Catching the attention of your potential customers is an easy task if you know exactly what you are searching for. So, begin by defining your target audience. Be as detailed as realistically possible. Include descriptors such as gender, occupation, NRIC number/FIN, hobbies, age group, and civil status.

Say you are selling Harry Potter merchandise to teens and other millennials. You noticed that they are immensely obsessed with social media platforms. Hence, you used Instagram and Snapchat to identify your potential customers.

Image Credits: pixabay.com

PROVIDE AN INVITING ATMOSPHERE

Charming your customers start as they enter your doorstep or website. Flashy signs may draw them in, but your accomodating gestures will make them stay. Send warm greetings and show new customers around your vicinity. This will make them feel appreciated and special.

This is certainly true if you are in the food business. Ushering your hangry customers with a friendly service can help them calm down. I cannot remember how many times this happened to me!

OFFER TEMPTING FREEBIES

Display an offer that new customers cannot resist by providing free trials. Fitness centers often distribute flyers that signify a week’s worth trial or a discounted package for first timers. This is a cost-effective way to get good reviews and honest testimonials.

There is nothing more powerful than giving your potential customers a good glimpse of what is to come!

LISTEN TO THEIR VALUABLE INSIGHTS

As you converse with your potential and existing customers, it is important to actively listen to their wants. Do not assume that you know their preferences! Many startups fail because they are selling products with a non-existent demand.

This is why you must encourage constructive feedback. These may be delivered thru social media platforms, focus group discussions, and online surveys. Take the appropriate actions to improve the operations of your small business.

LAUNCH A REFERRAL SYSTEM

My career path was carved when I became an administrative officer in a contemporary yoga studio. One of the studio’s promotions, which endured throughout year was the “Refer A Friend Campaign”. It encouraged the existing customers to invite their friends over to receive up to 20% discount on their next packages. The more people they refer, the higher the reward gets. You may launch the same campaign in your small business.

Remember that people love to be acknowledge. Use that to your advantage!

Image Credits: pixabay.com

New customers are the tools that enable your small business to flourish. If you want to attract more customers, you must consider these people in every step of your journey.

In the dynamic world of the investments, you will encounter the term “short selling”. How does it work and what are the rules behind it?

The age-old practice in investing is that you will profit by purchasing stocks in a low price and selling them for a higher price. Although you have invested in a seemingly good performing economy, some stocks or securities may go down. You cannot earn money by “buying low and selling high” in this circumstance. Fortunately for you, there is another way to make money! That is short selling.

Short selling plays a soothing music to the risk-taker’s ears. Its concept is relatively simple. It takes advantage of the market transitions from higher to lower prices. It occurs when an individual borrows a stock, sells it for a higher price, and purchases the stock again at a cheaper price. Watch this short video to grasp its essence:

Most local brokerage firms let you experience the ease of selling short. Just place an order to sell the stock and communicate with the broker. The brokerage firm will borrow the shares for you to sell. Then, it loans the shares to your account and conducts the sell order.

As with everything, rules shall apply. Here are just some of the common rules in short selling:

1. The “Uptick Rule” is one of the key edicts that short sellers abide. It refers to selling a stock short only when the last trade was a move up. You cannot short a stock that is moving down.

2. The odds may not be in your favor if you heard that a flock of investors are shorting the same stocks that you are shorting. There are so many risks if you short a stock that everyone else does. They can simply abandon their shorts if things do not go as planned. Doing so will drive the price to hike.

3. Short selling during seasonal holidays or during “options expiration week” may attract painful losses because those circumstances do not follow the natural or normal supply and demand.

Short selling takes advantage of the market transitions from higher to lower prices. The steep learning curve intimidates some investors, leading to avoiding it entirely. It is undoubtedly a skill that experienced investors develop!

If you are reading this, be glad that something has not yet happened to your child.

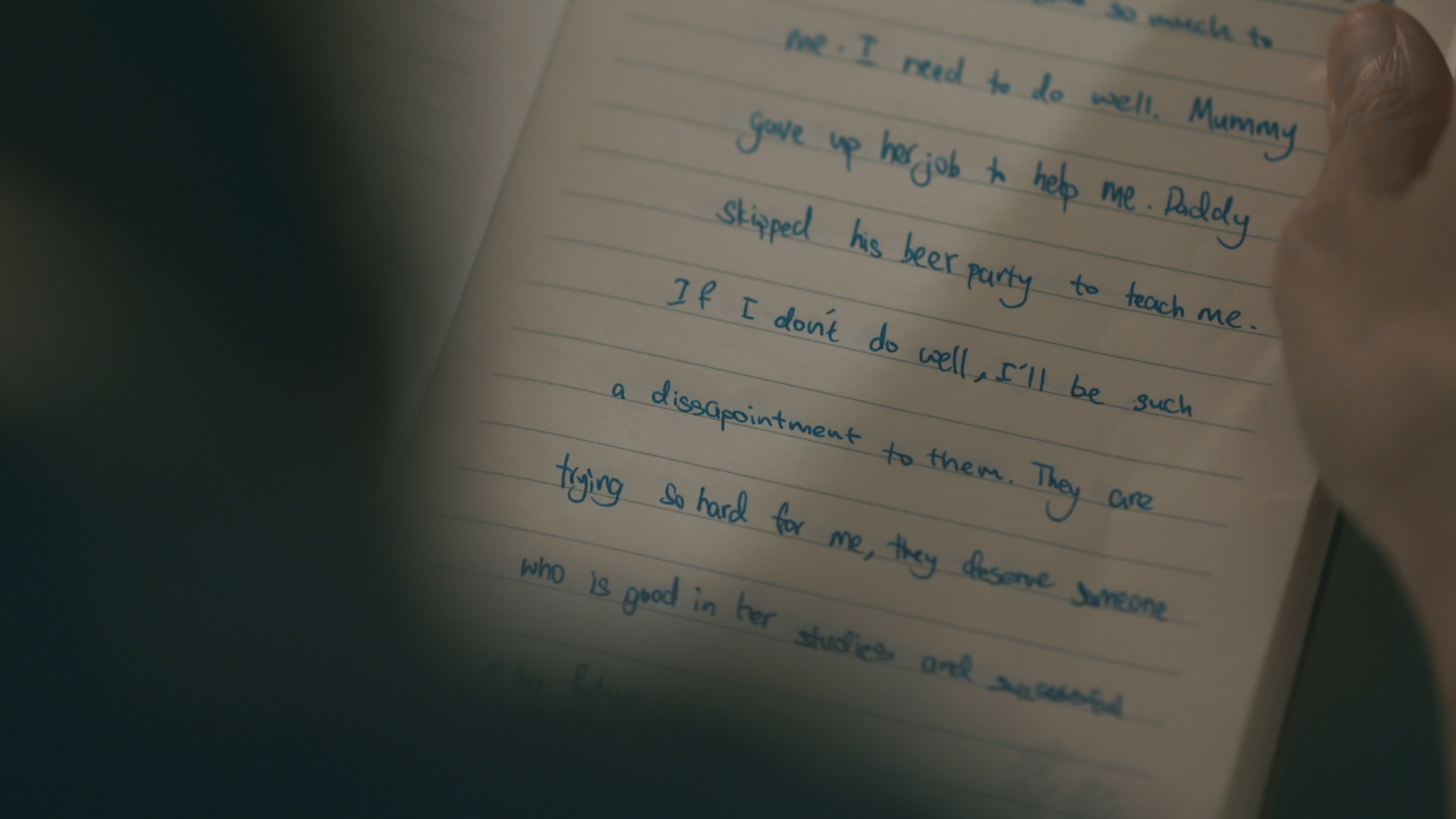

Child suicides are on the rise, as youngsters were pushed beyond breaking point and ended their lives. 10 fingers 10 toes. That was all that mattered in the past.

Now children are measured by a different set of numbers. 70 marks implies lack of effort. 80 marks is not good enough. 90 marks means room for improvement. When is enough?

Stills: Zi Hui Journal, 倦子2: PSLE GO

倦子2: PSLE GO shouts out this message. Your child is tired, yet still trying. Remember, not regret.

As a parent, I urge you to help spread this message. Treasure your child, not their grades. It is not too late.

I was teleported back to a nostalgic era when I was invited to a premier screening of 倦子2: PSLE GO. The venue was perfect in echoing chapters of the past. Numerous movie posters of old greeted me as I entered. It reminded of my childhood, a much simpler time.

Every morning I looked forward to school to make new friends. Not to compete with my classmates. Each time the school bell rang, I dashed out of class to join my friends. It was a beautiful childhood. Do you remember those lovely memories? These moments made me a happy and balanced adult.

Your child may have been denied this privilege to feel happy. Do you remember when you first held your new born? Back then, your child was perfect. You do not remember. Your child became less every day, and had to try harder to achieve more just to make you happy.

10 fingers 10 toes. That was all that mattered in the past. Now children are measured by a different set of numbers. 70 marks implies lack of effort. 80 marks is not good enough. 90 marks means room for improvement. When is enough to satisfy your expectations?

Stills: Zi Hui depressed, 倦子2: PSLE GO

Would you relent only when you witness an irreversible end? Suicides are no longer uncommon among the young. Each news report is heart wrenching; deepest pain only the parent would feel. It is an inevitable end, a result because of our actions, our inaction in protecting our most loved from the harsh judgement of others (and ourselves).

As a professional working adult, every day is an exam. Every hour we endure endless challenges. Do we score 100 marks each time? At home, we comfort ourselves with rest. We pamper ourselves with rewards. Yet, we forcefully push our child through additional stress after school. Your child needs your encouragement, not your enforcement.

倦子2: PSLE GO shouts out this message. Your child is tired, yet still trying. Remember, not regret. A great team effort, displayed most selflessly as Splash Productions embarked on a non-profit filming journey. Splash is to hit something or someone with full impact. In that moment of contact, the origin spreads out and covers a larger area than anticipated.

Splash Productions did exactly that. Impact and Influence. Never once had I been so proud to see familiar names when the credits were rolling. As a parent, I urge you to help spread this message.

Making New Year’s Resolution is synonymous to crafting a new budget plan. Creating these two signifies an act of self-improvement. However, no plan is entirely foolproof!

These are just some of the reasons why I previously failed at budgeting:

I FOCUSED HEAVILY ON THE PRICE

Before purchasing a new laptop for work, I inspected some of the contenders from the well-known brands. My new laptop must not only fit my physical preferences, but also my financial limit of up to S$1,000. I searched vigilantly through the store and found a 14-inch HP laptop as well as a 14-inch Dell laptop. These two devices have the same processors and operating system. However, the main memory of the former is 8GB and the latter is 4GB. An important fact is that only the Dell laptop was within my budget.

Which one did I chose? The one with better specifications. Although it retailed for S$1,099, I still taught that it was a smarter investment.

According to a 2012 study published in the pages of the “Journal of Marketing Research”, people fail to follow their budget because they are more likely to spend more than they planned. You must not always beam too much focus on the price. Instead, compare the value (e.g., which has laptop optimal screen size and RAM) of what you are getting before committing to a sale.

MY BUDGET WAS TOO STRICT

Upon getting my first full-time job, I started to restrict myself. My goal was to make enough money to save up for my graduate studies and to help my parents in the household expenses. I did so. I gave about 10% of my salary to my parents and 50% would go to my savings account. I removed my trips to the spa and the cinema. A hefty savings greeted me at the end of every month. But, I felt burnout as there was no room for pleasure. This is when my budget failed me.

To turn things around, I started to make money on the side. I became a blogger that solicits money for endorsements. Eliminating unnecessary expenses is a good idea, but you must reward yourself (from time to time).

I FELT EXHAUSTED WHILE TRACKING MY SPENDING

You need discipline to track your own spending. I realized this firsthand. I used to compile all my receipts and banks statements. But, it got too exhausting! I started with a willpower to succeed until the constant vigilance took a toll on me.

A study supports my statement as it was found that self-control and intelligent decision making involves one’s energy supply. Once this energy runs out, you are more likely to go on a spree.

Image Credits: pixabay.com

Get things by following thru your plan. Practice is the key! Improved decision making and control will become second nature to you as time passes.

In its fundamental form, insurance is a contract that enables individuals or entities to receive financial protection against losses. It ensures the stability of families and businesses after a crisis or other unfortunate events. Simply put, insurance grants policyholders a peace of mind. Isn’t that what everybody wants – to be able to sleep at night without having to worry about what the future holds?

These are the reasons why I am drawn to getting insurance policies. I have to be completely honest. One of the major drawbacks that I dislike about insurance is its complexity. I am apprehensive about the piles of questions and bulky documents. Do not get me started about the confusing technical terms!

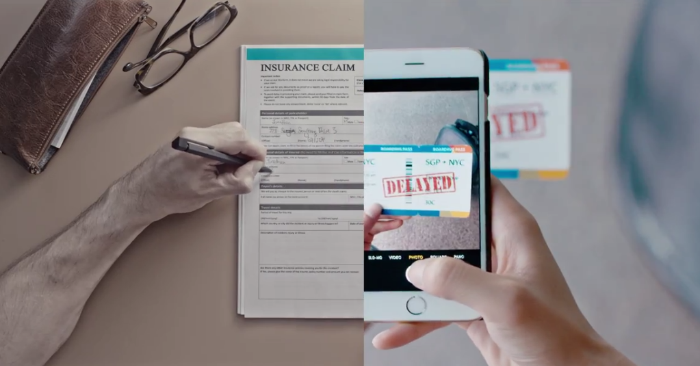

To my delight, I was introduced to a revolutionary insurance company that dances gracefully with the modern tides. This was none other than FWD Insurance. FWD Insurance aims to transform the way that Singaporeans experience insurance by simplifying the purchase and claims process. It helps you to skip the agent by directly working with them online.

Say goodbye to nerve-wracking call backs and time-consuming interrogations by embracing their user-friendly website!

FWD Insurance understands how valuable a working Singaporean’s time and money is. This is why the company maximizes these two commodities through providing insurance quotations under 60 seconds for car insurance and 10 seconds for travel insurance. These impressive figures are due to the fact that FWD only asks questions that are absolutely necessary.

For instance, it took me 25 seconds to be quoted with the premium of about S$174 for a DIRECT-Term Life insurance that seeks to cover 5 years of my life. I used the rest of my day to focus on other productive matters. You can do the same thing too!

The people behind FWD best explained the company’s concept: “We believe that insurance doesn’t need to be complex, sold through middlemen, or take up vast amounts of your time.” It offers competitive prices and easy-to-understand insurance.

Attractive Insurance Products

It is usual for people to feel skeptical when they encounter an insurance company for the first time. Wash away this feeling by knowing that you are supported by a company with a strong financial record. FWD is the insurance business arm of the established investment group, Pacific Century Group (PCG).

Choose from the four secure insurance products such as DIRECT-Term Life Insurance. Car, Travel and Personal Accident.

A. DIRECT-TERM LIFE INSURANCE

The DIRECT-Term Life insurance ensures that your family’s financial future is secured despite unfortunate events such as becoming diagnosed with a critical illness, becoming permanently disabled, or passing away.

These are the primary reasons why I am drawn to this policy:

I can choose the period that works for my budget and lifestyle (e.g., 5 or 20 years).

I can purchase coverage through my smartphone – without going through a middleman.

Because FWD does not pay commission to agents, my coverage of up to S$400,000 may cost less than S$1/day.

B. CAR INSURANCE

Three comprehensive plans cover vehicle repairs, third-party damages, medical expenses, and roadside assistance. These plans were crafted to suit your personal needs and budgets.

No matter what plan you avail, your repairs will be completed by the FWD workshops. You can cruise along blissfully until your car turns ten. Furthermore, your 50% NCD is guaranteed for lifetime. NCD stands for no-claim discount. Drivers who have earned their 50% NCD get to keep it for life because they believe that one accident doesn’t make you a bad driver.

On top of that, you can add amazing features which gives you coverage when you are driving in West Malaysia and certain parts of Thailand.

C. TRAVEL INSURANCE

Take for instance; to reap the rewards of her hard work, Jena scheduled a weeklong vacation to Thailand. The beautiful country has so much to offer from pristine beaches to established sports clubs. She did not forget to pack her favorite S$200 golf putter. To enjoy a fuss-free tropical getaway, she purchased FWD’s travel insurance. It was one of the best decisions she ever made as the putter got lost in the airport and fortunately, sports equipment is covered by the policy.

Aside from sports equipment, the travel insurance also includes unlimited medical evacuation. You read that right! The last thing on your mind is how much your emergency evacuation will cost. This is why FWD has thought of this for you.

You can expect the claiming process to be a breeze too. Claim with a few clicks with the “Click to Claim” feature. This means, all you have to do is snap your boarding pass and claim for flight delays via WhatsApp. This feature is available for baggage delays too. Simply take a photo of your baggage slip and send it to FWD via WhatsApp. That is convenience at its finest!

D. PERSONAL ACCIDENT INSURANCE

Personal Accident (PA) insurance provides compensation in the event of disability, injuries or death. In fact, one feature unique to FWD is that the policy also covers the most number of infectious diseases including Zika and dengue fever. Under this policy is the Guardian Angel Benefit. If both parents pass away or become permanently disabled due to an accident, FWD will provide up to S$500,000 for the surviving children.

Lastly, natural circumstances now cannot stop you from having fun as ticketed event cancellations due to haze are covered. Apparently, they are the only insurer in Singapore to offer this.

Irresistible Features and Highlights

Before you make a commitment, it is important to know what this new insurer can do. Let me start by stating the fact that there are no middlemen or agents. Since you do not have to pay for commissions, you can save more money.

FWD allows you to complete your purchases online. It is so quick and easy to complete the online quotation that even your 9-year old niece can do it for you! As soon as you make your purchase, you will get an email with the policy. You will also receive an SMS that notifies you to check your email.

Lastly, the policies are delivered with no technical terms. You will know exactly what you will get explained in plain English.

From now till 31 January 2017, you can now enjoy a 10% discount on all FWD insurance products with this promo code – FWDHi10.

For the people behind FWD, customers are at the heart of the entire process. They let you experience exceptional insurance by minimizing your effort and making products readily accessible. May they change the way you feel about insurance!