If you are planning to buy your first property, you will be made to get accustomed to a term call “TDSR” or Total Debt Servicing Ratio (besides SIBOR, LTV and the likes) introduced on 28 June 2013. Not surprisingly, 1 in 3 home buyers are not familiar with how the TDSR works.

TDSR is one of the 8 rounds of property cooling measures enforced the the Monetary Authority of Singapore (MAS) since the financial meltdown of sub-prime crisis in 2008.

It has been more than a year since it was implemented and has since impacted the property market in Singapore, dampening demands and preventing housing price to go out of control.

What is TDSR?

To ensure financial prudence in borrowers, a framework is set to ensure that a borrower cannot has a outstanding debt repayments more than 60% of his gross income. This not only prevent home buyers of excessive gearing, it also ensure that financial institutions (FIs) are able to manage their credit risk appropriately.

Outstanding debt repayments encompasses ALL your financial liabilities which includes and are not limited to: student loan, credit card debt, car loan, personal loan, etc.

When your overall debts cannot exceed 60% of your gross income, it also means that if you are earning a gross income of $3,000 a month, your total debts cannot exceed $1,800 (60% of $3,000). That is to say if your existing outstanding debts amount to $1,000, your mortgage repayment should not exceed $800 – calculated with the higher of actual interest rate or 3.5% (for residential properties) or 4.5% (for non-residential properties). On top of that, there is a Mortgage Servicing Ratio (MSR) of 30% that stipulates that the amount that goes to service your mortgage should not exceed 30% of your income. In this case, your maximum allowable repayment is $900 (30% of $3,000).

* If you are a variable income earners (e.g commissions, bonus), there is a 30% haircut which means only 70% of the income is used in the calculation of TDSR.

Why is there a need for TDSR?

With low interest rate and growing investment appetite, coupled with excess capital liquidity – it could be an eerie reminiscent of the housing bubble in 2006 which eventually goes burst and causes mayhem. Fortunately, Singapore has various cooling measures which include a limit on the maximum loan tenure, loan-to-value limits and imposing stamp duties such as the Additional Buyer Stamp Duty (ABSD) and Sller Stamp Duty (SSD) and has managed to curb inflating property prices. There is also a stricter liquidity rule which requires bank to hold quality liquid assets such as cash and government bonds to withstand an intense 30-days shock witnessed in the 2008 crisis.

What happens after several rounds of cooling measures?

As one would have expected, property prices has been heading south and dampening demands has led to many unsold units. The URA’s Private Residential Property Price Index has fallen for the fifth consecutive quarters in the latest URA’s flash estimate published in 2 January 2015. For the entire year of 2014, prices has fallen by 4%. There are anecdotal evidence that if prices fall by 10%, Singaporeans have the liquidity and means to snap up the units!

Housing loans has just increased by 6 per cent in September 2014 from a year ago, a stark contrast of the peak of 23 per cent in August 2010.

The property market is still lackluster and Minister Khaw Boon Wan seems adamant to keep the property cooling measures, home buyers may find themselves landing a good deal with 50,000 new units to be completed over the next 2 years.

When you are caught in a beauty dilemma, you need a quick solution! In order for fast action to happen, health care products that are already available can be used.

Here are 5 Affordable Beauty Hacks that can make your life easier…

1. FOR YOUR SHINY FACE

To deal with your shiny face, you may use hand sanitizer or Sticky Notes (e.g. Post-it). Hand sanitizer has “dimethicone” that smoothens the skin like a primer and provides a protective coat locking in moisture. You may use this along the hairline, forehead, T-zone or cleavage.

Post-it or sticky notes remove the excessive oil on your face without ruining your make up. Just peel off a Post-it sticky part then dab it along your T-zone.

2. MULTI-PURPOSE PRODUCTS

Many of the health care products have multiple uses so stretch its capabilities to save more money. Here is a list of 4 multi-purpose products:

a. Toothpaste can double as pimple remover

b. Baby oil can double as a make-up remover

c. Nail polish cannot only personalize your jeans but it can also stop a run in your stockings.

d. Greek yogurt to reduce pimple inflammation and redness

3. FOR YOUR HAIR IRON BURNS

If you accidentally burn yourself with your hair iron or curling stick, use raw honey to alleviate the pain and provide antibacterial protection. Honey also keeps your skin hydrated and smooth.

Image Credits: Maegan Tintari via Flickr

4. FOR YOUR DRY FEET

Debra Jaliman, a dermatologist and author of “Skin Rules”, suggests adding two tablespoons of brown sugar to 1/2 cup of coconut oil to exfoliate dry feet. She says that it helps to get rid of the unwanted dead skin.

5. FOR YOUR UNRULY HAIR

Your hair may either be dry or dull. When this happens, gather the ingredients you have in your kitchen and try these hair masks.

a. Hydrating Mask

Heat up 4 tablespoons of olive oil for 20 seconds then mix it with 2 tablespoons of honey. Apply it in your hair and put a shower cap on for 20 minutes. Then, rinse it.

b. Mask for Shiny Hair

Mash one piece of avocado until the texture is smooth. Then, add 1/2 cup of coconut milk and 3 tablespoons of olive oil. Heat the mixture up for 20 seconds. Apply it in your hair and put a shower cap on for 30 minutes. Then, rinse it.

In Singapore, where costs are ever running high, you may find that your current wage is direly insufficient to help you save up for that big-ticket new car or house that you have been hankering after. As such, it is unsurprising that many Singaporeans are seeking to take up side gigs outside of their day job, where they are able to earn a quick buck or two in their leisure time.

That being said, perhaps you cannot expect to earn thousands from such additional sources of income – after all, you are hardly committing to them full time. However, the benefit of such side gigs is that they do not interfere with your usual day job, and instead allows you to capitalise on your free time as well as your unique hobbies, to reap some additional side income from which you can better achieve your newest 2015 financial resolutions!

If you are an avid Internet-surfer who is out to find ways to take up a side gig of your own, here are 6 easy ways for you to earn a side income online. These 6 methods of earning additional income online are so easy that almost anyone will be capable of taking them up – no matter if you are 14, or 40! All you need is some free time to spare, a computer, and the ability to read and write English, and you are good to go!

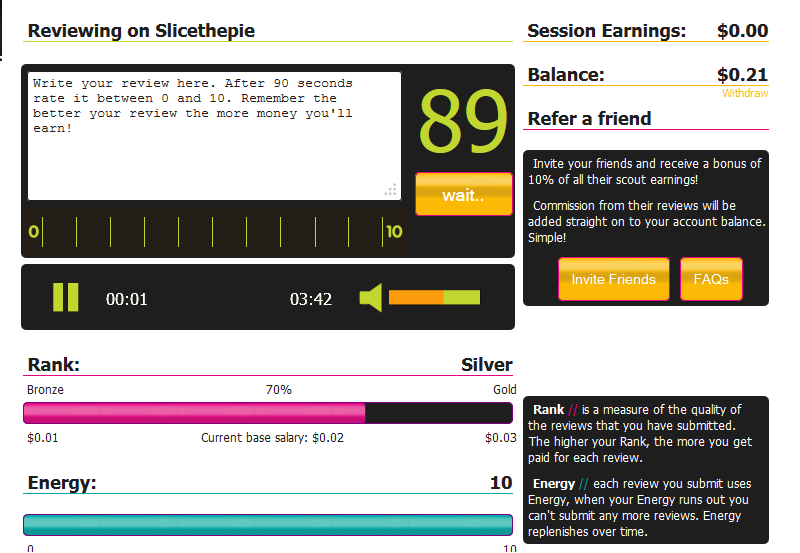

Are you a music enthusiast? If so, you might want to consider leveraging on your passion to write some music reviews on Slicethepie in your spare time.

On Slicethepie, you are paid for every music review that you write. Slicethepie is an online music community, where new bands upload their newest singles or demos, and reviewers can provide these bands with constructive criticism based on the soundtrack’s beats, melodies, vocals or production.

Although Slicethepie may not pay out a significant amount (reviewers start off with a base rate of 2 cents per song – a little paltry, but detailed reviews tend to get awarded more), it is a good way for music lovers to spend their time constructively to help out fellow musicians and earn some spare cash in the process. Plus, you get to listen in on exclusive tracks that have yet been released into the mainstream – what’s not to love?

If you find that your household is becoming rather cluttered with things that you no longer need, or items that have not quite come into use despite having been purchased five years ago – well, it is certainly time to let go of these preloved goods to better owners who will give them their due use instead of hoarding them in over-packed storerooms. And how should you go about finding these very ‘new owners’? The answer is simple – Carousell.

Carousell is becoming quite the household hit in Singapore, despite its recent inception in 2012. In fact, it is so popular that it seems to have garnered a permanent stay-hold on the App Store’s Top Charts. Through Carousell, buyers and sellers are brought together in an online marketplace.

If you have the time to spare, why not lay out all your unwanted items, snap a few pictures of them, and upload them onto Carousell, where potential buyers are abound? Surely, with the sheer extent of its reach – given that almost everyone has a Carousell account these days, it would be easy for you to find buyers who are willing to take over ownership of your preloved goods.

Certainly, clearing off your unwanted belongings through Carousell will allow you to earn some quick cash, and clear out your rooms for the new year!

Are you an Instagram addict? Or perhaps you might think of yourself as an up-and-coming blogger? Do you have relentless witty quips to share on Twitter? Or do you have a remarkable presence on Youtube?

Well, if you have a deep love for social media, and for sharing your adventures and exploits with the rest of the world, consider making use of your social media accounts to earn a quick buck. Companies are constantly looking for new faces and personalities to promote their products, and publicise their brand name. If you find that you have a sizeable number of followers on these social media platforms, you may be able to approach companies and successfully gain sponsors and paid advertisements, with which you can easily earn up to a hundred bucks or more per assignment.

Singapore has certainly made a fine art of social media influencing – just look at our top bloggers who are able to land even car sponsorship deals effortlessly! Anything and everything can be promoted on social media these days; why not hop on the bandwagon while it’s hot?

Another way of spinning some quick cash would be to fill out surveys online in your spare time. Corporations are constantly looking out for consumer feedback, and searching for new ways to identify the newest consumer trends. As such, giving your opinion in the form of paid online surveys can be deeply valuable to such firms, and you will receive due payment in the form of cash or shopping vouchers – a worthy transaction indeed!

Some of such paid online survey sites would include Opinisurveys, Toluna, and Mysurvey. But these are certainly not the only available survey sites. There are numerous online survey sites out there on the net, and all you need is to draw up a quick Google search, and you’ll be well on your way!

That being said, several paid online survey ads found on the Internet may turn out to be scams, so it is duly necessary to be discerning of any survey sites that promise rewards that seem too good to be true. Also, check up on the credibility of any new online surveying sites on the Internet.

If you’ve done your sufficient homework, then certainly carrying out online surveys is a remarkably easy and lucrative way of earning some extra moolah in your free time.

Do you have a flair for the written word? Do you have an undying passion for writing? Do you dream of getting published? If so, consider writing and publishing your own e-book! Given the rise in popularity of the e-book reader, e-books are gaining an ever larger audience, and surely you will be able to find a suitable audience for your very own book.

To publish an e-book, you can consider self-publication, or publication by legitimate publishing firms.

If you opt to self-publish, do bear in mind that you will have to cover all the costs of publication, and you might even potentially make a loss if your e-book fails to sell well. However, a major perk is that each sale of your e-book goes fully to you, and you have total ownership of your e-book.

On the other hand, if you seek to be published, it may prove an extended period of rejection until your manuscript lands into the hands of the right publisher who sees the potential in your work. However, it will eventually prove fruitful when your book is published, as such publishing firms often carry a more reputable brand name in the market which will help you to attain more sales for your book, and you will then be able to reap royalties from the sale of your e-book.

While the competition may be tough in the e-book industry, if you happen to land a hit, this may prove to be your fortune maker indeed!

In an age of industrialisation, where clothing and accessories are mostly mass produced or manufactured in factories, there has certainly been a surge in demand for hand crafted items in recent years. Goods that are produced in mass are often perceived to be common and mundane, and it is little wonder that several would rather shell out more money for unique hand crafted products. If you have a ‘crafty’ side (forgive the pun), why not put your skills to good use and create some handmade baubles for sale?

Etsy is an international online marketplace which curates an eclectic mix of independent stores which specialise in the crafting of handmade items, as well as the sourcing of vintage. As such, if you would like to peddle your home made wares online, Etsy is certainly the perfect place to host your online store as shoppers on Etsy are out to specifically find exclusive and uncommon handmade crafts and you will certainly be able to land a customer or two!

Not to mention, given that Etsy is popular internationally, you will be able to reach a wider range of customers than simply homely Singapore.

However, it is worthy to note that Etsy charges a fee of $0.20 USD for each listing. If you are unwilling to pay such fees, perhaps you can turn to Carousell or Instagram – both of which are entirely free platforms, to promote and sell your goods instead.

Some items are cheaper at certain times. Hence, with planning and knowledge, you will be able to save more money when purchasing throughout the year.

Here are the 11 cheapest things to buy from January to March 2015:

IN JANUARY

1. HOLIDAY ITEMS

Holiday items such as surplus or unused gift cards, Christmas decorations, and wrapping papers are now selling with discount in stores and in the Internet (e.g., eBay or Carousell). Buy now, as their condition and use will remain ’till next year.

2. LINENS AND BEDDINGS

Retailers offer huge discounts on sheets, towels, and blankets in January. But, keep an eye on it all year round, since retailers will put last season’s stuff on sale when new products come out.

3. VIDEO GAMES

Numerous video games go on sale after the holidays are over. Check out Steam and other gaming retailers for discounted prices.

4. COMPUTERS

Image Credits: Stefan Ledwina via Flickr

Like video games, companies offer discounts on older computer models to prepare for the upcoming release of new components and systems.

IN FEBRUARY

1. MOBILE PHONES

Some stores offer hand phone sales or even a buy-one-take-one scheme during Valentine’s Day. It may seem strange but it’s true.

2. WASHER, DRYER AND AIR CONDITIONER

During cold weather months, many appliance stores offer air conditioners at cheap prices. Also, old models of washer and dryers are being sold with good deals.

IN MARCH

1. WEDDINGS

Image Credits: Katsu Nojiri via Flickr

Tying the knot in this month means taking full advantage of the discounted prices on reception venues, catering, and photography. You must always be cautious of the venue’s weather.

2. CHOCOLATES

The surpluses from last month’s chocolates are sold for lower prices.

Image Credits: John Loo via Flickr

3. LUGGAGE

Retailers offer discount on luggage before vacation seasons of spring and summer arrives.

4. GOLF CLUBS

New models are coming out for the summer, so your local golf shops are pushing the old ones out. What’s more? Last year’s gold club models are much cheaper.

4. DIGITAL CAMERAS

Consumer reports and marketing analysis prefers grabbing digital camera in March and April, as sales are the best.

Mutual funds are investments that gather the investors’ money into a pool to make multiple types of investments, known as the portfolio.

Professional money or investment managers, who invest the fund’s capital and attempt to produce capital gains for its investors, operate the mutual funds.

The investment manager’s compensation relies on how well the fund performs. In this way, you can be assured that they will work hard to make sure the fund grows well.

Image Credits: Steve Jurvetson via Flickr

As a mutual fund investor, you become a “shareholder” of the mutual fund company. When there are profits you will earn dividends. When there are losses, your shares will decrease in value.

Mutual funds are diversified or are made up of different investments to lower the risk of loss.

Advantages of Mutual Funds

1. Mutual Funds give small investors the access to professionally manage, diversified portfolios of equities, bonds and so on. This is difficult and nearly impossible to create with a small about of money.

2. Each shareholder participates proportionally in the gain or loss of the funds.

3. The experts handle your money professionally…so even if you have little knowledge on stocks, you may learn as time goes.

Three Categories of Mutual Funds

1. EQUITY FUNDS. Equity funds are made up of common stock investments alone. Although this can be riskier, this can earn more money than other types of funds.

2. FIXED-INCOME FUNDS. Fixed-income funds are made up of government and corporate securities. Since the government and corporate securities provide fixed return, the risk of the investments are low.

3. BALANCED FUNDS. Balanced funds combine both stocks and bonds in the investment. It offers a moderate to low risk. So before investing to mutual funds, you will have decide how much risk you are willing to take.