Singapore is a haven for not only the food or fashion lovers but also for the digital savvy. That being said, most of the tourists that come to the Lion City are in search of the cheapest and the best electronics available. Fortunately, most if not all, provide you with the documents to claim the 7% GST from the Changi Airport. All you have to do is ask for it politely!

If you are set to buy quality yet reasonably priced Camera or Camera accessories, here are the Perfect Places To Buy Cheap Camera And Accessories In Singapore…

1. FUNAN DIGITALLIFE MALL

Topping the list is the famous Funan DigitalLife Mall. Funan DigitalLife Mall houses a variety of electronic stores with products at inexpensive yet competitive prices. These stores offer Cameras, DSLRs, Camera lenses, and more. One store that stocks ThinkTank Camera bags is the TK Foto at #02-14 and #02-38/41.ThinkTank bags are low profile and high-capacity bags suited for mirror-less Camera gear.

Rest assured that you would not be a victim of scam at the Funan DigitalLife Mall because its stores follow Singapore’s trading standards.

2. CATHAY PHOTO

One of Singapore’s trusted Camera stores is the Cathay Photo. Established in 1959, Cathay Photo offers an impressive range of Still-Cameras, Video Cameras, and professional studio equipments among others. They strive to give the best photographic equipments by importing from international brands and by widening their range of products.

The DLSR Cameras with HD video capabilities include brands such as Rotolight, Zacuto, Kessler Crane, and Steadicam. Accessories that they sell include lenses & filters, light modifiers, Camera straps, and Camera bags. They have two outlets with the Peninsular Plaza being a few steps away from Funan DigitalLife Mall. See the full locations here.

3. CEE SHOW AND IT SHOW

IT Show 2015 may have pass last March but shopping for attractive deals on electronics does not stop there! This May 29-31, CEE (Consumer Electronics Exhibition) Show will give you great deals on electronics, all in one place – Suntec Singapore.

For 3 days, you can get huge savings on your electronic lifestyle needs ranging from Digital Cameras to the latest touchscreen and LED displays. Also, you can trade-in your used or faulty electronics (e.g., laptops, tablets, and smartphones) to get up to S$1,200 worth of vouchers. Interested to trade-in? Get a quote by filling their form here: http://pcdreams.com.sg/CEE/ The best thing about CEE Show 2015 is not only can you get up to 90% off but admission is also Free!

They say that love is unconditional, selfless, and priceless. But the truth is, you have to spend money for roses, dinner, or even diamonds during special occasions such as birthdays or Valentine’s Day. And these gifts do not come cheap! The influence of money on the relationship does not stop there. It is significantly present in marriage. In 2012, a study found that the more regular couples argued over money, the more likely they were to get divorced.

There are different reasons why couples have dispute over money. One reason is the opposing views that deeply affect their values to the point that it is hard for them not to be self-righteous in the subject. Although, if both parties truly love each other and are willing to work things out then, they can set their differences aside. Here are 4 helpful ways to stop your couple woes over money…

1. DISCUSS YOUR VALUES ABOUT MONEY

To prevent another issue to boil, understand each other’s view by explicitly discussing your differences on financial issues. For example, if your partner is a saver then, he or she may view money as an important currency that shall not be wasted.

Learn put yourself in your partner’s situation (i.e., spender or saver) by recognizing his or her financial strengths. For example, if you are buying a washing machine. While a saver may lean towards a cheap and used machine, a spender will want a costly and new machine. Compromise by combining the saver’s ability to get a good deal with the spender’s ability to commit to a new purchase.

When faced in a situation where you are already frustrated and about to burst, take a step back from those feelings. Avoid blaming or shouting at each other. Instead, write down your feelings or values about money and how you want your money dynamics to change for the better. When your temper is gone, exchange letters to know where your partner is coming from. If you want to break the cycle of feud, you have to work together to a fresh start.

3. PRODUCTIVELY PLAN TOGETHER

Ensure that you will have a productive and open communication on your financial goals and new budget plan. Change can be difficult and you may need to remind each other of your dreams and budget from time to time.

4. ENCOURAGE INDEPENDENCE

Although you have a joint bank account, you may want to have separate bank accounts for your personal finances including buying gifts for your spouse or child. This degree of financial independence can help you deal with the changes better. Keep in mind that you shall still honor the new budgeting scheme and financial goals even if you have a personal account.

Image Credits: Robert Bejil via Flickr

In resolving your money woes with your partner, it is important to keep an open mind. Remember that it is not about winning or superiority, instead it is about understanding your partner’s perspective on money.

Are you in need of party supplies to use for the Birthday or the Mother’s Day coming up? What if you are hosting a themed party at home? You will need a variety of dramatic, novelty, or scary decorations of course. Whether you are hosting a safari-themed Birthday or a floral Mother’s Day celebration, here are the Best Shops For Wallet-Friendly Party Supplies In Singapore…

1. DAISO

If all the party goods in a shop cost S$2, you may never want to leave. Daiso offers party decorations, toys for give away, and glowing materials. You may buy a banner that says: “Happy Birthday” or “Happy Mother’s Day” to decorate your feast wall. Daiso has 7 outlets nationwide including one in Vivocity, IMM Building, and Plaza Singapura.

2. SPOTLIGHT

A popular crafts hub, Spotlight sells different kinds of inexpensive party decorations, table dressings, cake decorations, ribbons, toys, and candies. All the crafts materials that you will ever need could be found here.

Image Credits: spotlight.com.sg

Location: 68 Orchard Road, Plaza Singapura, Level 5

3. CAROUSELL

You would be surprise that Carousell, a mobile marketplace for bargain items, sells several party supplies too. My favorite item is the “Colourful Paper Straws For Party” priced at S$3/25 straws.

What I like about The Party Stuff is that they have party decorations for a wide selection of themes such as: Plaid Baby, Sports & Army Camouflage, Hawaii & Poker Night, Princess, and Superheroes. They offer party decorations, balloons, tableware, party favors, cake decorations, and costumes.

For S$5.95, you can buy the “Boom Wow Confetti Butterfly”: a handheld confetti cannon launching colorful Butterflies in the air. Also, take advantage of their Mother’s Day special 18″ balloons for S$7.90.

MTRADE is an online novelty wholesale store in Singapore. This store has countless of goods to offer including Personalized Party Items, Party Favors, Party Accessories, Stationery Gifts, Inflatable Items, Games, Tableware, Cake Decoration, and Confetti. These are sold at very affordable prices of course! For example, 8 pieces of party hats costs about S$3.50-6.90 while a piece range costs about S$0.40-1.30. I recommend their Glow Stick Bracelets sold at S$4.50/45 pieces.

Image Credits: mtradenoveltystore.com

With its organized website at mtradenoveltystore.com, you can either shop by price or shop by category.

Venture the Singapore nightlife without breaking the bank. Some of these night activities are even for FREE! From musical appreciation to board games feud, here are 4 Evening Activities (Under S$20) that you will surely enjoy…

1. FRIENDLY BOARD GAMES FEUD

Spend your night right by catching up with your family, friends, or colleagues at the Mind Cafe. Here, you shall enjoy hours of board games and affordable dining. Their shelves are stocked with the wildest selection of board games such as Taboo, Munchkin, Cards Against Humanity, and Say Anything. They have an ongoing promotion of only S$2/person for an hour of gaming on Monday-Thursday, and Sunday. While it is S$2.50/person for an hour of gaming on Friday, Saturday, and Public Holiday.

Image Credits: facebook.com/themindcafe

Wanting more hours of gaming? Then grab their “Happy Game Time” promotion including 4 hours of gaming and free flow of house pour drinks for S$7.90 on Monday-Thursday, and Sunday. For more details, view here.

2. WONDERFUL LIGHT SHOW

Enjoy the free “Wonderfull Show” at the Marina Bay Sands every evening from 8pm (full showtime schedule here). At the show, you will immerse yourselves in light, sound and music where your little ones will awe in delight. Remember to get there early to secure the best seats! The show is located at the Event Plaza at the Promenade.

3. ESPLANADE’S ENTERTAINMENT

From May 30 to June 1, you will have a chance to catch a live performance by the “Lorong Boys” in Esplanade Mall. The 30-minute performances at 5:30, 6:30, and 7:30 pm are all for free! Here is a sneak peek of their prowess:

Afterwards, you may indulge in a contemporary Italian and Southeast Asia bistro and bar at Level 1 called “Supply & Demand”. Majority of the pastas, pizzas, and entrées they serve are priced below S$20.

4. 2 HALFS AT SINGAPORE ORIGINALS BY GUINNESS AMPLIFY AND TIMBRE

After purchasing a beverage for less than S$20, you will witness a live band session at the Timbre @ The Substation. The 2 Halfs will be playing exclusively on May 27 from 7:30 pm. The band consists of 4 instrumentalists and 3 vocalists, adding to a total of 7 members! Drawing influences from various indie rock and alternative rock music acts, the band strives to keep their sound unique, enlivening and infectious. Want to hear a tease of their music? Listen to their SOUNDCLOUD account at soundcloud.com/2halfsband.

Image Credits: timbregroup.asia

Location: 45 Armenian Street Singapore 179936

You do not have to spend too much to have a good time with your friends or family. At the end of the day, each other’s company is enough to make the evening special. 🙂

My house has got a whole new look – thanks to the interior designers which put the furniture and fittings in place. The family car which has served us well for months has just went for a major servicing after running for another 40km. And i just had my dinner in a restaurant – a bento set prepared by Japanese chefs.

The services sector is paramount to the Singapore economy and as we get more innovative, it is not uncommon to see businesses offering different value added services to meet the demand of its people. Think Uber and Helpling.

That being said, i never let a financial planner handle my finances. Why, you might ask, since they are all services that help make the life of the common folks easier?

True. We are human beings after all and we tend to follow the path of least resistance. Why burden ourselves with the technicalities on how to fix a car or the myriad ways of where to place my sofa sets? I can definitely make my own meals, but i probably can’t dish out the the Xiao Long Bao at Din Tai Fung or to enact the perfect ambiance in a fine dining restaurant.

And if things goes wrong, the most i probably have is an upset stomach or a house that looks like a hostel. (which can be easily remedied without much repercussion)

My finances? There is more to just switching to the next better plan – my future is at stake.

Taking responsibility of my own finances

As Dave Ramsey aptly put it,

Personal Finance is only 20% head knowledge. It’s 80% behavior!

Don’t get me wrong. Personal finance can be complicated if you put the dynamics of investment and financial risk into the equation. Financial planners like the insurance agent or the bankers have their place in today modern society.

But if you are the ordinary man or woman on the street, like myself, chances are you are qualified to make your own decision. The word here is qualified and by that, i don’t mean you need to be educated in the area of Banking or Finance. If you have manage to chance upon this article, you are probably savvy enough to hook yourself onto the World Wide Web. With the internet, you can do wonders with the vast amount of information and knowledge out there – from learning how to cook a Shepherd’s Pie to planning your solo trip to Europe.

Can you manage and plan your own finances using the internet? You bet!

A website with useful resources would be MoneySENSE, a national financial education programme in Singapore. It has almost everything you need to become a financial literate – from the theoretical aspect to the nifty calculators.

Financial planning involves a few steps, and while you can budget and plan for your retirement the way you want it, there is one important factor that many have overlooked. Risk.

You can craft yourself an ingenious financial plan, but it can never be perfect should something unfortunate happen yesterday and ruin it. And that’s where insurance comes into play – to transfer the risk of loss to another party (the insurer in this case)

Encounters with insurance agents

Why would i not consult the insurance agents then? Well, i did, few years ago.

After several sessions with 3 financial advisers from different companies, i have had umpteen reminders that i need to save for retirement since i’m in my twenties. Spot on. We should always start accumulating wealth early and take advantage of the effect of compounding, where returns are reinvested to generate their own earnings.

But that’s not what i’m looking for. As i already have some money invested in the Straits Time Index Exchange Traded Funds, or STI ETF, i’m looking at covering myself with term insurance to hedge the risk of loss from unexpected events.

However, I was informed that i need to diversify my investment and/or to have another account to grow my wealth so i was recommended a whole life insurance and endowment products on the basis that i need another saving plan. I was also informed that term plans has no cash value and i’m just throwing my money into the drain.

Being the skeptical me, i was not sold to their recommendation and furthermore i have just started working with not much funds for any other products.

Online Insurance Aggregators

Only recently when i came across the news that there were websites out there that actually helps you to compare the different insurance plans from different insurers, i know it’s about time to reconsider my options.

Both are similar as they serve as a platform for consumers to compare the different insurance policies out there. They also provide handy calculators for you to work out the amount of coverage you need without consulting the insurance salesperson.

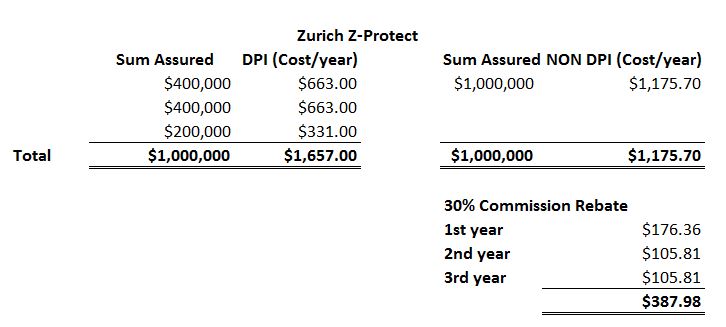

compareFIRST has a comprehensive list where you get to compare different insurance companies in Singapore. It even allows you to compare Direct Purchase Insurance (DPI), which is purchased directly from the company without any commission charged. The limitations of DPI is you can only purchase up to $400K of sum assured with a fixed term of 5 years, 20 years and up to age 65.

As i have calculated my need to insure myself up to $1 million, i could not take advantage of the more affordable DPI. I could have purchase two policies of $400K and one policy with $200K sum assured, but that is not cost-effective than if i were to purchase a single jumbo term insurance from a company.

Usually, insurance companies offer a substantial discount if you were to purchase a large term plans. I have used quotes obtained for Zurich Z-Protect in this example and as you can see, i end up paying $481.30 more a year if i were to purchase 3 separate DPI policies than a single non-DPI policy.

As its name suggest, you have to do your own planning and calculate your own needs and because of that they rebates 30% of the commission from non-DPI policies back to the customer. That works out to be a saving of around $387 (good enough to purchase a pair of Scoot economy tickets to Bangkok.)

If you think that you probably get little or no services because of doing it yourself, you are wrong.

Mr Christopher Tan, CEO of Providend said:

Instead of asking our insurance specialist to work out the insurance recommendations for you, we put that advice on the portal by way of the comparison tool. But anytime you need help or advice, you can always email, call or web chat our licensed and trained client service managers. Having said the above, when you come in for documentation, we will still do a final check for you to make sure your planning have been sound and we will still provide you with product advice, meaning, we will explain in detail the insurance you are buying.

That is basically saying you are getting your insurance with services – for less. Don’t worry about getting into sales talk with their client service managers because they are remunerated a fixed salary with no commission, so independent and transparency is the key here.

In conclusion

By taking responsibility of your own finances and doing it yourself, you not only save money but you also have a clearer picture of your own future – which means more flexibility to adapt to changes in different life stages. Would you rather be dependent and scramble to look for your insurance agent many years down the road when you get married, have your first child or buy your first apartment?