According to Markit Ltd., Singapore’s 2016 dividend growth forecast is among the worst. On the other hand, the South Korea’s dividend growth forecast is among the best in the Asia-Pacific region. This is with the exclusion of countries such as Australia and Indonesia as they are foreseen to cut payouts.

For those of you who are less knowledgeable about the stock market, a dividend is the payout or the distribution of the company’s earnings to its stakeholders. These are issued as cash, shares of stock, or other properties.

Markit, a global provider of financial information services, based its dividends outlook on what is supposed to be reported in 2016. Thus, the year-on-year comparison is in accordance with the dividends reported in 2015 (FY14 final + FY15 interim) and in 2016 (FY15 final + FY16 interim).

Markit foresees Singapore to distribute S$15.865 billion in 2016 – only greater by 0.3% from last year’s S$15.824 billion. If specials are included, the distribution is predicted go down by 2.5% (S$16.2 billion) compared to 2015’s S$16.6 billion.

Continue to sleep well if you are a stakeholder at Singapore banks because as a sector, it remains to be the highest dividend payers.

Image Credits: Wikimedia Commons

In fact, a Markit analyst said that the three Singapore banks’ (i.e., DBS Group Holdings, OCBC Bank, and United Overseas Bank) contribution to the total dividends increased to 27.2% last year from about 25% since 2011. However, this number is estimated to go down slightly to 27.1% this 2016.

OCBC Bank and DBS Group Holdings are presumed to observe single-digit increases while United Overseas Bank is improbable to pay a special dividend in its final 2015 results. In the past few years, United Overseas Bank has paid special dividends of 5 cents in 2013-2014 and of 10 cents in 2012.

Image Credits: pixabay.com (License: CC0 Public Domain)

Once again, these numbers are solely based on the predictions of Markit and are not entirely carved in stone!

James Berry, e-Commerce Director from Collinson Latitude explains how for banks and credit card providers, it’s time to make rewards add up, or risk losing out.

Consumers are keener than ever to shop around for a good deal when it comes to their finances, you just need to look at the rise of personal finance sites like Money Digest to see that. Armed with smartphones and 4G, they compare everything from the cheapest travel insurance to the best credit card rate, and are not afraid to do their research in order to get the best return for their hard earned cash.

In a new report, ‘Taking Account: The consumer perspective on loyalty programmes in financial services’ it was highlighted that nearly two thirds (63%) of consumers globally are now swayed by rewards on offer when choosing a new bank and credit card. In Singapore, stronger sentiments are expressed with nearly three quarters (73%) indicating that rewards have an influence on their choices, exceeding that of the global average. This actually ranked rewards on offer above customer reviews and almost on a par with brand reputation in terms of their sway in consumers’ decision making process.

But, it seems the financial service (FS) providers are playing catch-up when it comes to customer satisfaction. Many remain lulled by the false sense of security created by years of stable loyalty, as only 1 in 10 Singapore consumers said their rewards programme offers an excellent service.

The fact is the rules of engagement are changing.

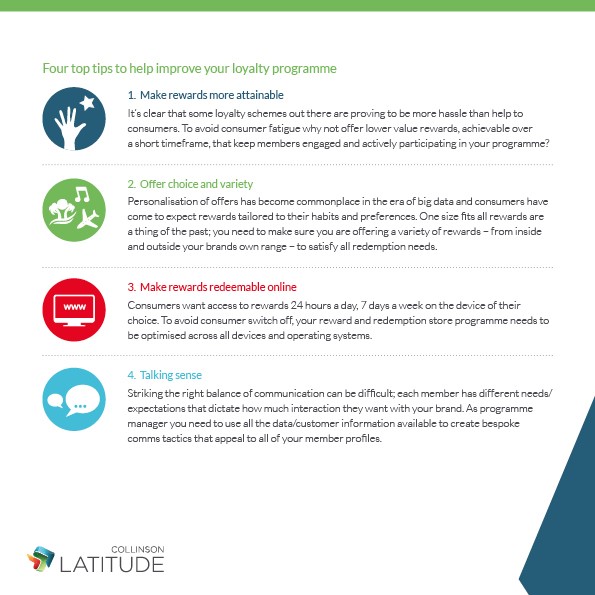

Making Rewards Add Up

So we know loyalty programmes have a significant impact on consumers purchasing decisions when choosing a new bank or credit card, and that a positive rewards experience can evoke loyalty – but if it was that easy wouldn’t everyone be doing it?

The simple answer is yes, but it’s not that simple. Availability of a programme is one thing, matching it with increasingly high customer expectations is quite another.

Consumers today expect rewards that are suited to them and their lifestyle. Over eight in ten of respondents globally said that their reward programme would be better if it offered more choice and allowed them to choose the categories of reward they wanted. The point is, customers have come to expect value, flexibility and choice when it comes to rewards. With more than one in two preferring to engage with their programme online, offering a single channel package will no longer suffice. Using customer data to pinpoint their preferred touch-points and fitting the redemption process around these will encourage conversion, beneficial to customer and financial providers alike.

Cashing In On Loyalty

Unfortunately many companies in the FS industry continue to look towards reward programmes as an ‘add on’ rather than as an integrated part of their business offering; this undoubtedly has a knock on effect for customer satisfaction.

What’s important for programme managers and marketing professionals in the sector to realise is that consumer expectations have changed; they expect to be rewarded for their custom 24 hours a day, 7 days a week, on the device of their choice. Banks and credit providers need to start investing in more personalised reward programmes that offer consumers greater choice and accessibility.

In an era where online banking, live chats, mobile banking and remote account management are considered a necessity rather than a value add for ‘connected customers’ – rewards and incentives are helping differentiate providers. In fact, around three quarters said they would like better access to rewards online and the ability to redeem their rewards more easily.

The Forecast for Loyalty in Financial Services

Over the past ten years and during the midst of a world-wide economic crisis, the financial services industry had a shake-up – one that has thrown up new ways of doing things and ultimately changing the way consumers interact with them. So far, many have managed to keep hold of their customer base, but how many of that base have already taken a loan or a credit card with another provider?

It’s hard to say, but what is clear is that with smartphones in their pockets and information at their fingertips, it’s easier than ever for your customers to look elsewhere. And when they do, a decent reward programme will be towards the top of their priority list.

If you’re unsure how to go about ensuring your reward programme meets these needs our tops tips below are a good place to start:

Believe it or not, the bank often lends its money to people who are stable enough that they would not need to borrow the money anymore. This is why some Singaporeans turn to alternative ways of acquiring money including Licensed Money Lenders. Now, before you borrow money from any of these options, you must know their differences first.

BANKS

Loaning money from the bank guarantees that there would be future repayment of the principal amount and its interest. A loan can either be specific or open-ended credit up to a certain ceiling amount.

Characteristics:

1. Larger Loans – Banks are ideal for larger loans such as renovating your home, starting a business, or buying a car.

2. Credit Assessment – A good credit score with a low debt to credit ratio is a must to qualify for a loan. And, if you want to pay a low interest rate, you need to be vigilant about your credit score.

LICENSED MONEY LENDERS

Licensed Money Lenders are businesses that are regulated by the Singapore’s Law. Unlike the loan sharks that lend with high interest rates, licensed money lenders’ fees are controlled by the parameters of the Law, which means you can expect to have a fair deal. Some of the known money lenders in Singapore are Max Credit, CashMax Credit and Quickloan Pte Ltd.

Characteristics:

1. Smaller Loans – Licensed money lenders are the ideal option for smaller loans such as paying utility bills, getting your laptop fixed, or repairing your car (even amounting to S$1,500).

2. Credit Assessment – Unlike the banks, licensed money lenders give more leeway in the credit score. This is because they lend a significantly smaller amount. So, if you have a bad credit and you cannot get a personal loan, licensed money lenders are there for you.

3. Transaction Speed – Licensed money lenders approve the borrower’s application within the day itself!

4. Higher Interest Rate – Since they carry more risk for granting loan to people with poor credit rating, they usually charge a higher interest rate and late fees

Image Credits: Taber Andrew Bain via Flickr

Although the license money lenders give more freedom in the credit score, they will reject your application if you have a large sum credit card debt or if you have an outstanding loan from another money lender.

According to Investopedia, Savings Account is an account managed by the bank which provides principal security and a moderate interest rate. Personally, I value this financial tool because it serves as an accessible shield to cover the immediate expenses. Before you open your own savings account, here are the 5 helpful and feasible things you should consider…

1. HOW MUCH TO SAVE

Having enough money in reservation, especially in an expensive country such as Singapore, is very important not just for you but for your family too. A savings account with an emergency fund can pay for the unforeseen expenses instead of using credit cards or applying for loans. You need to ask yourself this: “How much do you need to save?” Consider your needs and that of your family.

2. CHOOSE YOUR BANK WISELY

The first thing you should look out for aside from your eligibility to open the savings account, is the initial fee and the maintaining balance requirements. For example, UOB’s passbook savings account has an initial fee of as low as S$500 (for Singaporean/PR) and a maintaining balance of S$500. While, OCBC’s passbook savings account has an initial fee of S$1,000 (for Singaporean/PR/Foreigner) and a maintaining balance of S$1,000.

3. ATM AND BRANCHES AVAILABILITY

It is important that you can withdraw the cash from your savings account at your convenience once the need arises. Be sure to examine the bank’s ATM locations. Are there ATMs near your home, workplace, or frequented shopping malls? Also, if you are traveling a lot then, a bank with branches around the world is a better option.

4. SCOPE OF FACILITIES

In today’s world, most banks allow Internet banking and even Mobile App banking to check your savings account balance and to make various transactions. Consider this. Also, know whether your savings account comes with a passbook, a debit card (e.g., with VISA, NETS, or MasterCard), or an ATM card. This will help your options to narrow even more.

5. ESTABLISHING THE SAVINGS

To establish your savings, it is better to have a fixed amount to put inside every month. First, you must set a long-term goal about the money you can accumulate. Second, you must set a time frame that allows you to complete your goal.

Image Credits: Ken Teegardin via Flickr

Do not forget that different banks have varied interests rates that may affect your savings.

Like a kid in a candy store, consumers have various loans to choose from. From education loan to home loan, we shall look at personal loan through a microscope.

Personal loans are used for family emergencies, home furnishings, or consolidating other debts. These loans are often short-term.

1. APPLICATION PROCESS

You will be asked to complete a loan application that may include: your name, NRIC, date of birth, address, current and previous employers, length of employment, occupation, sources of income, total monthly income, and information about existing credit accounts.

Image Credits: Chris Potter via Flickr, (stockmonkeys.com)

Your credit card report includes your bill-paying history, amount and type of accounts you have, late payments, collection actions, outstanding debt, and so on. This along with your application shall help the bank decide if you are trustworthy and credible enough to pay the personal loan.

2. THE MORE PARTICULAR IT IS, THE CHEAPER IT GETS

When getting loans, be as specific as possible. The reason behind it is that loans that are particular often have lower interest rates. So, do not take up a personal loan to pay for a school debt when you can just apply for an education loan.

Personal loans tend to charge about 6% to 8% interest while Renovation Loan, Education Loans and etc. tend to have interest rates that are as low as 2%. Know what is best for your situation.

3. REVIEW YOUR OPTIONS

You may be tempted to immediately contact your current bank but that may bite you in the back. Personal loans and its interest change outrageously across time.

When there is less people borrowing from the banks (e.g., bad economy), they tend to lower the interest rates or give more lenient payment terms. So, look for a bank that is willing to give you the best offer and the maximum rewards.

4. WHAT HAPPENS WHEN YOU PAY LATE

Before venturing in, you must find out the clause of the payment penalties first. Like credit cards, it is not impossible to get an “interest adjustment” for a late payment.

Frets not…banks understand that certain circumstances such as unemployment or chronic illness can make it difficult to meet the bills. If this happens, contact your creditor, explain your situation and work out a repayment schedule together.