Emotions have a big influence on what we buy. As a result, it’s understandable that when anything is going on in our personal lives, it will manifest itself in our financial habits as well.

Does a little online shopping sound like the solution when you’re having a bad day? It may be as simple as picking up a new blouse or the latest pair of shoes. You convince yourself it’s not a huge cause for concern; you simply want to treat yourself to something good. Hold your horses! Making judgments based only on emotions is a proven way to give impulsive buying the upper hand.

Here’s how to stop the urge of spending money.

Have a plan

Having a plan for what you want to purchase and how much you will spend before you begin your shopping spree is a wonderful strategy to avoid impulse purchases. You will be less prone to overspending if you have a shopping list in place. It might include everything from groceries to holiday gifts for your family and friends; just make sure you know what you want to grab before you go.

Solve issues with existing products

Image Credits: sneakernews88.top

Is it really necessary to have a mobile phone holder on your workstation, or can you just rest it against a water bottle to check incoming notifications? Is it wise to purchase your kid a toy drum set when you could DIY your own? Using a little creativity, you might be able to fix problems with products you already own, or at the very least, postpone your next e-commerce transaction.

Track all that you’re spending: big or small

The smallest purchases may quickly mount up, and by the end of every month, we may be faced with buyer’s regret. The secret to effective budgeting is keeping track of your expenditures because it holds you liable for every dollar that leaves your bank account. You will be capable of making better spending decisions once you know where your money goes.

Many people begin by keeping track of their larger spending, but it’s just as vital to keep track of those minor, recurring purchases. A daily cappuccino, weekend meals out, or getting a seemingly harmless monthly magazine may add up to a lot more than you realize, and they can have a significant impact on our finances. You would have saved roughly over $100 per month if you could forego that Starbucks drink before you hit the office.

One of life’s most noteworthy temptations will always be to spend. Knowing how to control your impulses will help you get the optimum financial status possible in the future. While avoiding spending urges may seem tedious or challenging in the short term, the money you save today will provide greater options for enjoyment and financial security in the long run.

One most vital roles of parents are teaching their children about finances and success. Instilling in children the concepts of earning, saving, and investing is essential in developing life skills that they can use in the future.

Opening a bank account for kids is a good idea to train them on managing their money. It is also a surefire way to boost their educational savings and other expenses. On that note, here are five of the best savings accounts for kids in Singapore.

#1: OCBC MIGHTY SAVERS KIDS ACCOUNT

If you have S$50 to spare, you can open your child’s OCBC Mighty Savers Kids Account. Enjoy a 0.05% interest to set a head start for your child. Avoid withdrawing money from your account to get an additional 0.05%. Grow your savings even more by opting to link it up with an OCBC Child Development Account to get another 1% (i.e., resulting to about 2% interest p.a.).

Children aged 16 and below can ask their parents to open a UOB Junior Savers Account. It is a joint account with the parents, with a minimum initial deposit of S$500. The interest rate p.a. is 0.05%. Once your child ages beyond 16, the account will automatically convert into a regular savings account. This regular savings account can be used to grow their wealth during adulthood.

For parents who are eyeing for competitive interest rates, you can consider the CIMB Junior Saver Account. It offers a higher interest of 0.3% p.a. for the first S$200,000, 0.5% p.a. for the next S$800,000, and 0.3% for anything above S$1,000,000. What is the best part? There are no fall-below fees to maintain your child’s account. Set up an account online for approximately 10 minutes. It is that convenient!

Believe it or not, S$10 is all you need to open the Maybank Youngstarz Account! It has the interest rates of 0.1875% p.a. for the first S$3,000, 0.3125% p.a. on the next S47,000, and 0.3750% p.a. for anything above S$50,000. You and your child may also indulge in other benefits such as Popular bookstore vouchers and exclusive birthday privileges.

Help your child grow his or her finances by opening the POSB My Account. It works as a joint account. There is up to 3.8% interest p.a. when you convert your My Account to a Multiplier Account and it offers other benefits such as complimentary Popular bookstore 1-year student membership. The POSB Smart Buddy feature comes in handy as it automatically saves their pocket money and teaches them the importance of saving.

The term “cost of living” can be translated as the money needed to uphold our current lifestyle habits.

When finances are on a stretch, lowering the cost of living can weigh heavily on our minds. If you’re ready to hit the pause button on your spendings or make lifestyle changes because of a recent job loss or pay cut, that’s not impossible.

Downgrading can be a powerful punch in the face for the prideful. But when it comes to finances, it’s a massive boost for maintenance. Take a good look at your money matters right now and decide if it makes sense for you to downsize. Remember that selling your property takes time, so plan ahead and get started early.

But sometimes, selling your home can be made secondary by getting rid of your car instead. With most of us shifting back to working from home, maybe you don’t really need a vehicle to add to your existing financial burdens?

Rent out rooms

Image Credits: ohmyhome.com

For peeps who are not so keen on selling their house, see if you can empty a room or two to rent out. This presents a quick solution to bring in extra cash every month, on top of your salary.

Alternatively, you can also choose to downsize and then rent out a small room for someone to occupy temporarily. But this method might only be suitable for people who don’t mind sharing their living spaces with an outsider. Be sure to discuss thoroughly with your family members beforehand.

Minimise your energy consumption

Your current electricity appliances can be the culprit contributing to your steep monthly bills. Check to see if they are energy-efficient and make the switch if they aren’t. Since they are products you use for a long time to come, be sure to do your research and ask the salesperson about the specs before buying.

Another factor to consider is your air-conditioner. Yes, we get how Singapore’s weather is so humid and unbearable at times, but if you want to bring down your cost of living significantly, learn how to embrace the warmness. Can’t seem to give up on that? Use the timer setting to work your way around it when you hit the sack.

Rework your budget

Image Credits: procurementexpress.com

As we approach mid-year, maybe it’s time that you take a look at the budget you’ve drawn at the start of 2021. Changes are inevitable, and it’s okay to replan your spreadsheet to accommodate your income changes.

Study the spendings closely you have each month and maybe let go of a few inactive subscriptions. Examine if you genuinely require multiple content streaming services, or you could just do with one for the time being.

Singapore is undoubtedly a city with a high cost of living and seems to rise a little more each year. Unless you’re planning to move to another country with a lower cost of living, consider the above strategies to cut your money outputs.

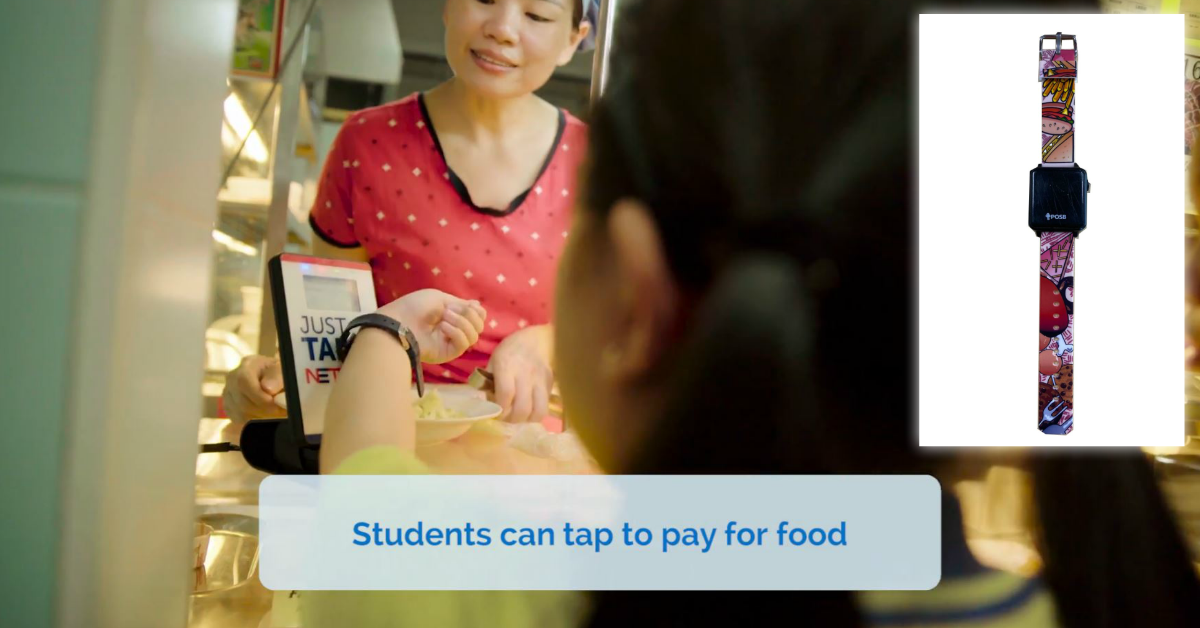

Saving is a habit that takes time to build. It’s never too early to start teaching your child the importance of saving and spending wisely. With My Account, you can keep track of how much you save and add features to meet your growing needs.

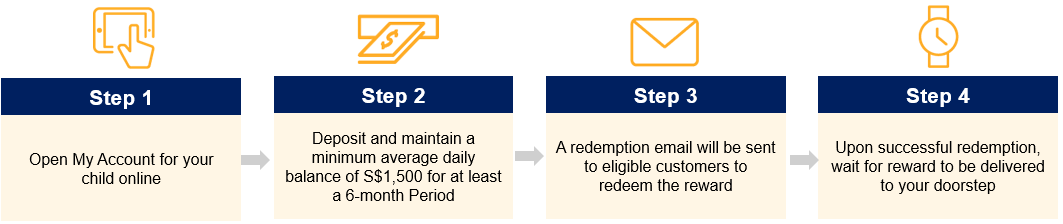

Start by opening a My Account for your child and receive a POSB Smart Buddy Watch with a Limited-Edition Strap (Worth S$45) to keep track of their daily spending.

Reward:

Receive a POSB Smart Buddy Watch with a Limited-Edition Strap (worth up to S$45)* when you deposit and maintain average daily of S$1,500 for a 6-month period.

*Limited to first 600 redemptions only, while stocks last.

How to be rewarded:

Promotion period is from 2 March 2021 to 30 June 2021.

Please prepare the following required documents prior to your application.

About POSB Smart Buddy

POSB Smart Buddy is the world’s first in-school savings and payments wearables on your child’s wrist. It lets your child tap to pay in school and at selected merchants, check on balances, and track fitness levels.

As a parent, enjoy greater convenience in managing your child’s finances and encourage smart living and saving habits – all with an accompanying mobile app.

It is fair to say that most of us want to achieve financial freedom. To have enough savings and solid investments to afford the lifestyle you wish to can sound really attractive. Unfortunately, finding that freedom can be challenging.

Many people hold debt, overspend, or encounter challenges that make financial freedom challenging to achieve. However, all hope is not lost. Develop and maintain these simple financial habits if you want to attain financial freedom.

#1: Set specific goals

A goal like “I am going to be rich one day” is vague. A better way to set targets is to use the SMART technique. They should be Specific, Measurable, Achievable, Realistic, and Time-focused.

You should be working towards a SMART aim like “I am going to increase my savings by 1% a month for twelve months.” Write your desire down in a journal, and make it your mantra. Specific goals lead to accurate results, so cut out that fluff thinking.

#2: Write a budget

Image Credits: pixabay.com

Budgeting is essential for wise money management. Instead of squandering money away and realising reason why i’m broke, it’s better to start analysing your spending habits.

Ensure your bills are promptly paid and your savings are funded before allocating money to luxury expenses or feed your lifestyle inflation. Understanding where your money goes each day is the best way to control your urge to splurge.

#3: Clear your debts

With existing debts looming over your life, financial freedom seems like a faraway dream. When you owe financial institutions money, don’t forget that the interests are rolling.

To eliminate debt, you may want to try the pyramid strategy. Pay off your smallest debt first, then allocate that money to your next-smallest bill, and so on until you have paid your debts off altogether.

We can’t emphasise enough because it’s one of the stablest ways to grow your savings. If you have a direct salary deposit from your employer to your bank account on payday, ensure a percentage of your income goes into savings right away.

It’s easy to set up recurring transfers to send money to a specific saving account every time you get paid, so you shouldn’t be giving any lame excuses. Once the automation is in, the routine will ease you into saving, so resist the urge to withdraw.

Take ownership to have at least a basic understanding of how money works – be it in the topic of debt or investments. Read books written by experts or consider taking some courses to develop your knowledge of money.

Speaking of which, do you know that Seedly is organising a Personal Finance Festival 2021? The most extensive personal finance event in Singapore is happening on Saturday, 10 April 2021, from 10am to 5pm. Read more about it here.

Yes, the market is volatile and can occasionally crash. Unforeseen circumstances can cause even the most robust markets to shrink. But without risk, there is no return. As such, the stock market is one of the greatest ways to grow your wealth.

If you know not where to get started, how about beginning your journey through Robo-advisors? From OCBC RoboInvest to DBS digiPortfolio and Stashaway, there are several local options for Singapore investors.

#7: Monitor your credit scores

Your credit score is the first thing lenders will examine when you wish to make a major purchase, such as a car or a house.

Do you know how to grab hold of your credit report? You can get a copy from the Credit Bureau (Singapore). Each CBS Credit Report is chargeable at S$6.42 (inclusive of GST). Simply make a purchase online, at any SingPost branches, at the Credit Bureau office, or CrimsonLogic Service Bureaus.

If you achieve financial freedom but then neglect your health, your hard work could go to waste due to unexpected healthcare costs. Constant exercise, eating right, and avoiding unhealthy lifestyle choices will benefit you in the long run.

While you take of your health, don’t forget to keep an eye on your things. Making sure that they last longer can help you save money.

This is true for everything, from mobile phones to laptops and cars. Keeping them well-maintained is likely to increase their lifespan and save you money on costly repairs or replacements down the road.

#9: Don’t exceed your means

Frugality is frequently on our radar, and you might have read about it in several money-themed blogs too. But you know what? It is an excellent trait for achieving financial freedom, and we’re going to play it like a broken record.

The ideal way to live within your means is to distinguish between things you want and the things you need. Just because you can afford something does not mean you need to buy it. If there’s a cheaper option out there, go for it.

#10: Talk to an expert

Image Credits: Great Eastern

Once you have accumulated some savings, talk to a professional about how to manage your money. Picking the right financial advisor who is legally obligated to act in your best interest instead of theirs is vital.

Final thoughts

While financial freedom may seem like a daunting goal to reach, it is well within your means to achieve it! Taking a disciplined approach and developing the abovementioned habits over time will help you get to your desired state of financial freedom in no time.