruptcy as much as possible by knowing some of the key signs that you should watch out for so that you can try your very best to remedy them before it’s too late.

What Are Some of the Key Signs That You May Be Heading for Bankruptcy Without You Even Knowing It?

While it’s completely normal to incur debt from a creditor as long as you can commit to timely repayment of the money that you borrowed from them, you might have taken up too much debt so that you’re unable to get through a single day without thinking of how you can pay your creditor back. As much as you’re putting off the idea of filing for bankruptcy, if your debt has grown to become increasingly unmanageable that you could barely settle it yourself, you would want to identify these key signs that you might be headed for bankruptcy without you even knowing it:

You’re making only minimum payments for your credit card.

Every credit card billing statement has a minimum amount due, but it doesn’t mean that you shouldn’t aim to settle your credit card’s entire outstanding balance on a monthly basis.

Unfortunately, some credit card holders pay only the minimum amount due every month as they feel that it’s more convenient for them since it usually costs less than their credit card’s total amount due.

When you’re settling only your credit card’s minimum amount due, a huge portion of it goes to interest with the remaining small amount serving as your actual payment to be deducted from the outstanding balance.

You’ve been taking out loans from your retirement account.

Often considered to be a rainy-day fund, the balance of your retirement account shouldn’t have a single deduction in it since you’ll be using it for when you’re required by the law to retire from your job due to old age.

However, you might be tempted to take a small loan out of your retirement account if the entire balance of your bank account isn’t enough to repay your debts.

While using a retirement account loan to pay back the money that you borrowed from your creditor might seem like a brilliant idea at first, you would have to deal with the need to deposit money back into your retirement account every month as well, which only adds to your existing debt problem.

You’ve been receiving calls from a third-party agency that your creditor had hired to collect your debt.

If you still haven’t paid back the money that you owe your creditor several months after you borrowed from them, they would entrust the collection of your outstanding debt to a third-party agency who might not take to your situation as kindly.

A debt collection agent would gently remind you at first over the phone to settle your debts, but if you still bail out on it, they might start making increasingly urgent and sternly worded calls to break you into paying back the money that you owe your creditor.

Worse comes to worst, your creditor might file a lawsuit against you that would require your employer to withhold a certain portion of your wages and send it as repayment of your debt.

If you find yourself unable to manage your finances properly you may have begun to feel that you can’t repay your debts on time. This situation only leaves you with more debt that you’re unable to keep up with it, and you might have started swallowing your pride and looking into filing for bankruptcy. However, it would greatly benefit you if you can read the above-listed signs to watch out for if you’re heading into bankruptcy without even knowing it so that you can address and resolve them immediately. To help you decide more clearly on what to do when faced with insurmountable debt, you should talk to a lawyer who can assist you in mitigating the ill effects brought about by those signs that might be telling you to file for bankruptcy and what you would need to do in case bankruptcy is the only solution left for you to wipe your slate full of debt clean.

Veronica Ferguson is equipped with more than 20 years of experience as a businesswoman. She is currently writing her next big project and hopes her pieces would impart vital knowledge to her readers. Veronica is a family woman, and is often with her family during her free time.

Disclaimer: The information presented below is meant to serve as a guide on some of the key signs of bankruptcy that you may not know about, and shouldn’t be interpreted as legal advice. If you want to find out more about how you can file for bankruptcy, you would have to contact a licensed bankruptcy attorney who can guide you throughout the entire bankruptcy filing process.

While experiencing bankruptcy is tragic and bouncing back is challenging, there are some strategies to get your monetary train on track.

1. COMMIT TO CHANGE

You are feeling isolated and helpless due to the recent loss of your assets, bank accounts, and primary source of income. Declaring bankruptcy can shake one’s confidence in many ways. However, you need to be reminded about the brighter things ahead. Is there any place to go to than up? The best thing that you can do now is to pick up the pieces and put them back together.

The first step is to make a strong commitment. Change your financial habits and be ready to perpetually follow through a plan.

2. ANALYZE THE CIRCUMSTANCE

You must analyze the overall financial circumstance that you are in, especially the events that led up to your downfall. Figure out the financial mistakes you made in the past and avoid repeating it in the future.

I have to admit that some setbacks are due to factors that are beyond your control (e.g., layoffs due to recession). While others are due to poor financial decisions. For instance, you became addicted to retail therapy and exhausted all your income on designer goods. You skipped out on emergency fund in favor of your fashion sprees. This is why you must come up with a plan to dig yourself out of the financial trap.

Image Credits: pixabay.com

3. FIX YOUR BUDGET

A new budget will help you rebuild your wealth by placing some constraints on your spending. Treat this as a map that will guide you to your financial goals. Now, let us start with the income. It is most likely that you are left with a single source of income that pays a minimum amount. Search for other part-time jobs or additional streams of income that can aid your journey. Face the uphill battle with a realistic budget.

Find ways to ensure that you are spending less than you are earning. I know it is not easy at first but, you have to endure the tides. Cut the unnecessary spending that you can spot in your previous budget. Rather than purchasing a smaller flat, ask your friends or family if you can crash their homes and pay a “rent” for the meantime. Lastly, sell your mint condition items to earn more money on the side.

4. PAY OUTSTANDING DEBTS

Contrary to popular belief, bankruptcy will not dissolve all your debts. You are not entirely safe yet! Although many of your unsecured debts were discharged, other forms of debts may still be on hold. This includes child support and student debt.

This is why you must gather and organize your financial documents. Determine all your obligations and list them down. Then, figure out various arrangements to pay off each one.

5. KEEP THE FAITH

The graceful bamboo stands firm in a beautiful sunny day. But, it is not always sunshine and rainbows. As strong winds gush through the forest, the graceful bamboo sways with the breeze. Be pliant like a bamboo. Embrace the strong winds of life much like this graceful creature does!

Image Credits: pixabay.com

No plan is entirely perfect and roadblocks are inevitable. Do your hardest to rebound from every setback and reverse the financial situation. The worst thing that you can do right now is to give up!

Are you searching for ways to improve your credit score for a better financial future?

You can see the light at the end of the tunnel when you first realise that so much of it depends on numbers. Your credit score is one of those important numbers. It is guaranteed to influence the cost of the big ticket items you have to prepare for such as taking out a mortgage, planning a wedding, qualifying for a car loan and building up for retirement. A good credit score is crucial for these financial successes.

Improving your credit score should be a priority. The higher your score, the better your chances of getting the credit you need. So do you know your credit score? And more importantly, do you know how to improve your credit score if it’s not measuring up?

Here are five tips to help you improve on your credit score.

Check your credit report and rectify any mistakes

Any incorrect information you find on your credit report could be affecting your credit score. Check your report thoroughly and get it fixed if you do see a mistake or factors that have pulled down your score. It is advisable to check at least once a year as the information in your credit report determines your credit score. Take steps to fix it and follow up to ensure it has been resolved. Otherwise, the error will remain on your report and could possibly hurt your credit score.

If you wish to dispute the completeness or accuracy of any item of information such as the account status, previous enquiries and overdue balances, do consult Credit Bureau Singapore (CBS) and CBS will post a notice in your credit file that the credit data is being disputed and is under investigation.

Pay your bills on time, all the time

A missed credit card bill payment will have the greatest and longest lasting impact. The more recent the missed payment occurred, the greater that impact will be, and the more missed payments you have, the longer it will take to recover. The prescription here is clear: Pay your bills on time, all the time.

How you charge purchases to your credit card and pay off your credit card debt every month will determine your credit standing and show how much of a credit risk you are. Paying your credit card balances in full every month helps you to maintain your credit rating and build up a good credit score. This will enable you to use credit to work harder for you, rather than becoming a slave to credit.

Where possible, always try to pay in full as rollover or outstanding balances will be charged at 24% p.a. Consider payment via GIRO to ensure payments are not late. The consistency of paying bills on time is critical to your credit score. It is simply month after month of plain-vanilla, on-time payments. This will greatly help improve your credit score if you are trying to offset the late credit card payments as these on-time payments will make positive behaviour in your favour moving forward.

Note: Default records stay on your credit report for 3 years upon full or negotiated settlement while bankruptcy data is retained for 5 years from the date of discharge from bankruptcy.

Avoid multiple new credit applications within a short period of time

There is no hard and fast rule that determines the number of new credit applications that will push you from looking like a responsible consumer to an unreliable one as every bank has a different set of requirements and criteria to satisfy.

Applying for new credit facilities within a short period of time can have an adverse effect on your credit score as it would put many enquiries against your credit report. Always approach credit use with moderation.

Note: Previous Enquiries are retained on your credit report 2 years from the date of enquiry.

Keep your credit active

One of the main purposes of having a good credit score is to ascertain that you are a responsible user of credit. It may seem contradictory, but it is not good enough to simply pay off your credit card bills and not utilise them again. There’s a solution, but one that should not be treated irresponsibly. Use your cards from time to time, manage within your credit limits and generate a sustained history of on-time repayments. Keep your credit active. In today’s world of credit repair, part of proving you’re a good credit consumer is actually using your credit.

Commit to keeping it simple

The bottom line when it comes to credit is this: When you do pay your bills on time, all the time, keep your balances low, avoid multiple new credit applications within a short period of time and keep your credit active, your credit score will work out fine. Many of us tend to overthink credit, but it is that simple. It is all about prioritising what’s important to you.

The absolute best thing you can do for your credit is to commit to doing the following in the long term:

Check your credit report annually

Pay your bills on time, all the time.

Avoid multiple new credit applications within a short period of time

Keep your credit active

Not everyone may have a sterling credit record but the good news is, it is entirely within your power and control to rebuild your credit health. You also have to be consistent. The above factors all matter, and credit is not something that grows by leaps and bounds, but if you treat it right, it will not fail you but push your score in the right direction.