Some people struggle to make ends meet while others succeed in their finances. Have you ever wondered why? The answer may be a combination of different factors that play a significant role and one of them is repeated behavior. An individual’s repeated behaviors or habits are learned from young and affects the person’s decisions in the long run.

So, understanding the value of money and being taught at an early age to save your allowance, watch your spending, and note down your expenses can really boost your finances throughout your life. As the saying goes, old habits are hard to break. Without further ado, here are the Secret Habits of Financial Savvy People That You Must Adopt…

1. WATCH YOUR SPENDING

The first step is to be aware of your spending patterns and exactly how much you are spending per month and per annum. This will help you decide how much you shall save and help you to highlight the unnecessary expenses.

Recording all your expenses, no matter how big or small they may be, can help you plan your budget wisely. Find the perfect (and Free) money management app for you here.

Lastly, stop buying useless stuff that you do not need. Rethink if buying overpriced coffee rather than making your own coffee at work saves you more. Instead of buying lunch, pack your own lunch for at least 2 months. It may seem simple, but these unnecessary expenses add up.

2. SET SMART FINANCIAL GOALS

Develop a habit of financial goal setting to know where you are going and to plan how you can get there. Write down your financial goals with a witness (e.g., spouse or a close friend) and contemplate the monetary milestone you would like to accomplish in the next 2 to 5 years. Track down your monthly progress.

This habit is practiced in businesses that have quota system or in fundraising events, but it surely works for personal finances too!

3. ACCOUNTABILITY AND INDULGENCE

In most cases you must you shall practice the habit of being accountable and owning the responsibility in your spending. Be accountable of your spending by managing it and by following your financial goals. It is an important habit if you want to maintain consistency and progress.

Image Credits: TaxCredits.net via Flickr

In order for a habit or a behavior to be repeated, it must be rewarding. Set aside at least 3-5% of your income to a category called “incentive or shopping money”. I personally do this through the envelope budgeting system (learn about it here). Giving yourself a well-deserved treat after the whole month’s work will surely keep you going.

According to DEBTSteps.com, envelope budgeting or envelope system is a popular way of maintaining a budget. It starts by storing the cash into separate categories of household expenses that are allocated in separate envelopes.

1. TRACK YOUR LAST MONTH’S SPENDING PATTERNS

One of the first steps that you have to take is to analyze your spending patterns, variable expenses and fixed expenses (i.e., monthly electric bills).

Fixed expenses remain the same every month (e.g. Hand Phone Plan, or HDB Rent). Variable expenses include food, entertainment, clothing, and other expenses that may change every month or year. The challenge now is for you to choose on which expenses you can reduce.

2. DEVISE A BUDGET PLAN

Recording all your expenses, no matter how big or small they may be, can help you plan your budget wisely. Categorize your expenses 7 or more sections such as Rent, Utilities, Electricity, Groceries, Gas, Entertainment, Savings, Loan, Childcare, Tax, Travel, etc.

For example if you are Fresh graduate living in your parents’ house and you earn S$1600 a month. Allocate your money with the fixed expenses first.

Rent- S$700

Utilities- S$150

Electricity- S$80

Student loan- S$100

Fixed Expenses Total: S$ 1,080

Then your variable expenses…

Savings- S$170 (transfer it to your bank account)

Groceries- S$100

Travel- S$100

Entertainment-S$100

Emergency- S$50

Variable Expenses Total: S$520

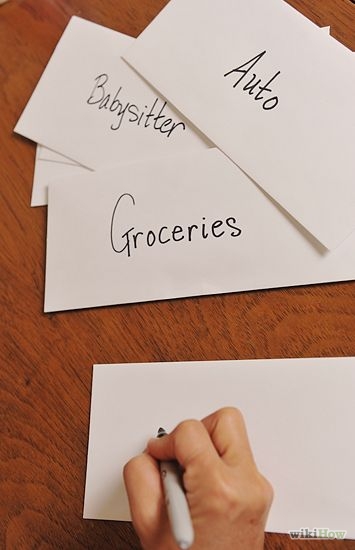

3. PUT YOUR INCOME IN SEPARATE ENVELOPES

Image Credits: wikihow.com/Do-Envelope-Budgeting

Use your marker to assign each category to each envelope. Use whatever size is best for you. It shall be able to fit easily in your purse or wallet. Follow the budget plan and allocate your money accurately. Spend only from the designated envelope and stop spending once you’ve emptied it. This practice of discipline will help you save a great deal of money.

Watch this simple video tutorial of the envelope budgeting or envelope system by NCNBlog:

Although money can seem occasionally to be easy in Singapore, many people are still concerned with saving their wealth for later. The simplest way of earning money is still saving money – this principle will also hold for 2015. No matter what position on the social ladder one is sitting on – savings and earnings are going hand in hand. The international stock market appears currently to be in a better condition than many experts had expected a few years back. Global indices are rising and markets seem stimulated, but they are hungry for more. There are, however, continuously increasing expenses, such as the recently raised credit card interest rates in Singapore. In order to stay financially on track and pay off debts on time, one should start into the New Year with certain saving strategies. When wanting to save money, one should be aware of the fact that mere saving is not effective enough. The combination of saving and investing will not only earn and save money, but also protect its value.

As the credit card interest rates in Singapore have been raised quietly in the end of last year, the hard-earning citizens have to find new ways not to loose more money. Paying the minimum rate of your credit card bill every month, will leave you in the long run with more debt than before. Even paying more than the bare minimum will not do the trick. If the full payment is not made, the interest rates will every month calculate a new and higher debt, due to the interest rate of the month before. This accumulated interest rate can let your debt rise quickly higher than initially planned, if one is only paying the minimum rate or slightly more. The debt will grow proportionately until the full amount is paid back. As the credit card interest rates have been raised about 1%, the debt is even bigger now. Therefore, it is important to pay off the credit card bill in the end of every month. In case there is no other option than stretching the credit card, one should consider a 0% interest instalment payment plan in order to save money. The credit card interest rate can be very tricky and quickly become a vicious circle that is getting increasingly harder to break out of.

Another option for saving money in 2015 is a saving account. An extra amount on the bank account can easily become a save investment. Let the money work for itself. Many experts presume that the saving account interest rates in Singapore will go up. Some banks already have some interesting offers. OCBC has a 2.35% Bonus & Saving Account offer that not only saves your money, but also makes you some more. If one has S$10000 or even more than that, one could potentially get a high and profitable interest rate for the OCBC savings account. The interest rate will go up if no monthly or quarterly withdrawals are made. The very basic rate is only 0.05%, which isn’t much at all and frankly won’t do much to your savings. However, without monthly and quarterly withdrawals, but with additionally added funds of S$10000, one can get a rate of 2.35%. But there are also other banks offering interesting rates. One other example is the 2.08% DBS Multiplier Programme. Extra amounts of Singaporean dollars that won’t be needed throughout the year, should be therefore stored on a savings account. One should watch out for changing rates throughout the year and check with one’s bank for specifics.

One should check its options though. Purely saving without investing might not do the trick. Many Singaporeans are however very interested in long-term saving programmes, such as emergency funds. If one was to save S$10000 in a year, one does have a substantial sum. However, this amount of money will surely not be the same in a decade. The inevitable inflation will decrease the value of the S$10000 eventually. Saving accounts should therefore not be the only long-term option for one’s money. Saving account can be an ideal way to save large and momentarily unneeded amounts of money. Storing money on a savings account is, however, only advisable and beneficial, if that particular amount of money will remain for a long time on the saving account. If there is a chance that one might need the money throughout the year for some reason or another, the savings account isn’t the proper place to store it. Frequent monthly or quarterly withdrawals will reduce your interest rate drastically. Furthermore, in order to protect you money from losing its value due to inflation, one should be investing as well. The combination of investing and saving is ideal.

Another trick to start 2015 by saving some money is connected to one’s car insurance. Firstly, it is advisable to check the individual policies of the car insurance. Often there are unnecessary policies that one can get rid of. Checking the car insurance’s polices one might discover that one is already covered for the same event twice. Reducing the policies to the bare minimum can help to save a lot of money. Furthermore, there are more tricks to save money with the car insurance. Increasing the deductible of your car insurance will course the premium rate of the insurance to go down. This saved money can be immediately put into a saving account and eventually used for another purchase. When wanting to buy a new car, one could start getting the money for it together a year or more before the actual purchase. Reducing one’s car insurance through different means will save money that can already finance the new car. When having finalised the purchase, one should immediately double check the insurance and eliminate all unnecessary policies. This way one can save straight from the start.

Starting the New Year by saving money isn’t the most difficult and unrealistic venture to do, but it is the combination of saving and investing that it actually makes it profitable and valuable for the individual. A saving account can be lucrative, but only if it is used properly. Therefore, one should be sure to invest and save at the same time.

Money gives people, of all ages, the decision-making opportunities they need. Educating your kids to make wise money decisions earlier on will affect their finances in the long run.

The most important thing you must do is to make saving money as fun as can be. Here are 5 Ways to Teach Kids About Saving Money…

1. MONEY INTRODUCTION

Once your children can count and discriminate, introduce them to the different denominations of money. Take a conscious effort in providing them information about money and savings and be ready in answering their countless questions.

Watch this cool way to introduce money and its values:

2. SET UP BUYING GOALS

Setting up realistic goals is the foundation to learning about the value of money and saving. Ask your children what they want to buy with their money. For instance, the toys, video games, and stationery items are the things they shall save money for. These goals will help the children learn to become more responsible.

3. USE A PIGGY BANK OR A MONEY JAR

After identifying the short-term goal, provide your child with a small piggy bank or a money jar where they can fill up their savings with. Have your child draw the picture of the specific toy on the side of the piggy bank or the money jar. Through this, they will be motivated to get what they want.

You may also want to help your child understand that some items will take longer than others to save for. For these long-term goals (e.g., going to Universal Studios), provide them with a bigger money jar.

4. ENCOURAGE SAVING

Be the good example to your children by putting some of your coins into their money jar. Since most young children want to be like their parents, seeing you do it will provide them with inspiration to save.

Aside from this, you may give them money in denominations that encourage saving. For example, give your children a $6 allowance that consists of three 2 dollar bills. Tell them to set aside $2 for their money jar.

5. PLAY GAMES INVOLVING MONEY

Image Credits: Rich Brooks via Flickr

As I said, the most important thing you must do is to make saving money as enjoyable as can be. Play games that teach children about financial concepts. Such games include Monopoly and The Game of Life. They will not only have fun but it will also shape their money management skills.

It is the beginning of a new journey entitled “2015”. There is a long way ahead and the worst is behind us. The future looks so much brighter! As you lay out your plans for the New Year, why don’t you take on the important goal of saving money?

Here are 5 Money Saving Tips from the Experts…

1. GET POSITIVE MOTIVATION FROM FRIENDS AND FAMILY

Bob Weinschenk, the CEO of “SmartyPig.com”, believes that saving money is a group activity in many cultures. By sharing your financial goals to your trusted partner, family or friends, they can be able to support you and even donate a few bucks. Having someone by your side that share the same goal will surely motivate you to continue this positive saving behavior.

Image Credits: Ken Teegardin via Flickr

2. TAKE THE SHOPPING DEALS ONLY IF YOU NEED THE PRODUCT

Donna Freedman, a writer for “Get Rich Slowly” and “Money Talk News”, said, “Coupons plus sales can easily tempt you to buy something you don’t truly need”. Do you really need to buy a bulk of toothpaste just because you have coupons and vouchers for it? Simply, when you see an item on sale think deeply if you will purchase that item on its original price.

3. LIVE WITHIN YOUR MEANS

Purchase within your means by balancing what you need and what you want.

Miranda Marquit, the founder of “Planting Money Seeds”, highlights that by knowing that you have enough purchasing power may turn into comfortable spending without keeping the best options for your finances. So, just because you can afford something, does not mean that you should buy it.

4. THINK TWICE WHEN BUYING PERISHABLE GOODS IN BULK

Jeff Yeager, the author and host of “The Cheap Life”, said “it’s not a good deal if it goes bad before you use it”.

This is why he stresses the importance of making a shopping list and sticking to it.

5. LASTLY, LEAVE YOUR CREDIT CARDS IN THE HOUSE

Stacy Johnson, the President of “Moneytalksnews.com”, said, “we’re more likely to overspend with pieces of plastic than real money”. Personally, when I shop, I only carry cash that I am willing to spend so I won’t go over budget. This prevents impulse buys.