Gold prices soared to a new all-time high during early Asian sessions on Monday, with spot gold breaking above US$3,100 an ounce for the first time in history. The surge comes as growing political tensions and financial market jitters continue to push investors towards safer assets.

The rally was largely driven by mounting fears of a global trade war, sparked by U.S. President Donald Trump’s latest move to impose new tariffs. The development has heightened uncertainty across global markets, prompting a flight to safety and driving strong demand for gold.

Image credit: Dhaka Tribune

With both geopolitical and economic tensions rising, gold is once again proving to be the go-to safe-haven asset.

This sharp uptrend marks a continuation of gold’s bullish streak in recent months, supported by broader concerns around slowing global growth, volatile stock markets, and a weaker U.S. dollar. The latest price action reflects just how nervous investors have become amid shifting policies and uncertain global outlooks.

This judgment-free guide promises to change your mindset around finances one cent at a time.

Drawing from the author’s journey to financial independence, Shang Saavedra shares an empathetic memoir and a mindset-changing methodology to help readers make peace with money.

Through concrete applications of her step-by-step process, you will learn to overcome emotional hurdles and take mindful actions to improve your finances.

Let’s be honest, ladies: managing finances can feel like a hassle you would rather avoid.

But not dealing with money is putting your future at risk.

“What’s Up With Women and Money?” is a relatable guide to key money topics like investing, car buying, and paying down debt.

Author Alison Kosik breaks down these often-intimidating subjects into crystal-clear steps you can tackle today.

Through real women’s cautionary tales of avoiding money decisions, you will gain the motivation to get savvy.

Kosik’s judgment-free approach, digestible advice, and accessible writing style make this a must-read for any woman seeking to feel confident about her finances.

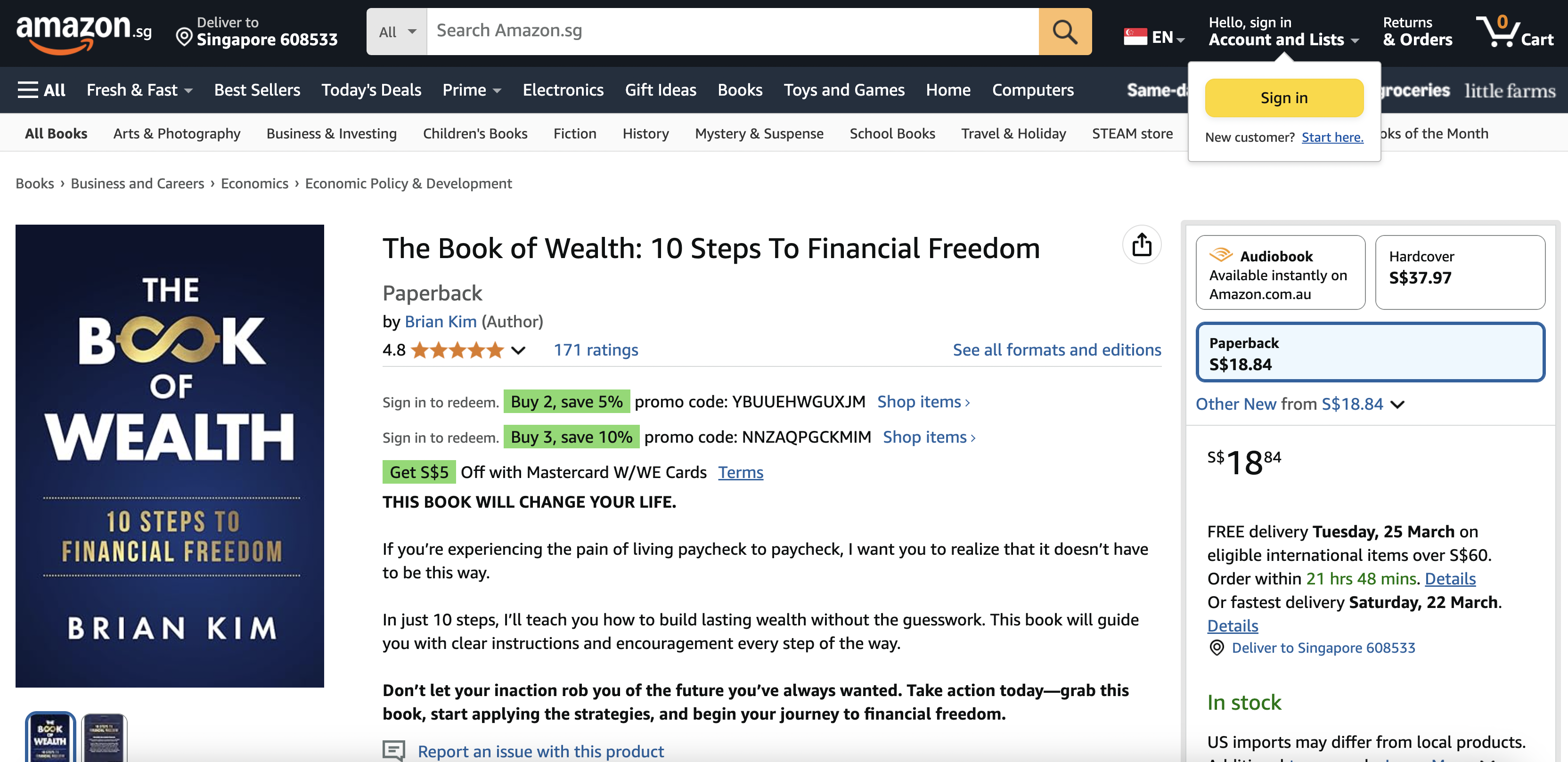

This life-changing book is your roadmap to real and lasting wealth.

In just 10 clear steps, the author Brian Kim guides you through an actionable plan to go from financial stress to freedom.

Implement Kim’s simple yet comprehensive system for taking control of your finances once and for all.

Packed with straightforward instructions and an encouraging, motivational tone, The Book of Wealth empowers you to break the cycle of barely getting by.

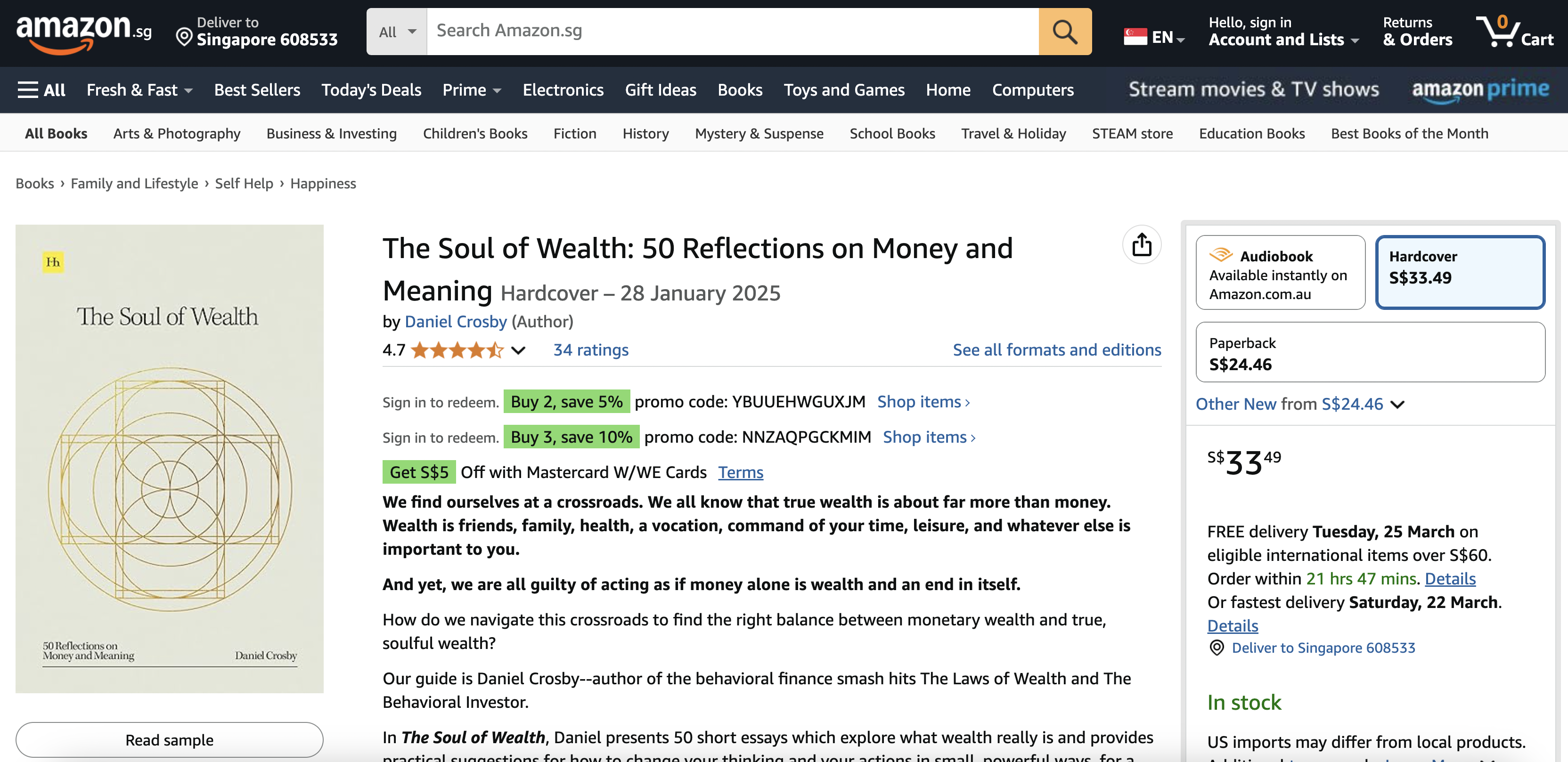

In this groundbreaking collection of 50 essays, Daniel Crosby challenges us to rethink our entire relationship with wealth.

With thought-provoking insights, “The Soul of Wealth” digs deep into the true meaning of money and how spending it mindfully can lead to a richer life.

Short but impactful, these reflections reveal how willpower isn’t everything, why some risk is worthwhile, and how delayed gratification pays dividends.

You will gain a fresh perspective to change your financial thinking in small, powerful ways.

The Singapore stock market is influenced by a wide range of factors, both global and domestic. These elements shape investor confidence, market performance, and stock prices. Understanding the following factors can help investors make better decisions.

ECONOMIC CONDITIONS

The overall health of Singapore’s economy plays a big role in the stock market. Important factors like economic growth, inflation, unemployment, and trade balance affect investor confidence and stock prices.

GLOBAL MARKET TRENDS

Singapore’s stock market is connected to major international markets like the US, China, and Europe. If these markets go up or down, it can influence investor decisions in Singapore as well.

INDUSTRY PERFORMANCE

Different industries such as technology, finance, shipping, and real estate impact the stock market. If a sector is doing well, stock prices in that industry may rise. If it struggles, prices may fall.

COMPANY NEWS

Stock prices can change based on company announcements like earnings reports, new products, leadership changes, or business updates. If a company performs well, its stock price usually goes up. If it faces challenges, the price may drop.

GOVERNMENT POLICIES/REGULATIONS

Changes in government rules, taxes, and financial policies can affect the stock market. Policies that encourage business growth can boost investor confidence, while stricter regulations may create uncertainty.

INTEREST RATES

The Monetary Authority of Singapore (MAS) controls interest rates. When interest rates go up, people may prefer safer investments like bonds instead of stocks. When rates go down, stocks become more attractive.

CHALLENGES FACING THE SG STOCK MARKET

On July 13, 2024, a report stated that Singapore’s stock market had reached its lowest point. Investors have been worried about low liquidity and weak stock prices, making the market seem less attractive. Many describe it as boring and unexciting.

One major problem is that fewer companies are listing on the Singapore Exchange. At the same time, many companies are choosing to leave the market. This has created a cycle where low activity discourages new investors, making the problem worse. Experts have noted that in the first half of 2024, Singapore had only one small new company listing on its stock exchange.

WHAT TO EXPECT THIS YEAR

As we move into 2025, experts are uncertain about how Singapore’s stock market will perform. Global interest rates and trade restrictions could impact the market, especially as the United States gets a new president.

Image Credits: unsplash.com

Economists believe 2025 could be a tougher year than 2024. Singapore’s economy relies on trade with China, the US, and the European Union. If these economies slow down, Singapore’s stock market may struggle.

IN A NUTSHELL

The Singapore stock market faces some challenges, but investors who understand these factors can make better decisions. Market conditions may be unpredictable in 2025, but keeping an eye on global trends, government policies, and industry performance can help investors find opportunities in the Singapore Exchange.

They say time is money but when it comes to investing, time is actually wealth. In Singapore’s fast-paced economy, understanding the magic of compound interest can be the key to financial freedom. So, how does it work?

POWER OF COMPOUNDING

Think of compound interest as a snowball rolling down Bukit Timah Hill small at first, but growing bigger as it gains momentum. In finance, this means your initial investment earns interest, and that interest starts earning more interest over time. The longer you leave your money to grow, the bigger the effect.

Let’s say you invest S$10,000 at an annual return of 5%. In a year, you’ll have S$10,500. But in the second year, you’re earning interest not just on your original S$10,000, but also on the extra S$500, bringing your total to S$11,025. Fast forward 20 years, and your initial sum has nearly doubled without you lifting a finger!

WHY START NOW?

Singapore’s CPF system already takes advantage of compounding, but you can supercharge your wealth with investments in ETFs, stocks, or savings plans. The trick? Start early and stay consistent. The longer you let your money grow, the more time does the heavy lifting for you.

Image Credits: unsplash.com

So, whether you’re saving for your first BTO or early retirement, remember: wealth isn’t just about how much you earn it’s about how wisely you let time work for you.

I’ve been on the lookout for a credit card with the best rewards and after some research, I stumbled on this combo:

UOB Lady’s Credit Card x UOB Lady’s Savings Account

I’m excited to make the most out of my savings and spending, knowing that signing up for both can earn me up to an impressive 25X UNI$ per S$5 spent, equivalent to 10 miles per S$1!

How It Works for Me:

UOB Lady’s Credit Card: I earn 10X UNI$ per S$5 spent on up to two of my preferred rewards category(ies). That’s 4 miles for every S$1 I spend.

UOB Lady’s Savings Account: I boost my rewards with up to an additional 15X UNI$ per S$5 spent on my preferred rewards category(ies), adding up to 6 more miles per S$1.

Plus, there’s no lock-in period, giving me the flexibility to choose and change my preferred rewards category(ies) every quarter.

And the best part? There’s no minimum spend required, allowing me to earn rewards on my terms!

Painting the Picture:

I have plans to maintain a S$50,000 Monthly Average Balance (MAB) in my UOB Lady’s Savings Account and spend S$800 each month on my preferred rewards category(ies) with my UOB Lady’s Credit Card.

For me, a monthly S$800 spend is easily attainable since I spend the bulk on the Beauty & Wellness and Dining categories.

Here’s the rough breakdown if you’re interested:

Gym membership ($100)

Beauty/cosmetic buys ($100)

Personal grooming such as hairdressing, facial treatment/hair removal, nails/lash/eyebrows, etc. ($300)

Dining at my favourite restaurant and ordering food via foodpanda ($300)

This means in just one month, I could rack up 3,200 UNI$.

Keeping this up for 12 months means I could gather a whopping 38,400 UNI$ in a year!

Redeeming My Rewards:

I can convert these UNI$ into 76,800 KrisFlyer miles (1 UNI$ = 2 miles).

With that, I could snag my round-trip business class ticket to Hong Kong* within a year! It would be my first-ever business class experience.

But if I decide not to spend all my UNI$ on flying, I have plenty of other options too.

I can redeem my UNI$ for rewards from a variety of dining, shopping, and travel merchants on UOB Rewards+.

In essence, whether I’m aiming for luxury travel or indulging in simple everyday perks, the benefits add up quickly!

*Based on Singapore Airline’s Saver Awards Chart as of October 2023, excluding taxes, charges, and fees.

Maximizing Your Rewards:

You can choose and change your preferred rewards category(ies) every quarter. These include:

Dining

Travel

Fashion

Beauty & Wellness

Family

Transport

Entertainment

This flexibility means you can adapt as your spending habits and priorities shift.

Switch to whatever categories you deem fit quarterly to maximize your UNI$ and get the best rewards for your spending and savings!

For example, during the year-end holiday season, I can switch my rewards category to Travel. This allows me to book air tickets and easily hit the S$800 spending target in a single transaction!

By consistently managing my spending, I can easily accumulate a significant amount of UNI$ annually. During travel months, I can reach the monthly spending target even faster by booking air tickets and covering other travel expenses.

If you have more savings to park aside and can maintain at least a S$100,000 MAB, you can earn an additional 15X Lady’s Savings Bonus UNI$ on your preferred rewards category(ies).

So, it’s smart to consolidate your purchases with the Lady’s Credit Card to maximize your Lady’s Savings Bonus UNI$.

Curious About Your Rewards?

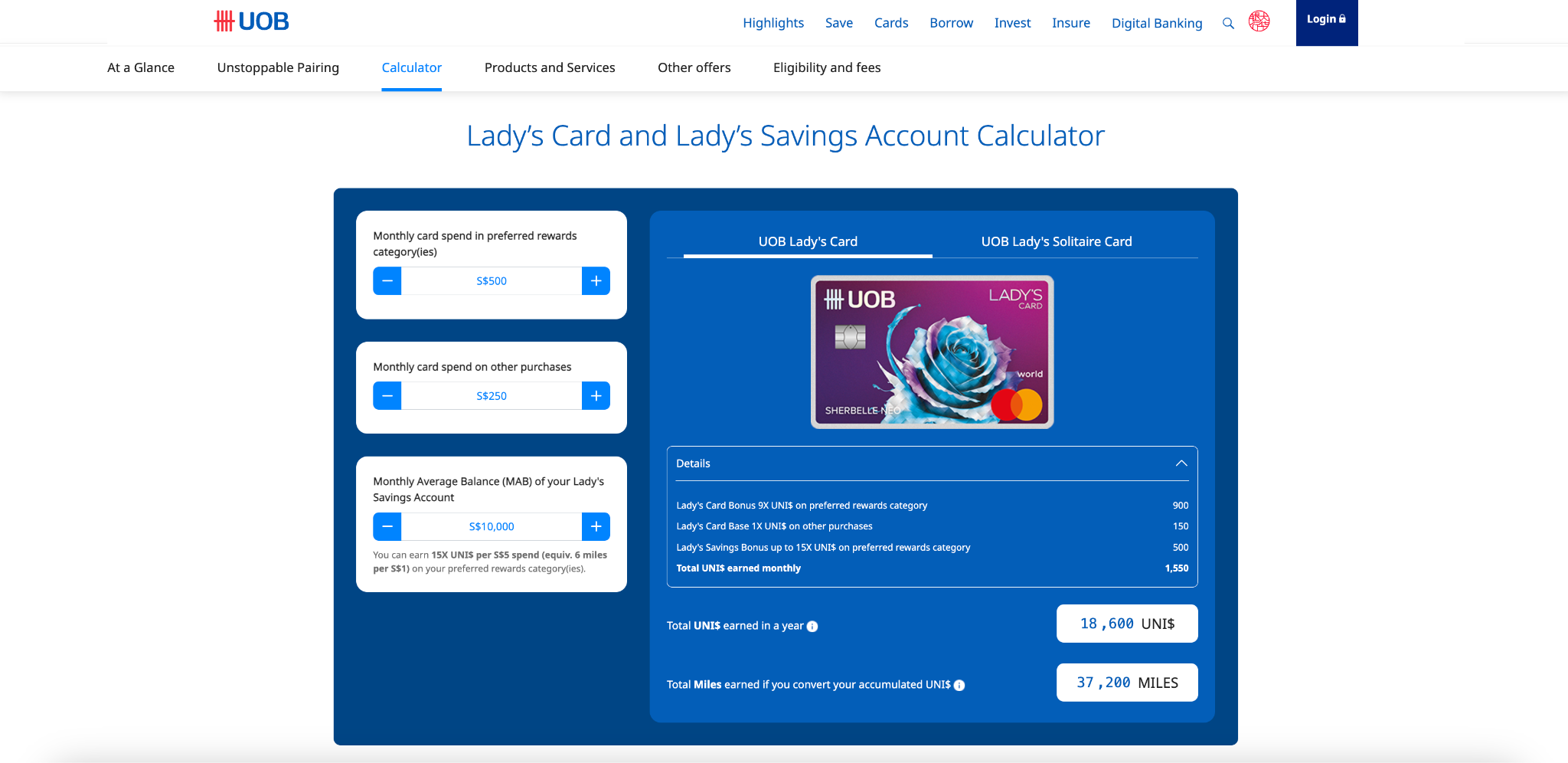

Wondering how many UNI$ and miles YOU can rack up based on YOUR spending and savings?

Simply click this link to UOB’s official website and click on ‘Calculator’ to access the ‘Lady’s Card and Lady’s Savings Account Calculator’ to enter your details and see your potential rewards in a flash!

Just like this:

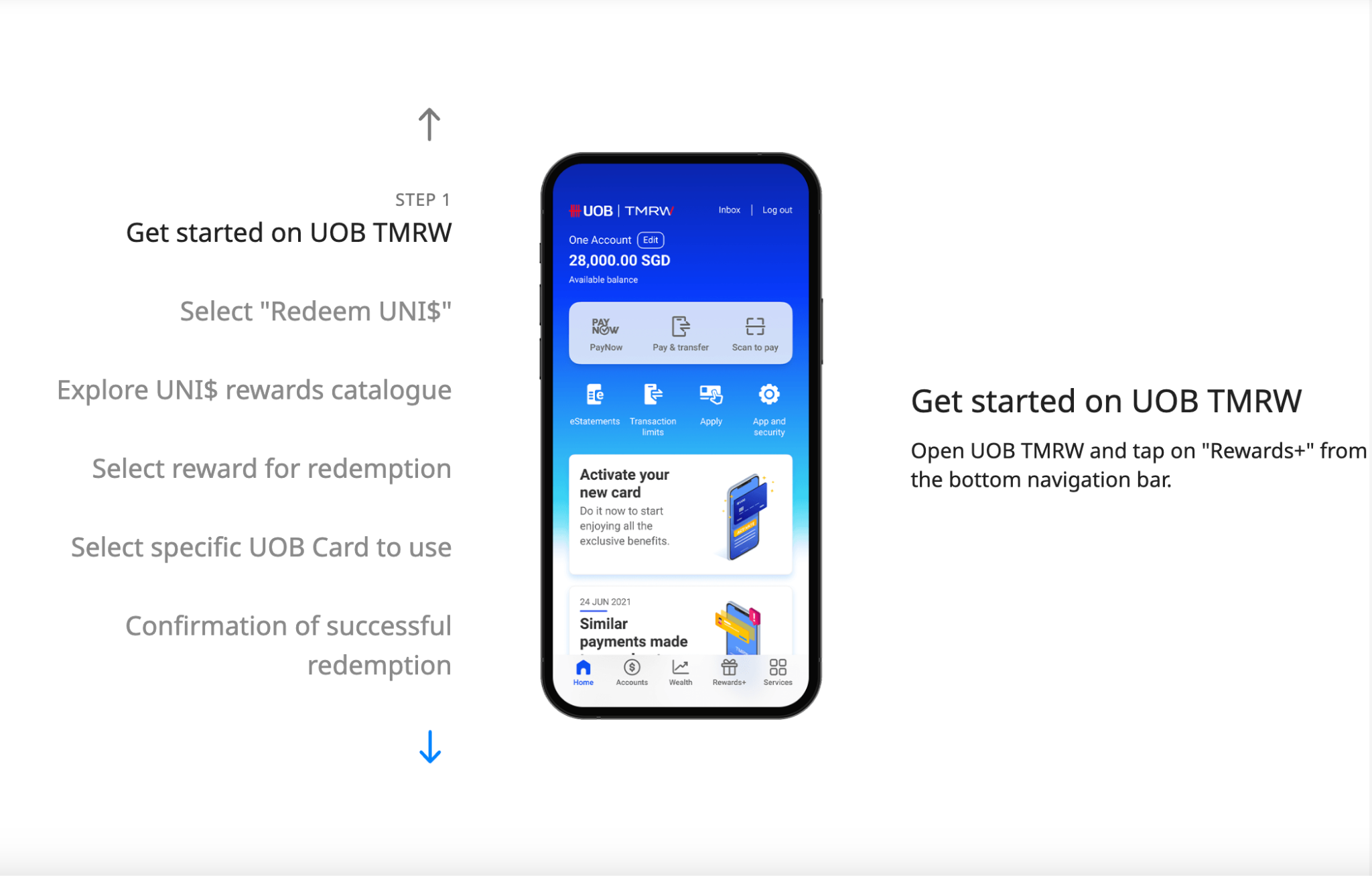

Subsequently, as a card member, you can easily view, track and redeem your UNI$ rewards all on the UOB TMRW app.

0% LuxePay Interest-Free Payment Plan over 6 or 12 months on your luxury purchase (shoes or bags)

Exclusive Birthday Treats during your birthday month

e-Commerce Protection for your online purchases

Complimentary Travel Insurance covering up to 100,000 USD

Receive a S$250 Sephora Gift Card when you spend a min. of S$6,000 on your UOB Lady’s Credit Card. Limited to the first 280 eligible cardmembers.

For the UOB Lady’s Savings Account:

Receive a Bespoke Puffy Bag with Rose Leather Charm worth S$98 by reBynd, an eco-conscious brand by Bynd Artisan, when you apply for the account online and deposits S$5,000 new funds into the account. Limited to the first 150 customers in each calendar month from 8 March to 30 April 2025 only.

That’s not all. UOB is also rewarding ALL customers who hold both the UOB Lady’s Credit Card and UOB Lady’s Savings Account as of 30 Apr 2025 with a lucky draw chance to win an Éclat KNOT Alone® Double Pave Bangle worth S$520 or Gentle Monster sunglasses worth S$490.

T&Cs apply, of course. Insured up to S$100k by SDIC.

So stop waiting and join me right away by signing up now here.