Health has long been associated with wealth. According to this age-old proverb, good health plays a vital role to reaching a prosperous life. Having poor immune system may lead to more abseentiesm at work or at school. Furthermore, you illnesses are usually accompanied by medicines and medical fees. You waste time and money when you are constantly sick.

The good news is that the Ministry of Health (MOH) has established the National Adult Immunisation Schedule (NAIS) for Singaporeans aged 18 and beyond. You are encouraged to protect yourselves against vaccine-preventable diseases under the NAIS. In the beginning of next month (November 1, 2017), you will be allowed to use your Medisave to acquire recommended vaccinations for the specific population groups that you belong to.

To reduce confusion, I am highlighting that Medisave is different from MediShield. Medisave is the national medical savings account that Singaporeans need to fulfill to cover future medical needs. Individuals or your employers need to regularly contribute as long as you are employed. On the other hand, MediShield is a low-cost medical insurance scheme aimed to pay for larger hospitalization bills.

Now that you are enlightened about Medisave, I must eagerly note that this vaccination scheme is highly encouraged. However, it is not mandated! You are free to discuss your vaccination needs with your trusted physician. You do not want to be allergic to the ingredients of a particular vaccine (e.g., the latest Influenza shot I took was not suitable to individuals who are allergic to egg)! That will only make matters worse.

If you wish to use your Medisave, you must ask your healthcare provider prior to the vaccination. You will be able to use up to S$400 at public healthcare institutions, Medisave-accredited GPs, and private hospitals. The eleven diseases covered by this scheme are:

(i) Influenza;

(ii) Pneumococcal (PCV13/PPSV23);

(iii) Human Papillomavirus (HPV2/HPV4);

(iv) Tetanus, Diphtheria and Pertussis (Tdap);

(v) Measles, Mumps and Rubella (MMR);

(vi) Hepatitis B; and

(vii) Varicella.

Let us part ways with the significant words stated by the Senior Minister of State for Health – Dr. Lam Pin Min.

Image Credits: pixabay.com

“Vaccination provides a person with protection against infectious diseases, and is one of the strategies to reduce the risk of disease outbreaks in the community. While the coverage for vaccinations under the National Childhood Immunisation Programme has been high for most of the vaccines, there is low awareness of the benefits of adult vaccination for personal protection and protection of at-risk family members. With the introduction of the National Adult Immunisation Schedule (NAIS), we hope to encourage Singaporeans to take up the recommendations made in the NAIS, to protect themselves and their loved ones against the relevant infectious diseases.”

I believe it is safe to say that “Insurance” is an unfamiliar territory for most Singaporeans. For young adults who recently joined the workforce, it is a necessity that comes with the new responsibilities of adulthood. Weighing your insurance options is just the start!

You may have encountered policy terms such as premiums and deductibles. However, do you know what each term means? I shall focus on the former.

DEFINING INSURANCE PREMIUM

In its simplest form, an insurance premium is the amount that an individual or an institution must for upon signing on a policy. It represents a bind that the insurer must provide coverage for the claims made against the policy. More so, it is the income earned by the insurance company.

HOW INSURANCE PREMIUM IS CALCULATED

There are many interacting factors that affect the prices of the insurance premium. For starters, the price heavily depends on the type of insurance (e.g., Critical Illness policy or Car Insurance policy). Other factors include the area where the policyholder lives, the likelihood of claims being made, the behavior of the policyholder, and the amount of premium offered by the competition.

Let us take the Life Insurance policy as an example. Various factors affecting your specific premium include the:

a. policyholder’s age at present time,

b. scope of coverage that the policyholder buys,

c. length of the policy,

d. and the policyholder’s life and health expectancy.

WAYS TO ACCOMPLISH PAYMENT

Singaporeans were blessed with a number of options when it comes to paying for the insurance premiums. Some insurers require the policyholder to pay for the total amount before the coverage starts. While, others offer installments (e.g, semi-annual payments).

It is vital to highlight that you may encounter situations that entail the increase of insurance premium. Firstly, it may increase after the policy period ends. Secondly, it may increase if you made claims during the previous period. Lastly, it may increase if the risk associated to the type of insurance gets more pervasive.

Image Credits: pixabay.com

THE BOTTOM-LINE

In summary, the insurance premium is the amount of money charged by the insurer for an active coverage. The total amount depends on multiple factors including age and address. Individuals may pay premiums annually or in smaller amounts over a year. Also, this amount changes over time. The policy is usually voided when the insurance premiums are not paid.

The traditional mode of how insurance is sold is a frustrating process for most people. Consumers do not know where to start when it comes to getting insured. In many cases, there is a sales-pitch and high pressure selling from advisers who have a conflict of interest.

To address these needs, Do It Your-way Insurance (DIYInsurance) was launched in 2014 to empower people to make informed decisions about their own insurance purchase and they started Singapore’s 1st Life Insurance Comparison Web Portal for users to compare insurance products and provide greater transparency. To-date, more than 150,000 users have used DIYInsurance.

Consumers find it difficult to know where to start when it comes to getting insured. To help consumers obtain an assessment of their life insurance needs, they have recently launched Selfcheck, Singapore’s 1st digital adviser to bring insurance planning to the next high level.

This is like having an insurance adviser help you with your insurance check-up and providing instant advice, but without you feeling the obligation to buy anything.

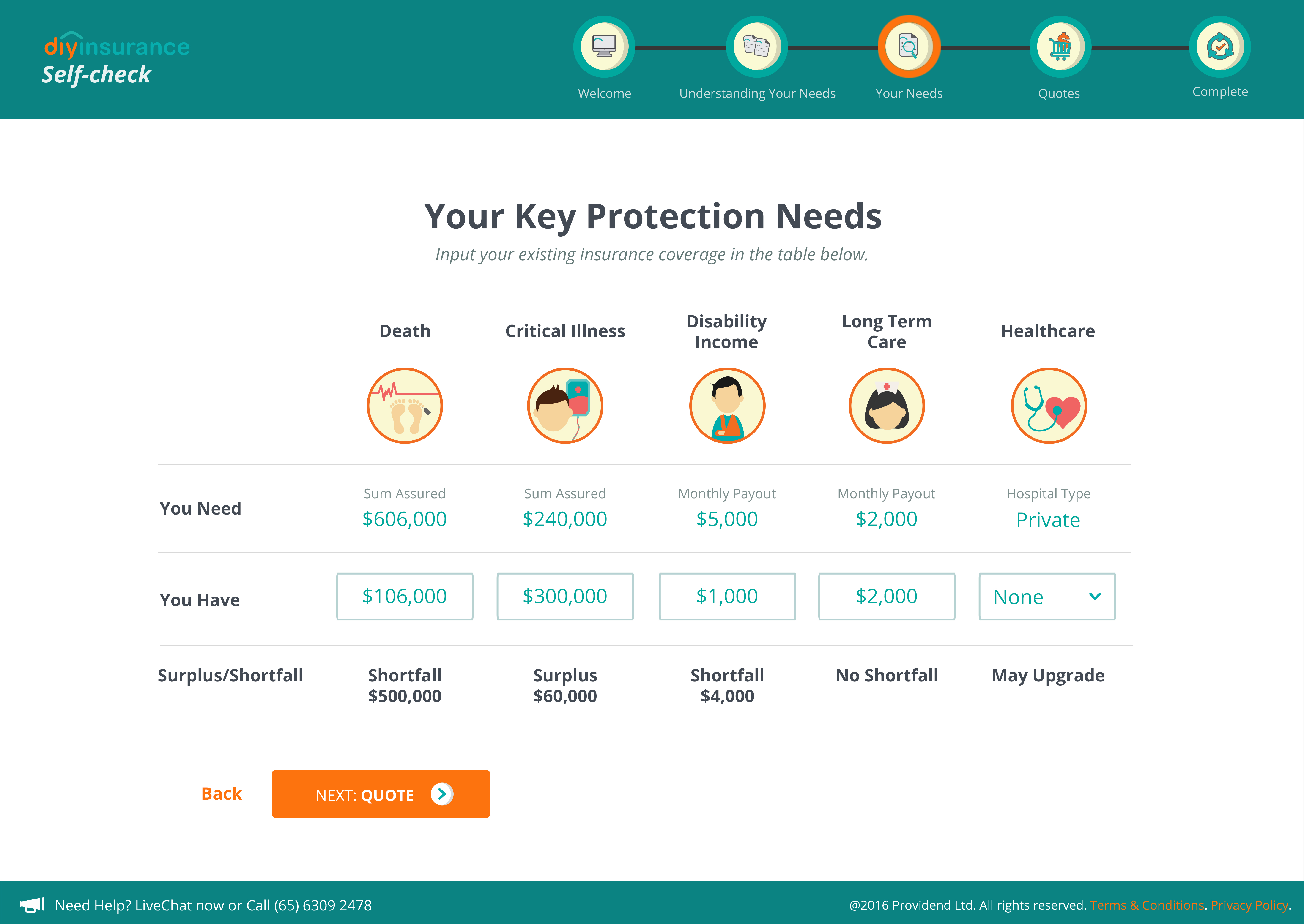

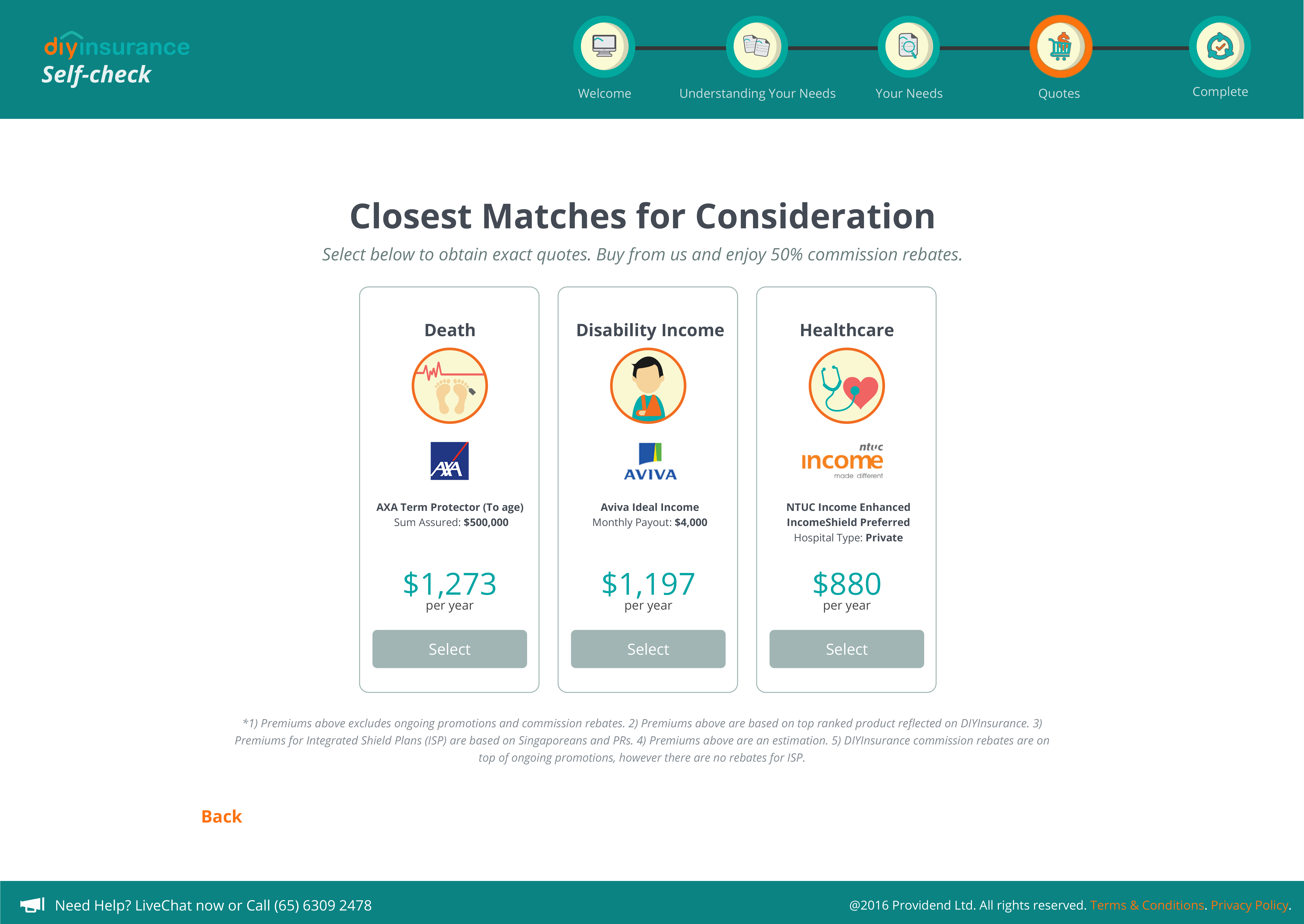

You can easily uncover:

types of insurance you really need

how much insurance you require

surplus or shortfall in your insurance coverage

recommended policies to meet your needs

Everyone can now perform a Selfcheck and obtain a customised and tailored insurance solution from a place they can trust.

The DIYInsurance Difference

Expert advisers to assist you

When you plan your insurance with DIYInsurance, they assign a dedicated expert insurance adviser to complete your planning process. Simply put, you use Selfcheck to build your own insurance plan and the human insurance adviser act as your guide to complete the process by fine tuning your plan. This is insurance advice at its best.

Honest advice

To avoid conflict of interest, all of their insurance advisers are salaried-based and not remunerated on a commissions-basis hence there is no incentive to hard-sell and push products that reward higher commissions. DIYInsurance wants to provide the most honest, independent and competent advice to their clients.

Dedicated after-sales service

If there are any claims or after-sales service requirements, you not only can approach your adviser, DIYInsurance has an entire team of Client Service Managers who stand ready to assist you. All you need is to contact them and they will do everything for you.

It is critical is that there is a trusted DIYInsurance adviser and a client service team whom you can always go to. DIYInsurance is not just High-Tech, they are High-Touch.

Lower Cost

With Selfcheck, the insurance process is made more efficient and hence they are providing greater cost savings to their clients by increasing their commission rebates from 30% to 50%.

DIYInsurance rebates 50% of the salesperson’s commissions to their clients and retain the remainder of the commissions as their service fees. These rebates to their clients are on top of ongoing policy promotions offered by the insurers and they rebate the commissions for as long as the insurer pays them on a policy which could be over a period of 3-6 years.

Expertise

Started by Providend Ltd, a licensed financial adviser and registered fund management company with the Monetary Authority of Singapore (MAS) since 2003, the key leaders of DIYInsurance are Chief Executive of Providend Ltd Christopher Tan, MBA, CFP® and Head of DIYInsurance, Eddy Cheong, CFP® whom each have almost 2 decades of experience in the wealth management industry. All DIYInsurance advisers are licensed with the MAS.

Summary

When you plan your insurance needs through DIYInsurance, what you get is quality, transparent and conflict free advice at a much lower cost from a trusted place. Best of all, you can do all this at the comfort of your desk, without feeling the pressure that you need to purchase something. In addition, you still get all the help needed when you need to claim against your policies. That is why DIYInsurance is not “Do It Yourself Insurance” but “Do It Your-Way Insurance”. Try Selfcheck today!

In its fundamental form, insurance is a contract that enables individuals or entities to receive financial protection against losses. It ensures the stability of families and businesses after a crisis or other unfortunate events. Simply put, insurance grants policyholders a peace of mind. Isn’t that what everybody wants – to be able to sleep at night without having to worry about what the future holds?

These are the reasons why I am drawn to getting insurance policies. I have to be completely honest. One of the major drawbacks that I dislike about insurance is its complexity. I am apprehensive about the piles of questions and bulky documents. Do not get me started about the confusing technical terms!

To my delight, I was introduced to a revolutionary insurance company that dances gracefully with the modern tides. This was none other than FWD Insurance. FWD Insurance aims to transform the way that Singaporeans experience insurance by simplifying the purchase and claims process. It helps you to skip the agent by directly working with them online.

Say goodbye to nerve-wracking call backs and time-consuming interrogations by embracing their user-friendly website!

FWD Insurance understands how valuable a working Singaporean’s time and money is. This is why the company maximizes these two commodities through providing insurance quotations under 60 seconds for car insurance and 10 seconds for travel insurance. These impressive figures are due to the fact that FWD only asks questions that are absolutely necessary.

For instance, it took me 25 seconds to be quoted with the premium of about S$174 for a DIRECT-Term Life insurance that seeks to cover 5 years of my life. I used the rest of my day to focus on other productive matters. You can do the same thing too!

The people behind FWD best explained the company’s concept: “We believe that insurance doesn’t need to be complex, sold through middlemen, or take up vast amounts of your time.” It offers competitive prices and easy-to-understand insurance.

Attractive Insurance Products

It is usual for people to feel skeptical when they encounter an insurance company for the first time. Wash away this feeling by knowing that you are supported by a company with a strong financial record. FWD is the insurance business arm of the established investment group, Pacific Century Group (PCG).

Choose from the four secure insurance products such as DIRECT-Term Life Insurance. Car, Travel and Personal Accident.

A. DIRECT-TERM LIFE INSURANCE

The DIRECT-Term Life insurance ensures that your family’s financial future is secured despite unfortunate events such as becoming diagnosed with a critical illness, becoming permanently disabled, or passing away.

These are the primary reasons why I am drawn to this policy:

I can choose the period that works for my budget and lifestyle (e.g., 5 or 20 years).

I can purchase coverage through my smartphone – without going through a middleman.

Because FWD does not pay commission to agents, my coverage of up to S$400,000 may cost less than S$1/day.

B. CAR INSURANCE

Three comprehensive plans cover vehicle repairs, third-party damages, medical expenses, and roadside assistance. These plans were crafted to suit your personal needs and budgets.

No matter what plan you avail, your repairs will be completed by the FWD workshops. You can cruise along blissfully until your car turns ten. Furthermore, your 50% NCD is guaranteed for lifetime. NCD stands for no-claim discount. Drivers who have earned their 50% NCD get to keep it for life because they believe that one accident doesn’t make you a bad driver.

On top of that, you can add amazing features which gives you coverage when you are driving in West Malaysia and certain parts of Thailand.

C. TRAVEL INSURANCE

Take for instance; to reap the rewards of her hard work, Jena scheduled a weeklong vacation to Thailand. The beautiful country has so much to offer from pristine beaches to established sports clubs. She did not forget to pack her favorite S$200 golf putter. To enjoy a fuss-free tropical getaway, she purchased FWD’s travel insurance. It was one of the best decisions she ever made as the putter got lost in the airport and fortunately, sports equipment is covered by the policy.

Aside from sports equipment, the travel insurance also includes unlimited medical evacuation. You read that right! The last thing on your mind is how much your emergency evacuation will cost. This is why FWD has thought of this for you.

You can expect the claiming process to be a breeze too. Claim with a few clicks with the “Click to Claim” feature. This means, all you have to do is snap your boarding pass and claim for flight delays via WhatsApp. This feature is available for baggage delays too. Simply take a photo of your baggage slip and send it to FWD via WhatsApp. That is convenience at its finest!

D. PERSONAL ACCIDENT INSURANCE

Personal Accident (PA) insurance provides compensation in the event of disability, injuries or death. In fact, one feature unique to FWD is that the policy also covers the most number of infectious diseases including Zika and dengue fever. Under this policy is the Guardian Angel Benefit. If both parents pass away or become permanently disabled due to an accident, FWD will provide up to S$500,000 for the surviving children.

Lastly, natural circumstances now cannot stop you from having fun as ticketed event cancellations due to haze are covered. Apparently, they are the only insurer in Singapore to offer this.

Irresistible Features and Highlights

Before you make a commitment, it is important to know what this new insurer can do. Let me start by stating the fact that there are no middlemen or agents. Since you do not have to pay for commissions, you can save more money.

FWD allows you to complete your purchases online. It is so quick and easy to complete the online quotation that even your 9-year old niece can do it for you! As soon as you make your purchase, you will get an email with the policy. You will also receive an SMS that notifies you to check your email.

Lastly, the policies are delivered with no technical terms. You will know exactly what you will get explained in plain English.

From now till 31 January 2017, you can now enjoy a 10% discount on all FWD insurance products with this promo code – FWDHi10.

For the people behind FWD, customers are at the heart of the entire process. They let you experience exceptional insurance by minimizing your effort and making products readily accessible. May they change the way you feel about insurance!

There is a new trend circulating the insurance market. This trend is none other than women’s insurance. Have you heard of this?

I cannot deny the fact that women are more prone to certain diseases due to the workings of the female body. Health issues such as pregnancy complications and ovarian cysts are peculiar to women. Some of these health conditions are not covered by life or health insurance due to its exclusivity. This is why women face encouragement to add special riders. But, this scenario is a thing of the past! More and more insurers are offering women-centered maternity and critical illness plans.

Parents who are experiencing the miracle of childbirth for the first time can be overtly “kancheong” (tensed). Who can blame them? Maternity is a vulnerable period that you must not take lightly. To safeguard yourself and your child, you may purchase maternity insurance policies. Some of them are in the form of bundled plans to cover the child’s needs beyond the early stages. Consider signing up for the “PINKLIFE” by Great Eastern Life Assurance.

PINKLIFE covers allows the policyholder to feel safe while she is pregnant. Women (between ages 17 to 40) have the option to upgrade their plans to include coverage for pregnancy-related conditions such as stillbirth or miscarriage due to accident. The newborn will also be covered for premature birth requiring ICU care and congenital conditions (e.g., Down’s Syndrome). This plan stands out from the rest because is protects the policyholder from 37 critical illnesses too.

Image Credits: pixabay.com

Aside from maternity bundled plans, insurance policies for women occur as critical illness insurance. Critical illness (CI) insurance usually pay a lump sum when an individual is diagnosed with a disease covered in the terms. It is important to note that most policies depend heavily on the policyholder’s age. Insurers will charge you with a higher premium if you belong to an older age group. This is because the risk to certain diseases increase as age does. So, examine the point of coverage. Is their an age allowance? How about a “stage” allowance (e.g., the coverage takes place only at the early stages of breast cancer)?

As this CI policy is targeted at women, you can commonly find that some of them offer free health checkups such as mammogram. Speaking of free health checkups – I introduce you to the AIA Glow of Life. It is a CI that is especially made for women. You may enjoy a complimentary medical checkup every two years starting from your 3rd year with the policy. It gives you payouts for a wide range of illnesses including breast cancer, osteoporosis, and rheumatoid arthritis.

What’s more? Policyholders can expect to gain from a 100% reimbursement for a reconstructive surgery due to an accident.

While some insurers offer standalone women-centered plans, others do not. Please make sure to read the fine print to understand what you are covered for! Feel free to contact a financial adviser for an appropriate consultation.