You do not need a PhD to know that unplugging your cables and electronics when not in use can help you save energy and reduce your bills. Even if you turn the switches off, appliances will continue to use energy if they are plugged in.

Image Credits: Chris Potter via Flickr

2. KEEP IT COOL

Cold running water uses lower amount of energy than heated ones. So, use cold water when washing your clothes and dishes or when doing other tasks.

3. CHOOSE WISELY

If you are buying a new appliance, make sure that it is an energy efficient model. Smaller appliances not only help you save more on space but on bills also. Opt for a relatively small microwave than an oven and smaller lamps than the overhead lights.

4. REFRAIN FROM REPEATEDLY OPENING THE FRIDGE’S DOOR

Ensure that you know what you must get before opening the refrigerator’s door/s. Repeatedly opening and closing the door/s will only cause cold air to escape and for the appliance to work more than it should.

5. PUT DOWN THE BLINDS

During summer and hot days, put down the blinds to prevent extra heat from coming in and prevent your air conditioner from running more on energy. Do the opposite during the cold weather to keep your home naturally warm.

6. PAINT THE ROOF WHITE

In Color Psychology, white symbolizes new beginnings while in Business, it symbolizes efficiency. By merely painting your roof white, findings suggest that it can cause a 40% drop on the energy consumption. It also cools down the whole house.

7. COVER THE POTS

Cover your pots when boiling because if you leave it open, the boiling period will only be longer and therefore requiring more energy.

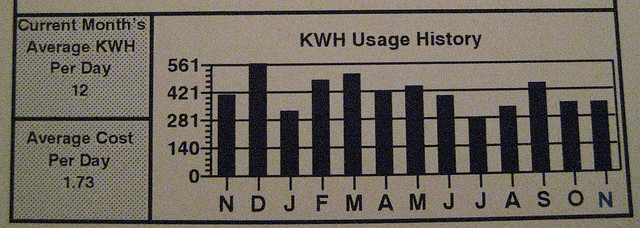

8. DOUBLE CHECK YOUR BILLS

Image Credits: Phillip Stewart via Flickr

Double-check your billing amount to ensure that you are paying accurately. Do this by checking the reported bill usage and comparing it to your meter.

When you are thinking twice on purchasing an item, ask yourself if you are willing to try it on the dressing room at that very moment. If you are not really excited to wear it then, do not bother to buy it.

2. AVOID “GIVING UP”, USE “SAVORING” INSTEAD

You will only feel deprived if your perspective is to give up something in order to save more. So, change your perspective and start “savoring” the moments that you indulge on lavish things. The goal is to change your frequency of indulgence and not to hinder you from enjoying life’s goodness.

3. WHEN YOU ARE NOT EARNING, YOU ARE SPENDING

Keep in mind that when you are not earning, you are just losing the money you earned. If there are opportunities to work more and your body feels okay then, take on the challenge. Sometimes, the feeling of losing money is more painful than missing it.

4. MAKE TIME A CURRENCY

To get a clearer perspective, break down the monetary value of things by the hour. For example, if you make S$10 an hour and a bowl of bean curd is S$2 then that is 12 minutes of your work and life. This technique will help a lot to cut down your impulse purchases.

5. BE MOTIVATED WITH A SLOGAN

If you are struggling to be frugal, make a tangible slogan or a poster that you can hang on to. For example, you can use this slogan to help you think critically when purchasing: “Use it up, Wear it out, Make it happen, or Do without it”.

Some online businesses and websites are prevalent of scams or are filled with annoying ads that give a bad impression. But, do not let that stop you. The Internet is full of realistic opportunities to make a couple of quick cash. All you have to do is be creative and patient in finding credible ones. Here are 6 ideas you can start with…

Originally from Australia, 99 Designs became one of the world’s largest online graphic design marketplaces. They have been connecting designers to customers who are in need of quality yet affordable designs. If you have always been good and passionate at Photoshop or any graphic design tools then 99 Designs is perfect for your skills. Simply enter t-shirt, logo, website, and print design contests to win and earn money.

Explore through your pile of books, clothes, and other items. Look for anything of value and good condition that you do not want or need anymore. Then, sell it on eBay or Carousell. eBay is a website that serves as a marketplace for people worldwide while Carousell is pretty much a Smartphone version of eBay. You can also sell your bargain items to your friends and family by posting an ad on Facebook.

3. CONTENT-BASED SITES

Content websites are always in the lookout for quality and sensible content. Know your expertise then get paid for each article at eHow or Constant-Content.

Amazon Mechanical Turk is a market place for workers, businesses, and developers. It gives you an opportunity to work from home and to hold your own working hours. Just find and complete simple tasks such as testing sites or answering surveys, to make money.

Crowd source your Micro Jobs to more than 600,000 Workers worldwide through Microworkers. Make money by completing small tasks online such as signing up for websites, searching articles, or linking url to websites.

Image Credits: Tax Credits via Flickr

These are such easy ways to make few bucks online! Try ’em now.

It is fair to say that travelling is one of the most soul-satisfying experiences that one can encounter. Unfortunately, it doesn’t matter if you’re in your twenties or forties, travelling can burn quite a hole in the bank account.

Where money spent transcribes to priceless experiences, it may be worth the wads of cash – but most of us don’t have that luxury.

Despite the tight budget some of us have to work with, there are 193 countries available to choose from – of which, even on a tight budget, definitely ample to travel a lifetime! But since time is of the essence, some might prefer not to travel too far – thus Asia would suffice.

Majority of these countries offer a variety of well-priced accommodations that aren’t too shabby, leaving you with enough spare cash to explore your surroundings. From the adventurous spirit to those who prefer to unwind, there’s unquestionably a place for you.

Here’s a list of five unexpectedly inexpensive places to travel in Asia.

1. Koh Lipe, Thailand

(Image credit: shin–k, via Flickr)

If you enjoy the sun, sand and sea – this is your ultimate paradise. Gaining popularity in recent years, it is the perfect getaway for couples, friends and even families. Known as the Maldives of Thailand, it is a small island in the Southern part of the Thai Andaman Sea. Crystal clear water, white sandy beaches and an abundant of marine life, it is part of a nature reserve and is also known as Thailand’s second National Park.

Activities such as snorkelling, diving and hiking are all reasonably priced, but if you want to spend less (or none at all), sunbathing at any of the three beaches will definitely keep the wallet fat and happy.

Generally priced a little higher than the mainland, it’s still thoroughly affordable.

2. Bali, Indonesia

Bali Tanah Lot (Image credit: Fabio Gismondi, via Flickr)

For travellers of all walks of life, Bali has something install for everyone – from the tranquil quiet getaway to party animals ready to get hammered, this is a must go destination if you’re ever in South East Asia.

Savour their local food and ride a bike like the locals do there. Not only do you save quite a bit, it’ll be a more enjoyable than renting a car. If you’re staying in Seminyak or Kuta, majority of the things are within walking distance – beaches, eateries, shops and massage parlours. Various packages and tours are also available for those who prefer to explore temples, rice terraces and the famous monkey caves or even white water rafting and ATV rides through the lush forestry.

Without the tours, $50 a day is more than enough to spend.

Filled with interesting historical sites and national parks, Sri Lanka, is one destination that aren’t on majority of travellers “top lists”. One of the cheapest places to travel to on this list, there are plethora of things to do in Sri Lanka such as visiting wild safaris, whale watching, rock climbing and even hot air ballooning.

Try a popular local beverage that you can buy off the streets,Thambili. Made from fresh coconut water and is very refreshing, and it’s also a cheaper option compared to bottled water.

Their staples are often made with rice and curry and can be very spicy. Sri Lankan and South Indian cuisine eats for under a dollar, but there are also more touristy places where you might pay upwards of ten U.S. dollars.

Lastly it’s best to go around in a tri-shaw, or three-wheeler, which is comparable to a tuk tuk in most nearby countries. While they’re fun to ride in, there are some safety concerns.

Overall, $15 a day would suffice.

4. Yemen

Haraz Mountains, Yemen (Image credit: Rod Waddington, via Flickr)

Known as Arabia’s undiscovered gem, Yemen is where you can find the world’s oldest skyscrapers, spectacular mountaintop villages, pristine coral reefs, and stunningly gorgeous trees unseen anywhere else on earth. Dubbed as one of the dangerous holiday destinations, that’s the appeal to most who travel there.

Stepping out of your comfort zone, Yemen has a long list of eco-activities, camel and horse riding as well as paragliding tours which will definitely make it a unique holiday. Visit their local fish markets and try the popular Arabic coffee.

Ladies, note that you don’t have to dress definitely the Yemeni way but dress modestly in the public places – bare shoulders and miniskirts are not appreciated. The same goes for kissing in public.

* Singapore Airlines is having a two-to-fly fares sale until 31 Mar 15. Fares starts from SGD 358 for Bali and SGD558 to Colombo when you book with your MasterCard®. More info here: Singapore Airline's Sale. If you want to get to Koh Lipe, the easiest way would be to travel to Langkawi, grab a 10 minute taxi ride to Telaga Habour and then take the 60 minute ferry across to Koh Lipe. For Yemen, travelers are advised to defer travelling plans due to civil unrest until further notice.

For hotels booking, use our hotels search engine here: http://hotels.moneydigest.sg where we search thousands of travel sites to get you a best-price guaranteed hotel

Long before you give birth to your child, the desire to buy adorable child’s clothes kicks in. But, quickly growing children, changing of fashion trends, and huge deals may put a hole on your pocket. Giving your child fashionable clothes does not have to be expensive. Here are 5 Ways to Save Huge Bucks On Your Kid’s Clothing…

1. OUT WITH THE NEW

Since your toddler grows increasingly in the first few years then buying new clothes every year will surely break the bank. Try buying stylish clothes that are very cheap in thrift stores, garage sales, or online (e.g., Carousell or Gumtree).

There are a couple of neat thrift stores in Singapore namely: Praisehaven Thrift Store, New2U Thrift Shop, Oakham Market, and O-Mighty. Most of these thrift stores are donating its proceeds to charity. Visit Yelp.com.sg to read the reviews of these stores. The best part, of course, is that you’re contributing to a great cause while shopping.

2. HAND-ME-DOWNS

Hand-me-downs are totally free! Ask your family and friends (whose kids are older and bigger than yours) if you can have their children’s outgrown clothes. You will not only help your family or friends to de-clutter their space but you will also save more.

3. USE CLOTHES FOR MULTIPLE PURPOSES

Get your child leggings that she could wear during the cold weather then keep wearing them as capris the next summer. Same thing goes for dresses, you can use them as a dress or a shirt once its outgrown.

4. BORROW OR SEW YOUR OWN

For occasions that require special outfits such as Halloween, weddings or other formal parties that you only wear once a year, you can just borrow costumes to save loads of space and money. If you are good in sewing, use your creativity to sew your own “princess or prince” costume for Halloween.

5. KEEP IT SIMPLE

Avoid buying a matching set because it is more costly and it limits your options. Instead, buy solid colored pants and simple patterned skirts that you can mix and match with funky shirts. You will save more buy these items during clearance sales.